Chapter 3

The Capital Stack and Two More Variables

Devising how to fund your business investment typically involves multiple capital sources. Those capital sources are mostly evident from the right side (or so it's always called) of the financial statement balance sheet, which is where liabilities and shareholder equity are reported. In finance vernacular, the various sources of capital used to finance business investment are often referred to as the “capital stack.” In the case of Daymond John, his capital stack was simple: He personally borrowed $120,000 on a second mortgage loan on his home and then infused that cash into his company as an equity investment. Typically, capital stacks are far more intricate.

The Right Side

I have found that most investors and entrepreneurs spend far more time focusing on the left side of the balance sheet than the right. In the case of STORE Capital, the most recent company where I served as founding chief executive officer, the left side of the balance sheet was loaded with profit-center real estate assets the company owned and leased on a long-term basis to service, retail, and manufacturing companies across the country. Most of the questions I fielded from investors and analysts stemmed from these investments.

When it comes to evaluating the right side of real estate company balance sheets, many corporate observers are simply inexperienced. For one thing, most public real estate companies have similar sorts of borrowing, with the resultant interpretation that the right side of a balance sheet is less important. However, this is far from so.

In 2005, at a predecessor public company, we conceived of a novel way to use serially issued secured debt. About three years after we embarked on this process, we sold the company to an investor group that was able to fully assume the highly flexible debt we had created. The result was that our shareholders were able to realize a compound annual rate of return approximating 19%, which would not have been possible without the flexible, assumable nature of our debt obligations. Had we simply followed the well-worn path of traditional financing options employed by most other industry participants, we and our shareholders would have missed out on this opportunity.

Borrowing sources can be instrumental in elevating shareholder rates of return, improving corporate flexibility, and even protecting shareholders in the event of severe economic turbulence.

Other People's Money (OPM)

When conceiving a corporate capital stack, there is an order of operations. At a high level, your analysis should begin with how much you can borrow, and then back into how much equity investment you might need. In the example of FUBU, Daymond John had no access to corporate borrowings when he founded the company. So, he made a $120,000 equity investment into FUBU that was funded by a personal loan he had to collateralize with his home. That small, but meaningful, investment ended up generating over $6 billion in revenues, ultimately making Daymond John an amazing financial success story. Over my years in business, I have seen similar success stories and have been proud to play a role in our customers' achievements.

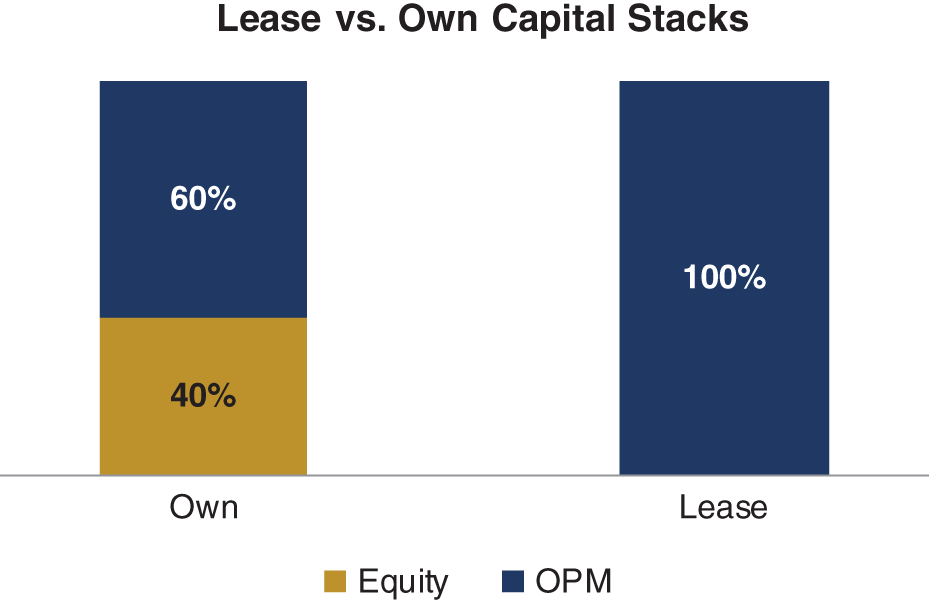

As a finance professional, I do not think personally about borrowings when considering how a business should be capitalized. That is too simplistic. Instead, I think about “other people's money” (OPM). For instance, STORE Capital is in the business of owning the profit-center real estate of companies and then leasing it to them on a long-term basis. There are numerous companies that use a lot of real estate in their business (think restaurants, fitness clubs, retailers, and many more) and they have a problem to solve. They could own the real estate and seek bank financing, or they could instead lease the real estate from a company like STORE.

Real estate ownership requires an equity investment that can typically range as high as 40%, paired with borrowings for the remaining 60% plus. The alternative is to have a company like STORE put up all the money for the real estate, buy it, and then lease it back to you on a long-term lease. The amount of OPM entailed is different. A real estate lease offers far more OPM than does the choice of real estate ownership. Yet both are viable choices when it comes to creating a corporate capital stack.

As a self-described “finance guy,” I could care less about the accounting treatment of my capital stack. My attention tends to turn in the direction of equity returns, corporate flexibility, liquidity, and margins for error, which are important keys to value and wealth creation. I find that most corporate CEOs feel likewise. Hence, some will choose to own equipment or real estate, while others will elect to lease equipment and real estate. Either way, these decisions impact the corporate OPM and equity mix. They impact the capital stack.

Accountants like to include within company liabilities non-interest-costing obligations, such as trade payables, deposits (deferred income), and accrued liabilities. As a finance guy, I ignore such liabilities within the corporate capital stack. Since they cost nothing to me, I subtract them from the amount I would otherwise have to make to determine business investment, the first of the Six Variables, which was discussed in the preceding chapter.

Borrowings at cost are generally visible on a corporate financial statement, while the cost of leased assets is nowhere to be seen. Accountants have always been obsessed with lease accounting, which embodies why accounting is always going to be an imperfect reflection of financial reality. For most of my career, real estate leases were not included on a balance sheet at all. They just showed up in the form of rent expense, and required a detailed financial statement footnote disclosure explaining how much in lease payments the company was obligated to pay over time. All of this changed with new accounting rules imposed in 2019.

GAAP Lease Accounting

| Old Rules | 2019 Rules | |

|---|---|---|

| Show an Asset? | No | Yes |

| Show a Liability? | No | Yes |

| Show OPM Proceeds? | No | No |

In 2019, new lease accounting standards set by the Financial Accounting Standards Board (FASB) were enacted, resulting in the creation of non-cash “right to use” assets and liabilities, representing the estimated present values of lease payment obligations.1 Since a lease is generally not a debt substitute, but instead a debt and equity substitute, the amount of the “right to use” liability and asset created will typically not approximate the actual amount of the OPM represented by your decision to lease.

Variables #2 and #3: Amount and Cost of OPM

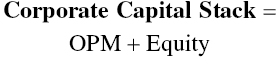

A company's capital stack provides numbers two and three of the Six Variables at the hands of corporate leadership to deliver investor returns.

- The second of the Six Variables is the OPM/equity mix.

- The third variable is the cost of OPM.

In starting a company, business owners understand fully the cost of assets they choose to rent instead of buy. Business owners also understand the amount of money they borrow from banks and other sources. Add the two together and you get the second variable, the amount of OPM used in a business.

In determining current investor returns, the cost of OPM is paired with the amount of OPM used to arrive at the third equation variable. The simple formula is as follows:

If you were computing the cost of OPM for a year, you would take the total amount of interest and lease payments shown above and then divide them into the average of the loan principal outstanding and the cost of the leased assets deployed. When it comes to determining the cost of OPM, my treatment of leases can seem simplistic, because leases often have escalators built into them and sometimes allow for an accumulation of equity with a future known purchase option. But, as you will see as we go on, I am most interested in computing a current investor rate of return, and not a theoretical total rate of return. To do this requires that I simply compute a current cost of OPM.

Cost of Capital vs. Cost of Equity

A corporate capital stack is comprised solely of interest-costing OPM, together with equity that is likewise demanding of a return. If you can take the total annual OPM interest and lease cost, together with the desired current annual rate of return for equity investors, and then divide that cost by the amount of your capital stack, you can determine your current annual corporate cost of capital. Then, if you can realize current corporate returns that exceed that cost of capital, you have market value added (MVA), creating a business worth more than its cost. The whole is now worth more than the sum of the cost of its parts.

In golfing terms, you have broken par, which is a feat few can accomplish.

Corporate cost of capital is a frequent topic of conversation in business schools. However, I decided some time ago that the only thing that really mattered from a mathematical point of view was the cost of equity. After all, entrepreneurs are not trying to make their lenders, equipment owners, or landlords rich. They are trying to make their equity owners rich.

So, to keep it simple, the important metric to know is not corporate market value added. It's equity market value added, which is the amount by which the value of corporate equity exceeds its historic cost.

When it comes to your capital stack, you want to strike a balance between OPM and equity having the potential to deliver the highest equity rate of return. Hence, in the order of operations to determining a capital stack, you start with the amount of OPM you can attain and then back into the amount of equity you require. When it comes to equity, less tends to be more.

Capital Stack Assembly

During my business career, I gained something of a reputation for creating financial models. Not to be outdone, Mort Fleischer—my mentor and business partner for most of those years—created “Mort's Model,” which he had framed, and then freely passed around, and which I will immortalize here. Mort's Model embodies the notion of less equity is more, and goes like this:

“Yenem's Gelt” is Yiddish for OPM, and “∞,” otherwise called a “lazy eight,” is the mathematical notation for infinity, which is supposed to be the resultant equity return. The formula is intended to convey that a business generating cash flow and funded entirely with OPM will yield an infinite rate of return to the owners of the business. Of course, equity rates of return would not be computed this way. Instead, operating cash flow would be divided into the equity investment of zero to arrive at an effective infinite rate of return. Mort simply wanted to make the point of the importance of OPM. Saying it in Yiddish elevated the amusement level. In my years in business, I have seen a number of people successfully start or buy businesses with no equity. It is possible, but not easy.

Consistent with Mort's Model, forming a capital stack begins with a determination of the maximum amount of OPM you can get. In the end, you may not want to maximize your use of OPM, but it is good to know the art of the possible. As I noted in the conclusion to the last chapter, companies go out of business because they run out of cash. So, understanding where liquidity can be accessed outside of business operating cash flow is important. Plus, understanding how to maximize OPM will give you the best shot of minimizing equity and achieve something close to Mort's Model.

At a high level, when it comes to the puzzle of how to assemble an equity stack, there are just three simple steps:

Step 1: Start with money that has the longest repayment requirements. Hard assets like real estate and equipment can be financed for a long time and may even be leased.

Another area where long-term money is to be found is with asset-based loans (ABLs), whereby lenders advance money against accounts receivable and inventory. Such loans are often in the form of lines of credit that can mature in a year or two. However, they require no repayment and can generally be readily extended, since they are based on accepted formulaic advance rates against assets that can be easily valued. Accountants often think of such credit lines as short-term, owing to their debt maturity time frame. Finance experts tend to think differently, because they know such lines to be readily extendable.

Another source of long-term money, if you are buying a business, can be in the form of notes payable to the prior owner, which are often unsecured corporate obligations.

Financing assets through OPM that involve long-term repayment (as in equipment or real estate loans) or modest to no repayment (as in equipment leases, real estate leases, or ABL facilities) provides several benefits: OPM can be maximized, monthly payments can be minimized, and the capital stack can be stable.

OPM that is repaid quickly will alter the capital stack over time to elevate equity. That may sound nice, but an altered capital stack will tend to lower equity returns and potentially lessen corporate cash flow that can otherwise be invested in expansion. Repaying OPM and tilting the capital stack to 100% equity is fine, so long as your business has nothing more productive to do with the cash.

Step 2: Your next step is to turn to short-term money. In general, this will be money that has limited collateral and is repayable from free cash flows expected to be thrown off by the business after all the other OPM obligations have been met. Such loans will tend to amortize more quickly and represent a more volatile form of OPM because they are less universally available. Economic cycles come and go, lender risk tolerance rises and falls, and corporate cash flow loans are the most vulnerable to such changing environments.

There may be an order of operations to determining OPM and a capital stack, but there is no standard OPM portion of a capital stack. Daymond John was declined 26 times for bank loans before finally borrowing money from a subsidiary of a South Korean conglomerate that he would not have found but for his newspaper advertisement. Indeed, commercial banks are not all the same. Likewise, there are a myriad of equipment and real estate leasing companies having diverse views of investment risk. And then there are non-bank lenders, such as small business investment companies (SBICs), business development companies (BDCs), and a host of non-bank direct lenders that collectively amounted to over $800 billion in assets at the end of 2019 from less than $30 billion in deployed capital in 2000.

When it comes to OPM, there is a lot to choose from, which means that it's important to be informed and selective. Take time to shop.

Step 3: Your final step is to determine the amount of equity required. Once the OPM portion of the capital stack is determined, then the amount of equity you require is simple. It's the difference between your required business investment and OPM.

Equity Sourcing

Having solved for the required amount of equity, the question is, where does the equity come from? In the case of Daymond John, he was unable to get any OPM to start up FUBU, so he had to put up all the money himself in the form of equity by pledging a personal asset to the bank. He would later get OPM from Samsung and others as he grew FUBU into the success that it became.

As you might guess from our discussions up to now, there is a limit to the amount of equity you should invest. Equity is entitled to all the free cash flow remaining after paying the OPM obligations. The relationship of that free cash flow to the equity you invest, combined with the potential growth of that cash flow and the risks in the business, will determine whether you have the potential to create EMVA.

Equity does not have to all come from you. Most entrepreneurs I have known began their careers with little in the way of financial resources. After he became a financial success story, Daymond John landed a spot as a “shark” on the syndicated show Shark Tank. Each week, select entrepreneurs seeking capital to start or grow their business would pitch their offerings to Daymond and other sharks, all highly successful businesspeople, in the hopes of raising added equity without giving away too much of their companies. In essence, the sharks became OPM equity for business founders and brought with them added skills to help the companies (and their personal investments) succeed. With that said, for simplicity I will start with the notion that all equity is your own money, which I also call YOM. OPM equity will be a subject for later.

Notes

- 1. In 1996, we created the first US real estate master trust. The idea was to borrow against a pool of real estate by issuing bonds. Then, later, we would grow the vehicle by adding pools of real estate in subsequent years. In this way, unlike traditional real estate bond issuance, where the bond holders are secured by the specific pool they invested in, master trust bondholders would be secured by the collective the real estate held in past and future pools. For investors, the disadvantage was that they would invest in a pool of notes secured by real estate, but without fully knowing what their ultimate collateral would look like, since we could add to and occasionally substitute the collateral. However, the clear advantage for investors was that the pool could grow larger and become far more diverse over time, with a resultant likelihood that it would perform consistently. By contrast, traditional individual pool borrowings could be expected to have a higher level of performance variability. For us, the master trust delivered secured vehicle where we could service and control our own assets, giving us the ability to sell, improve, or substitute real estate to maximize the value of the pooled assets. Alignments of interest are always important, especially since commercial real estate note issuances are done without recourse to the issuers. In our case, we had an equity commitment amounting to 30% of the real estate investment amount.

- 2. A present value is computed by discounting back future lease payments to be made at a company's estimated cost of borrowings to arrive at a theoretical borrowing equivalent. While the borrowing equivalent may be a reasonable approximation, the discounted value will not tend to equal the amount of OPM used, which is key in evaluating comparative corporate capital stacks. The present value of lease streams is also somewhat irrelevant, since companies nearly always extend leases or replace them with other leases. In that sense, computing the present value of a lease stream does not treat companies like going concerns. Financial statement analysts are most interested in the annual lease payment obligations and generally assume these to be ongoing or increasing, assuming the company is to remain the same size or grow.