The Pricing of Art and the Art of Pricing: Pricing Styles in the Concert Industry

Pascal Courtya and Mario Paglierob, aUniversity of Victoria and CEPR, Victoria, Canada, bUniversity of Turin and Collegio Carlo Alberto, Moncalieri, Italy

Abstract

We document the existence of pricing styles in the concert industry. Artists differ in the extent to which they rely on second- and third-degree price discrimination, and in the probability of their concerts selling out. Most strikingly, artists who use multiple seating categories are more likely to vary prices across markets and less likely to sell out concerts. These patterns are difficult to explain within a standard profit maximization paradigm. The hypothesis that artists differ in their willingness to exploit market power provides a plausible framework for explaining these patterns in artist pricing style.

Keywords

Price discrimination; Rationing; Behavioral pricing; Pricing style; Exploitation of market power; Fair pricing

JEL Classification Codes

D42; D45; L21; L82; Z11

Tickets to see musicians such as Bruce Springsteen, who insists that entry to his shows be cheap enough for working stiffs to afford, are particularly susceptible to what fans call ‘price gouging’.

Bruce Springsteen, Pearl Jam, and Dave Matthews have never charged as much as they could for their tickets.

When Babs tried to charge up to Euro 900 for a Rome gig, Italian fans rebelled and urged the city’s government to refuse the singer use of a stadium. After the public outcry, Streisand cancelled the concert.

13.1 Introduction

Why devote an entire chapter of the Handbook to studying how artists set prices for live concerts? One reason is the overwhelming popular interest in the topic. Ticket pricing receives a lot of attention in the press, and fans seem obsessed with the price and availability of tickets. Journalists howl when concert prices are perceived as outrageously high and squawk when fans have to line up for hours for a much sought-after ticket unless they can afford to pay several times the face value on online resale markets. Newspapers also report on how difficult it is to get some or all types of seats when tickets are all sold at the same price. Artists, promoters, fans, and commentators have different views on ticket pricing. So who should one listen to?

Ticket pricing is also interesting because of the unusual nature of the live event industry. The suppliers, typically individual artists or bands, are not the textbook profit-maximizing entrepreneurs. Many artists are also songwriters and composers who see higher meaning in their music. Some songs have strong emotional and political messages. Music can raise spirits and aspirations. Artists are celebrities who often rely on their public image to sell their art. Some enjoy public adulation for the sake of it. Another unique feature of the concert business is that artists sometimes express personal views about who should attend their concerts and how much they should be expected to pay. Bruce Springsteen, for example, explains the low price of tickets to his concerts as an attempt to make them affordable to the working classes. One may question whether such statements are sincere. The debate goes on.

Concert-goers are not textbook consumers either. Many fans are loyal to specific bands, and develop emotional attachments to particular types of music and individual artists. The media reports on the lives of artists, thereby feeding fans with information that shape their perception of the artist. Some fans feel that concert attendees should not be selected on the basis of how much they are willing to pay but rather on the basis of their sincere understanding of, and commitment to, the art. Many artists are sympathetic to this view.1

These are just a few features of the live music industry that contribute to its uniqueness. While some have to do with the supply side of the market, others have to do with the demand side. The nature of the product and how it is distributed to consumers also raise interesting issues. Pricing is a salient issue because live bands have a tremendous amount of market power and sell highly differentiated products. Not all seats in a venue provide the same experience. Moreover, live music is also often delivered to consumers through tours that stop in cities with sometimes widely different local demands. This raises complex pricing issues. Should an artist charge different prices for the same concert in two different markets? Should an artist charge different prices for two seats located in different areas of a venue? What determines the artists’ willingness to use price discrimination?

While interesting questions are a good starting point for conducting worthy empirical research, they are not enough; one also needs reliable data to conduct statistical analysis. In this sense, concert pricing offers a unique laboratory for the researcher. Artists have to make a large number of choices when pricing tickets. Each time an artist launches a tour, which most artists do regularly, decisions must be made concerning the overall level of prices, how much prices should be differentiated across local markets, and how much prices should be differentiated within a venue. Artists set ticket prices in advance and rarely change them (although prices may vary widely in the resale market). Two trade publications cover the concert industry, Pollstar and Billboard, and maintain datasets that match artists, promoters, venues, and concert prices. Most importantly for the researcher, the concert industry lends itself to the use of statistical analysis because the econometrician can use repeated observations to control for many unobserved factors. Artists tour repeatedly, year in and year out, and give a large number of identical concerts within each tour. They may sing over and over again in the same city and venue as part of different tours. In addition, a fairly small number of promoters repeatedly promote concerts given by top artists.

A research topic is of particular interest if it offers outcomes that challenge conventional views. The live music industry is rich in such puzzles. First and foremost, one has to ask why rationing and resale markets are so common. The Economist (2011) claims that ‘Live music is one of the few businesses in which second-hand goods often sell for more than new ones’.2 This may be an overstatement, but it points out the connections between the price level, the extent of price differentiation in the primary market, and the subsequent resale activities in secondary markets. Economists and others have produced many theories of underpricing, rationing, and price rigidities. However, rigorous empirical evidence on rationing is almost non-existent. Overall, it is fair to say that there is no systematic understanding of the causes of rationing.

Another puzzling phenomenon is that price discrimination is not very common. Why are seats in the same venue often sold at the same price? Even when there are multiple seating categories, it seems that the number of categories is fairly small. The same is true if we consider the pricing of the same concert in two different cities. Why do so many artists set the same price for concerts that are part of the same tour?

Connolly and Krueger (2006) highlight these puzzles in concluding their review of the ‘Economics of popular music’ in Volume 1 of the Handbook of the Economics of Art and Culture. Several areas they deem worthy of future research have to do with ticket pricing. They ask: ‘What determines the amount of price differentiation within concerts? Is there less regional variation in prices for the same concert than one would expect in an efficient market? If so, why? Why do tickets appear to be underpriced for many concerts?’ This chapter takes on these questions. We study price discrimination and rationing in the concert industry.

We document new stylized facts from a large dataset that covers about 20 000 concerts offered by the top 100 artists in the period 1992–2005. Our initial focus is on the issue of the use of price discrimination (between seats within a venue and between venues that belong to the same tour). We document the existence of large differences across artists in the use of second- and third-degree price discrimination, even after controlling for a large number of sources of unobserved demand and product heterogeneity. Some artists vary prices to respond to demand conditions while others do not, suggesting that artists may have different pricing styles. Next, we develop a simple framework that is consistent with these stylized facts, and hypothesize that artists differ in their willingness to exploit market power. This assumption provides a plausible framework for explaining the observed patterns in artist pricing styles: (i) it rationalizes the observed heterogeneity across artists, and (ii) it implies that artists who are more likely to vary prices within a venue will also vary prices across venues more and ration tickets more. These predictions, which are unique to the hypothesis that artist pricing styles stem from differences in willingness to exploit market power, find remarkable support in the data.

Our evidence is drawn from one industry: concerts for live popular music. There are many reasons for this choice. As mentioned earlier, data on ticket prices are uniquely suitable for conducting statistical analysis. In addition, the industry is significant in value, global, and subject to market forces with little government interference, three features that distinguish it from many other performing arts.

The rest of this chapter proceeds as follows. Section 13.2 presents background information about the live event industry, reviews the literature, and lists a number of open questions. Sections 13.3–13.5 present the data and establish stylized facts about the use of second- and third-degree price discrimination. Sections 13.6 and 13.7 show that it is difficult to associate the differences in pricing practices to unobserved heterogeneity. Instead, heterogeneity in artist willingness to exploit market power can, in fact, rationalize a number of observed patterns in the data. Section 13.8 presents further evidence consistent with the hypothesis that artists differ in their pricing styles. Section 13.9 concludes and lists a number of questions for future research. This last section also discusses the broader relevance of our work and explains how the concept of pricing style could be applied elsewhere.

13.2 The Live Event Industry: Facts, Literature Review, and Open Questions

The economics of live events raises a number of interesting issues that cannot all be addressed in a single chapter. Here, we focus on second- and third-degree price discrimination and rationing. To prevent confusion, discussion of the broader context and of connections with other pricing issues is useful, although of course these issues are not directly addressed here.

This study focuses on the primary markets for concert tickets. Concerts are often sold out before the event date. Consumers who cannot purchase a ticket in the primary market can purchase one in resale markets. The most common ways to do so are through auction websites such as eBay, specialized resale websites, or professional brokers. Although secondary markets are outside the scope of this study, we do investigate the issue of sold-out concerts, which is essential to understanding the economic rationale for secondary markets.

Typically, the price of tickets is fixed when a tour is announced, prices do not change over time, and tickets are distributed through the box office or national distributors. Although there have been some innovations in recent years (e.g. revenue management and distribution through artist websites), this is still the dominant model for the industry. While we do not study these innovations in the core of this chapter, we shall touch on them again in the conclusion, when discussing areas for future research.

Another consideration is that some artists offer many concerts each year and rarely take breaks, whereas others hardly ever give live performances. We leave aside the decisions of when to go on tour and which cities to visit, taking these decisions as given, and focus on the setting of prices for different seats in a venue and for different venues in a tour. Finally, the revenue from ticket sales is often supplemented by concessions revenues coming from the sale of food and drinks as well as CDs and a wide variety of souvenirs. Although these are important sources of revenue, they are not the focus of this work and are not discussed at great length. The artists present in our sample make most of their income from touring. Connolly and Krueger (2006) discuss some of the connections between touring and other sources of income, recording in particular.

13.2.1 Industry Background

We present the key characteristics of the concert industry that are relevant for this chapter. A more detailed review is available in Connolly and Krueger (2006) and Waddell et al. (2007). The modern touring industry was born in the late 1960s when a few bands such as the Rolling Stones and Led Zeppelin regularly started touring a variety of arenas and stadiums, using their own experienced crew to take care of the sound, staging, and lighting. In the 1980s, advances in technology allowed bands to offer even more ambitious stage shows that were louder and brighter, and available to ever-larger audiences. By 2007, the North American concert industry had grown to $4 billion in revenue and 100 million in attendance.3

Although some artists give single concerts, the dominant model in the industry is that of tours. In brief, a concert tour is typically organized by an artist represented by his or her manager, a (booking) agent, and a promoter. The artist and the agent agree on an act and a tour plan. The agent then looks for promoters to organize the event in each city. The artist comes to an agreement with each promoter on a pricing policy and on a revenue sharing rule. Promoters are in charge of organizing the events. This involves booking venues, advertising, and collecting revenues. There are some variations on the theme. Most artists use the same set of promoters to be in charge of the tour, but some also use local promoters in certain cities to tap into the local expertise so crucial for success. A few artists even do everything in-house and contact the venues directly. Although there are different types of tours (e.g. promotional tours of new releases, seasonal tours, festival tours), all of the concerts in a single tour usually include a common set of songs and similar staging, and are marketed together.

13.2.2 What Is Specific About the Pricing of Live Events? A Review of the Literature

Ticket prices of concerts are typically set jointly by the artist and the promoter(s) when the tour is announced, and remain unchanged thereafter. Each event is unique and there is no set formula for pricing a concert. There is no second chance if one gets the wrong number of seating categories or prices. Events are sometimes added or cancelled, but prices or category allocations typically remain the same.

The problem of pricing tickets for live events shares much in common with selling perishable products such as tickets for air travel, booking hotel rooms, or handling restaurant reservations. At the heart of the problem is the issue that the seller has a fixed capacity, faces much demand uncertainty, and has a limited amount of time to sell tickets. Many industries dealing with perishable products use techniques known as revenue management, dynamic pricing, or responsive pricing (Courty and Pagliero, 2008) to handle these problems. However, the live event industry does not think about pricing a seat for a concert in the same way that a revenue manager thinks about pricing a seat for a flight or a hotel room. The concert industry is unique in its lack of sophistication. Although we have seen more experimentation with revenue management in recent years, it is still rare, and one has to ask why the concert industry does things differently.

13.2.2.1 Price Discrimination

According to price discrimination theory, prices are expected to vary in response to differences in demand in different markets (third-degree price discrimination) or for different seats in the same venue (second-degree price discrimination. See Stole (2007) and Courty (2010). Live events are peculiar in that the distribution of seat quality is given by the structure of the venue, and the artist decides only on the number and location of the different seating categories. Rosen and Rosenfield (1997) present a theory of second-degree price discrimination that deals with this specific problem.

Courty and Pagliero (2012) estimate (using the same dataset as the one herein) that the return from price discrimination relative to uniform pricing is about 5% of revenue. The magnitude is consistent with the results of Leslie (2004) in the context of a Broadway show. To put this number into context, assume that the artist’s profits are 40% of revenue (LaFranco et al., 2002). Price discrimination increases the artist’s take by 12.5%. Courty and Pagliero (2012) also show that the return to price discrimination increases in markets where demand is more heterogeneous, as predicted by price discrimination theory.

A preponderance of evidence indicates, however, that artists do not fully exploit the revenue potential of seat differentiation within a venue. The number of seating categories used in the concert industry appears to be relatively low. The majority of concerts in our sample use two seating categories and the maximum number of seating categories is four. In the context of a Broadway show, Leslie (2004) reports a similar observation. More than three seating categories for a given show are never used. In contrast, the number of seating categories can be quite large for classical music events (Huntington, 1993).

Why do artists not increase the number of seating categories? One may argue that seat differentiation is not important in the concert industry. However, Leslie and Sorensen (2009) present evidence consistent with the fact that not all seats are alike within a seating category. For example, the best seats within a category are much more likely to be resold in secondary markets. Connolly and Krueger’s (2011) analysis of resale markets is consistent with these findings. Their survey reveals that the main reason for buying tickets on the secondary market was to get better seats.

Courty (2011) shows that a monopolist prefers to sell all the seats in a venue at the same price if low valuation buyers are more likely to obtain the better seats. Leslie and Sorensen (2009) make a similar point. They show that the existence of a secondary market influences the queuing game as well as the sales of each seating category in the primary market. Clearly, there are interactions between the primary and secondary markets.

Courty and Pagliero (2012) estimate the return from adding seating categories. They find that although the return to price discrimination decreases with the number of categories, the return from adding a third and fourth category is significant (about half the return of introducing a second category). This suggests that some artists leave money on the table. Einav and Orbach (2007) address a similar puzzle in the context of the movie industry. They begin by observing that prices do not vary for different movies within a theater, despite differences in theatrical potential and realized success. They consider a different dimension of product quality than we do (film quality rather than seat quality), but the puzzle is similar: firms sell differentiated products at the same price. Einav and Orbach rule out conventional explanations based on fairness, uncertainty, and agency, and conclude that history and industry conservatism must be at play. A similar explanation may also hold in the concert industry. For example, industry norms and resistance to innovation may explain why so many concerts use just two seating categories. Nevertheless, this type of argument is not useful in explaining the large differences across artists in pricing choices central to the present analysis.

There is a growing empirical literature in industrial organization on price discrimination (Verboven, 2007). Several studies investigate the relationship between second-degree price discrimination and market structure (e.g. Borenstein and Rose, 1994; more recently, Busse and Rysman, 2005). The issue is relevant in markets with multiple firms selling products that are close substitutes. Market power in the concert industry differs because products are differentiated in two key dimensions. Artists have loyal fans who may not substitute even within a given musical genre. Even more importantly, few concerts are offered in any given local market on the same date. For these reasons, artists have a tremendous amount of market power.

Another line of research has tried to explain why service operators (e.g. telephone, electricity) offer only a few types of contracts (Wilson, 1997; Miravete, 2007). This literature shows that the gains of finely sorting consumers by providing many contracts that approximate the profit-maximizing non-linear schedule are marginal. The issue is slightly different in the case of concert pricing because the distribution of seats is given and the only issue is whether to sell different seats at the same or at different prices. The return to price discrimination depends not only on the heterogeneity in consumer preferences, but also in the (exogenously given) seating experience. Offering multiple ticket prices may raise profits even if all consumers are identical. This is not the case in the standard model of second-degree price discrimination à la Mussa and Rosen (1978). As mentioned above, artists do not fully exploit the opportunities offered by second-degree price discrimination.

To our knowledge, no studies have been done on the use of third-degree price discrimination in the context of the concert tour industry or, in any market, on the joint use of second- and third-degree price discrimination. The literature on industrial organization has studied the two pricing questions independently (Stole, 2007). This is not because the issue has no empirical relevance. In fact, most firms that sell vertically differentiated products do so in multiple markets. Such firms apply second- and third-degree price discrimination simultaneously, charging different menus of prices in different markets. However, under the classical approach, there is no theoretical reason why the two decisions should be linked. Indeed, the second- and third-degree price discrimination literatures have no overlap.

A behavioral approach, however, can establish links between the two decisions. Kahneman et al. (1986) argue that community standards of fairness prevent sellers from increasing prices in response to positive demand shocks. Such a constraint on the sellers’ ability to fine-tune pricing may apply to both second- and third-degree price discrimination. Alternatively, sellers may be subject to biases or personal styles, as we argue shortly, and such biases may apply to all pricing choices. A novel aspect of our work is to show that second- and third-degree price discrimination are linked empirically, and to suggest that they are linked through the identity of the sellers.

13.2.2.2 Rationing

Happel and Jennings (2010) list several explanations for the prevalence of rationing for live concerts. Broadly speaking, these explanations belong to one of two categories depending on whether the argument is based on classical economics or whether it also includes some psychological elements. Consider explanations based solely on classical economics. The main reason for rationing is that concert demand is subject to a great deal of uncertainty. Prices have to be set in advance before knowing many of the variables that influence demand.

Uncertainty alone, however, cannot explain why some artists systematically sell out the first days that tickets are offered for sale. It is possible that when artists first offer tickets for sale, they do not know what the demand for the concert will be on the event date. However, how could they have such poor information about contemporaneous market demand and fail to learn from past mistakes? Classical economics has offered other explanations that address this fact. One is based on the observation that most performing artists care about their reputation. Empty seats may reveal negative information about the tour that could damage the artist’s eminence and ability to sell tickets in the future. If concert-goers systematically substitute away from those artists who do not sell out, it may be rational for all artists to underprice because none of them wants to fall victim to a negative information spillover.

There are, however, other features that are specific to the industry. Producing a successful concert involves managing a coordination game between fans with important consumption externalities and informational asymmetries. Concert attendance is a joint consumption good and also an input of production (Busch and Curry, 2010). Becker (1991) has argued that due to consumer externalities, the demand for concerts may be upward sloping at least for some range of prices. DeSerpa and Faith (1996) refine the argument to explain excess demand for concerts. Another type of explanation is based on the relationship between ticket sales and other markets. Underpricing secures a full house, which increases ancillary sales on the premises. There are also complementarities between concert sales and the sales of recorded music that may justify keeping prices low (Krueger, 2005). Artists may therefore choose to subsidize tickets to increase consumption in other markets. However, while this explains selling below monopoly price, it does not offer a rationale against market clearing. It does not explain large excess demand for tickets that results in rationing and high prices on the secondary market.

A second class of explanations is based on the psychology of concert fans. One argument is based on the idea that ticket pricing is subject to norms of fairness. Kahneman et al. (1986) have argued that considerations of fairness play a large role in ticket markets to justify price compression. Fans have implicit contracts with artists that give entitlement to affordable prices. Artists who violate these norms may be subject to antagonism and withholding of demand. This view is consistent with the fact that high ticket prices receive ample coverage in the media. If the media is more likely to pick on unfair prices, charging excessive amounts can backfire and trigger a consumer boycott (for a discussion of these issues, see Courty and Pagliero, 2010).

Happel and Jennings (2010) have argued that underpricing generates goodwill and that consumers reciprocate in other markets (recordings, ancillary products, endorsement) as they would in a gift exchange. They also propose another behavioral argument. Frenzies associated with rationing may produce an aura of scarcity that drives the fear of rationing and exclusion. Consumers want to be among the happy few who get tickets. Artists may gain in the long run from creating such psychological pressure.

There is very little evidence in support of these explanations. In fact, there is not even systematic evidence that rationing prevails in the concert industry. The underpricing debate is fueled by anecdotal evidence and lacks systematic examination. There is little doubt that some artists (e.g. Bruce Springsteen) sell out most of their concerts. In addition, these artists seem to underprice some concerts. Consumers have to line up (or wait on the phone), tickets sell out very quickly, and some tickets are subsequently offered online at much higher prices. These observations suggest that some artists leave surplus to consumers (or resellers). The fact that brokers and scalpers make large profits in resale markets is consistent with the underpricing hypothesis.

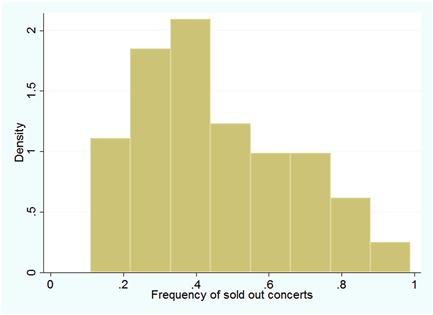

However, there are also counter-arguments to the hypothesis that tickets are systematically underpriced. It could be that brokers enter the market because artists use very coarse seating categories. Since consumers strictly prefer the best seats in a given category, these seats have to be underpriced in order to sell the worst seats. This alternative hypothesis is consistent with the fact that brokers trade in the best seats in each section (Leslie and Sorensen, 2009). In addition, rationing does not necessarily mean that artists leave money on the table. Courty (2003) has argued that artists may not be able to capture the profits from resale that are captured by brokers. More to the point, rationing is common but not at all pervasive. On the one hand, 40% of pop concert tickets were routinely unsold in 2011 (The Economist, 2011). On the other hand, our data reveals that 42% of concerts by the top 100 pop artists were sold out between 1992 and 2005. The debate on underpricing is still open. This is partly due to the challenging task of proving that artists charge prices that are substantially lower than the profit-maximizing prices (Connolly and Krueger, 2006).

13.2.2.3 The Artist’s Objective Function

Sellers in the performing arts may have non-standard objective functions. They may not care solely about maximizing profits as in the standard classical framework. For example, artists may care about their fans out of altruism. Pro-social attitudes could play a role in explaining pricing decisions. Artists do not underprice out of fear of consumer retaliation, as in Kahneman et al. (1986), but because they may be willing to forego some profit to make sure that the event remains affordable to certain subgroups of fans. Obviously, both motives may be at play.

As argued earlier, the assumption that artists have pro-social preferences is difficult to distinguish from the alternative hypothesis that artists are strategic. A strategic explanation typically assumes that fans’ preferences have some behavioral component (e.g. consumers care about fairness or are loss averse) and pricing is used to manipulate fans’ willingness to pay. Most of the industrial organization literature on pricing has focused on behavioral consumers and maintained the assumption that firms rationally maximize profits (Ellison, 2006, see also Spiegler, 2011, for a review). A strategic explanation, however, has difficulty explaining large differences in pricing choices across sellers.

An alternative approach is to assume that there is some heterogeneity in how sellers set prices. There are two main ways to proceed. Sellers may have behavioral preferences that influence pricing decisions (e.g. pro-social preferences as described above). Classical theory has traditionally not paid much attention to such a possibility. The argument against doing so is that market competition will eventually eradicate these differences because it will drive inefficient practices out. However, this argument does not apply to the concert industry because sellers earn substantial rents and can afford to forgo some profit opportunities. In the concert industry, differences in seller preferences may explain some differences in pricing styles.

Another possibility is that decision makers are subject to behavioral biases. There is some recent evidence that supports this assumption. Bertrand and Schoar (2003) and Malmendier et al. (2011) use datasets on top officers of large corporations and demonstrate the existence of manager styles. They show the existence of individual fixed effects that are correlated across a wide variety of financial decisions. They attribute these differences to individual specific life and career paths, such as early life experience and MBA education. The interesting point is that seller heterogeneity survives in a context where one would assume that market selection is vigorous. If top managers influence management practices, it is not unreasonable that rock celebrities may also influence pricing decisions.

These two arguments suggest that the existence of pricing styles is not entirely implausible. Artists may form preferences over pricing decisions in the same way that managers have preferences over financial decisions. Moreover, artists have a tremendous control over prices, and widely different views about their relations and responsibility toward fans and society. Some artists say that they care about fairness and affordability, but not all do. In addition, there is much heterogeneity in how much artists invest in their public image and care about their celebrity status.

13.2.3 Summary and Questions to be Addressed

The pricing of tickets offers an ideal case study to investigate standard questions in industrial organization (monopoly pricing, price discrimination), but with several twists due to the emotional nature of the product (musical performance), the special relationship between buyer and supplier (fan-idol), and the role played by the media in influencing the demand for top artists (celebrity status). The following questions are open:

• How often do artists price discriminate? Do demand and product characteristics explain the use of price discrimination as standard theory predicts? Is the use of second- and third-degree price discrimination connected?

• How often are concerts sold out? Do demand and product characteristics explain the use of rationing? Do artists leave money on the table by underpricing?

• Do artists differ in pricing styles? What behavioral considerations influence artist pricing? Do artists have different objective functions?

The rest of this chapter presents a detailed analysis of price discrimination and rationing. We identify several puzzling features of the data and propose a unified framework based on the concept of artist pricing styles to explain these puzzles.

13.3 Data and Summary Statistics

This study focuses on the primary market for concert tickets, with data from two sources. The core of the data was collected by Billboard. It covers the same set of concerts and contains variables similar to those of Connolly and Krueger (2006), who used data from Pollstar instead. We supplemented this data with additional information on artists and tours from a wide range of sources.

13.3.1 Data

Our data identifies the main parties involved in organizing a concert (artists, venue, and promoter), with the exception of the agent, whose role is limited to putting artists and promoters in touch. For each concert defined by the date, venue, and artist(s), the Billboard dataset reports the promoter in charge, ticket prices, venue capacity, attendance, and the revenue realized. One main shortcoming of this dataset is that it does not have information on tours. We gathered that information from band and fan websites. In addition, we gathered information on the characteristics of the bands from music websites, artist websites, and the Rolling Stone Encyclopedia of Rock and Roll.

Our resulting panel data is thus three-dimensional. The first dimension describes the product (i.e. a concert) and can be aggregated by music genre, artist, or tour. The second dimension describes the local demand and can be aggregated at the level of city or state. In addition, knowledge of the venue where the concert takes place provides information about both product (venue characteristics) and demand (through location) characteristics. The third dimension is time.

There are several differences with respect to the Connolly and Krueger (2006) dataset. In terms of depth, our data is richer in several dimensions: (i) we observe all of the prices for each concert, rather than just the highest and lowest, and (ii) we know whether a concert is part of a tour and, if so, what tour it belongs to. This additional information allows us to provide a much more complete picture of the pricing strategies across seating categories and also across venues by comparing only concerts that belong to the same tour (with the same product offered in different local markets). In terms of breadth, our dataset covers fewer artists and fewer years. Still, we cover a large fraction of the industry measured in value terms for the years in our sample.

13.3.2 Scope and Representativeness

Our sample includes all concerts collected by Billboard given by the top 100 grossing artists over the period 1992–2005. Billboard collects data on most concerts offered by our sample of artists in North America. We checked this by sampling a few tours, for which we collected the exact tour schedule from the artist’s website and matched it with the concerts reported in our database. In terms of breadth, our sample represents the majority of the industry in value terms. If we increased the sample to include the top 500 grossing artists over the same period, for example, the top 100 artists would represent 70% of the total revenue. Obviously, the sample covers only a small fraction of all performing artists. For our purpose, however, the pricing policies in our sample are representative, in value terms, of the average ticket sold in North America. That being said, our selection rule draws only from the superstars. The industry distinguishes between new performers and established artists. Established artists have more bargaining power over their promoters. They also probably have more market power to set prices.

A few entries in our sample include multiple artists who often tour together (e.g. Billy Joel and Elton John, Bob Dylan and Paul Simon). We treat each of these artists as one artist when they tour alone and as another when they tour together. Hence, we have a total of 122 different artists. In the rest of this chapter, the term artist (or act) may refer to an individual, a band, or a set of these systematically touring together.

Table 13.1 presents some descriptive statistics. Our sample contains 122 artists, 779 tours, and 20 362 concerts. There are 1561 concerts given on average each year.4 Most concerts in our sample were given as part of a tour. The average number of artists performing in a given year is 57 and this number does not vary much across years (the minimum is 42 and the maximum 67). The average artist gives seven tours and 167 concerts in our sample period with respective medians of 5 and 151. The majority (75%) of artists give at least two tours. The average tour has 24 concerts with a median of 18 and a standard deviation (SD) of 22. There is variability in the number of concerts per tour, but half the tours have between 8 and 34 concerts.

Table 13.1

Summary statistics: concerts, artists, tours, cities, venues, and promoters.

Statistics based on 20 362 concerts performed by 122 artists, in 579 cities, between 1992 and 2005; 18 798 concerts were part of one of the 779 tours. The total number of promoters is 464. The number of venues per city includes venues used at least once in each city.

Concerts are given in 579 different cities throughout the United States. For half these cities, all the concerts are hosted in the same venue. For the other cities, there is much variation in the number of venues used. The overall average number of venues per city is 2.8 and the maximum is 25.

The tours in our sample are large multi-million-dollar operations. Each concert is associated with a promoter. There are 464 promoters in our sample. Table 13.1 presents the distribution of the number of concerts organized by each promoter. The median promoter organizes two concerts and there is much variation across promoters. Clear Channel Entertainment dominates the market (it organizes a bit more than a quarter of the concerts in our sample), but it has many competitors. About 46 promoters organize 67 concerts or more.

13.4 Price Discrimination: Measurement Issues

An act that goes on tour offers the same concert in different cities, with a variety of seating categories in each city. One possibility is to offer all the seats in every city at the same price. Selling all seats in a venue at the same price is called general admission, single-price ticketing, or uniform pricing. Another possibility is to charge different prices for different seats in a given venue and/or different prices in different cities. The former corresponds to second-degree price discrimination: consumers face a menu of seating quality options with different prices. As long as ticket availability is not an issue, they can choose their favorite option. The latter corresponds to third-degree price discrimination, at least as long as arbitrage is not a viable option. This will be the case if fans do not travel to cities where ticket prices are lower – a reasonable assumption if travel costs are much larger than price differences.

In this section, we present different measures of second- and third-degree price discrimination. We distinguish two types of measures that are inspired by past studies of price discrimination in the industrial organization literature (Verboven, 2008). One may measure whether an artist uses price discrimination instead of uniform pricing. In addition, conditional on using price discrimination, one may also measure the extent to which prices vary (Borenstein and Rose, 1994). This can be done both for second- and third-degree price discrimination.

There is a large body of empirical literature investigating whether price differences reflect differences in cost or differences in demand. In these studies, price differences among differentiated products might be due to variations in marginal cost, not just to price discrimination (Shepard, 1991; Clerides, 2004). In our application, however, matters are much simpler because most costs are fixed at the venue level, so cost considerations should not influence pricing decisions. Hence, one can interpret the absence of uniform pricing as price discrimination. This is obvious in the case of second-degree price discrimination: the seating capacity and the distribution of seat quality are given, and the only issue is whether to sell different seats at the same or at different prices.

13.5 Price Discrimination at the Concert Level

13.5.1 Second-Degree Price Discrimination

We identify concerts that use multiple seating categories with a dummy variable:

![]() (13.1)

(13.1)

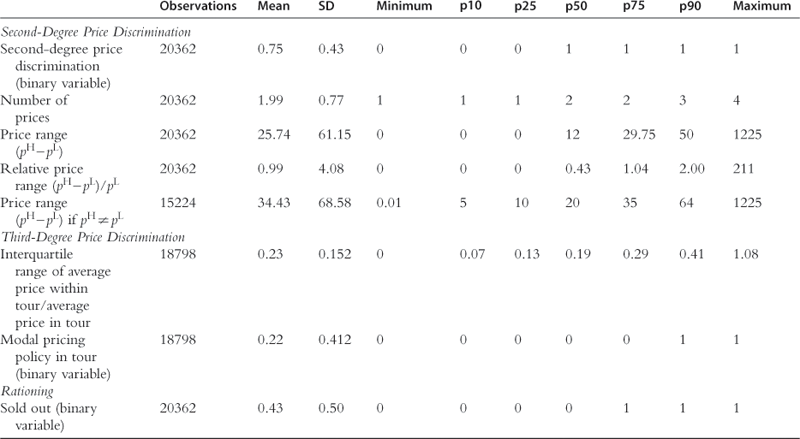

where piH (piL) is the highest (lowest) price for a seat in concert i. Table 13.2 presents summary statistics on price discrimination. In our sample, second-degree price discrimination is used in 75% of the concerts. The dummy variable di measures the existence of price discrimination, but does not take into account the number of seating categories or the price difference between seating categories. The number of seating categories per concert ranges from 1 to 4 with an average of 1.99. Overall, 56% of the concerts offer two price categories, 25% one, 15% three, and the remaining 4% four categories.

Table 13.2

Summary statistics (price discrimination and rationing): concert-level data.

Statistics based on 20 362 concerts, of which 15 224 used more than one price category and 18 798 were part of a tour. The second-degree price discrimination binary variable is equal to 1 if a concert has more than one price category. The modal pricing policy binary indicator is equal to 1 if a concert uses the combination of prices that is most common within a tour. The sold out binary variable is equal to 1 if the concert is sold out.

We next report some statistics on the intensive margin of second-degree price discrimination. We measure the maximum differences in price for seats in the same concert. The average price range (piH – piL) is about $25.74. After normalizing by the low price, (piH – piL)/piL, we get an average of 0.99. Top seats cost on average twice more than the worst ones. This figure, however, hides much heterogeneity. As reported above, piH – piL is equal to 0 for 25% of the concerts. The price range piH – piL grows to $34.43 for concerts in which piH ≠ piL. In addition, the quality premium is extremely high for a few concerts.

The three measures of price discrimination (price discrimination dummy, number of prices, relative price range) are positively correlated with very low p-values. In the rest of this chapter, we will often conduct the empirical work using the price discrimination dummy because it is simpler to manipulate (e.g. than the number of prices) and easier to interpret (e.g. than the price range, which has an arbitrary component to the extent that concerts may use different venue splits). However, the results still hold using alternative measures of price discrimination.

13.5.2 Third-Degree Price Discrimination

We measure third-degree price discrimination at the tour level, since concerts in a tour are virtually identical (same stage, musicians, and set of songs). Rental and labor costs can vary from one city to the other. The largest fraction of these costs, however, is highly inflexible at the venue level since the only choice variable that is costly to adjust is the number of shows offered in a given venue. However, most tours offer a single show in most cities visited. For the sake of conciseness, we do not discuss in detail the case of multiple concerts given in the same city.5

Conditional on visiting a city, the price of tickets should depend only on demand factors (local public) and on venue characteristics, in particular total capacity. If price discrimination takes place, we would expect prices to vary from city to city as long as there are important variations in public demand across cities. The only reason for a lack of variation in prices is the implausible scenario that differences in audiences are exactly compensated for by differences in venue characteristics.

To measure third-degree price discrimination, we define a concert pricing policy as the number of seating categories and the price for each seating category. For each tour, we record the pricing policy used in each city. We say that uniform pricing is used for a set of cities if the pricing policy does not vary across the cities in that set. The reader should keep in mind that the terminology ‘uniform pricing’ means different things for second- and third-degree price discrimination. The correct interpretation, however, will be clear from the context.

There is no single method of measuring uniform pricing at the tour level. We propose two measures. The first computes the fraction of concerts within a tour that use the modal pricing policy, which is the pricing policy most frequently used within a tour. On average, 22% of the concerts use modal pricing (Table 13.2). This is the average across all tours, of the proportion of concerts that use the same pricing policy as the tour modal policy. This high figure could be driven by tours with few concerts. For these tours, a high proportion of concerts may use the modal policy even though the actual number of concerts with identical policies is low. This is not the case. For example, the proportion of concerts that use the tour modal pricing policies does not decrease when we restrict the sample to tours with at least 10 concerts.

The median number of concerts per tour is 18. If each concert within a tour were priced differently (a different number of seating categories or different price for at least one seating category) the fraction of concerts using the tour mode would be 5.5%. The much higher figure of 22% suggests that uniform pricing across cities plays a large role in the concert industry.

Our second measure computes the Gini–Simpson homogeneity (or concentration) index for the set of pricing policies in a tour. This is the probability that two concerts drawn randomly from a tour use the same pricing policy. It can be written as:

![]()

where t denotes a tour, i denotes a pricing policy within a tour, ni,t the number of concerts in tour t using pricing policy i, and Nt the number of concerts in tour t. Let N denote the total number of concerts in our sample. On average across all tours, the probability that two concerts in a tour use the same pricing policy, G = Σt(Nt/N)Gt, is 7.4% (Table 13.3). If all concerts in a tour sharing the same pricing policy used the modal policy, we would expect the Gini index to be around 4.8% (0.22 squared). The fact that it is much higher says that uniform pricing at the tour level is not just due to modal pricing.

Table 13.3

Concentration (or homogeneity) of pricing policies.

| Partitioning the Sample by | Gini–Simpson Index |

| Tour | 0.074 |

| Artist | 0.026 |

| Promoter | 0.021 |

| Venue | 0.015 |

| City | 0.008 |

| Year | 0.005 |

| All data (no partitioning) | 0.002 |

The table reports the mean probability that two concerts selected randomly within a tour, artist, promoter, city, year, or in the whole sample have the same pricing policy (i.e. the same number of pricing categories and the same prices).

One concern with our measures of price discrimination is that some pricing policies may just happen to be the same by chance. A second concern is that identical pricing policies may be associated with venues or with promoters rather than tours. Table 13.3 reports the Gini–Simpson index for different partitions of our sample. Note that the Gini–Simpson index is at least three times higher for tour partitions than for any other partition (venue, artist, year, city, or promoter). This indicates that uniform pricing occurs mainly at the tour level, confirming the validity of our measure of third-degree price discrimination.

There are many different measures of the extent of third-degree price discrimination. We compute the interquartile range of prices within a tour for the lowest, mean, and highest price. To illustrate these concepts, assume for the sake of argument that tours use a single seating category. The interquartile price range in tour t is (pt75 – pt25), where pt75 is the price that corresponds to the 75th percentile of prices in tour t and similarly for pt25. This measure provides information on how much prices vary across cities within a tour. The interquartile range provides a more robust measure of variability of prices than SD, for example, because there are outliers. On average across all tours, the interquartile range of the lowest price is $7.5, of the mean price $8.3, and of the highest price $9.4. Table 13.2 shows that the interquartile range of the mean price is about 23% of the average price within a tour.6

Our measures of third-degree price discrimination are correlated, and the correlation is statistically significant at conventional levels. Most interestingly, the tours that use less modal pricing also vary prices less across cities. There is no clear reason why this should be the case. Something common to all concerts in a tour probably influences several pricing decisions. In Section 13.9, we will see that artist pricing styles can rationalize these correlations.

13.5.3 Summary

We have defined two sets of measures for second- and third-degree price discrimination. The first set measures the existence of price discrimination. The second set measures the intensive margin of price discrimination (differences in price). We find that price discrimination is often but not always used. Uniform pricing is also common, although not as common as price discrimination. The next section shows that there is considerable variation in the use of price discrimination across artists.

13.6 Price Discrimination at the Artist Level

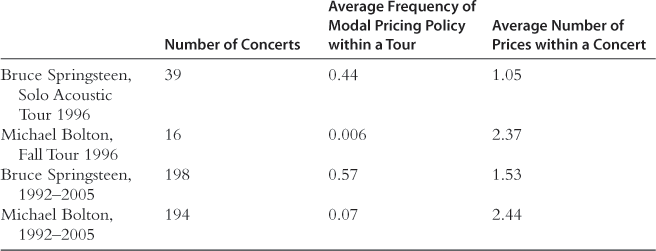

Artists do not price concerts in the same way. Figures 13.1 and 13.2 illustrate the point with two tours by two different artists. The two figures describe ticket prices for Bruce Springsteen’s ‘Solo Acoustic Tour’ and Michael Bolton’s ‘Fall Tour 1996’. Both tours took place in 1996 and both artists are American rock singer-songwriters born around 1950. Figures 13.1 and 13.2 report the prices for different seats in a given venue (points on a vertical line), and for the different cities visited in a tour (different dates on the horizontal axis).

The use of price discrimination varies greatly across these two tours. Two patterns are worth noting:

• There is essentially only one seating category (on average 1.05) in the Bruce Springsteen tour (Fig. 13.1), while there are typically multiple seating categories (on average 2.37) in the Michael Bolton tour (Fig. 13.2), with significant variability in price within a venue (the highest price in a concert can be up to 200% higher than the lowest price). Bruce Springsteen rarely uses second-degree price discrimination while Michael Bolton often does so.

• Most prices are equal to one of two values ($30 or $33) across locations for Bruce Springsteen’s tour, while they vary greatly for Michael Bolton’s tour. The fraction of concerts that use the modal pricing policy is 44% and 0.6%, respectively (Table 13.4). The differences in pricing patterns for these two tours are remarkable.

Why do Bruce Springsteen and Michael Bolton choose such different policies? Before we attempt to address this question we provide more systematic evidence that the use of price discrimination varies greatly across artists. In fact, Figs. 13.1 and 13.2 report only one tour for each artist. To start, we should investigate if the patterns presented in Figs. 13.1 and 13.2 are not specific to the two tours we selected. Table 13.4 also considers other concerts given by these two artists. We find that Bruce Springsteen uses fewer seating categories than Michael Bolton (1.53 against 2.44 on average across the 198 and 194 concerts in our sample period) and varies price less within a tour (on average 57% of Bruce Springsteen’s concerts are identical to the tour modal pricing policy versus 7% for Michael Bolton). Bruce Springsteen and Michael Bolton seem to price concerts very differently. Is this typical just of these two artists?

The rest of this section documents the existence of differences in the use of price discrimination across artists. In Section 13.7, we will use a simple model to investigate candidate explanations for these differences.

13.6.1 Second-Degree Price Discrimination

Table 13.5 reproduces Table 13.2, but at the artist level. To illustrate the difference between these two tables, consider our measure of second-degree price discrimination. Here, the unit of observation is an artist. Denote E(di|a) the mean value of di across all concerts offered by artist a where di is defined by Eq. (13.1). This is a measure of an artist’s propensity to use second-degree price discrimination. Table 13.5 presents summary statistics of the variable E(di|a). On average, artists use second-degree price discrimination 77% of the time. This figure is similar to the same figure for the entire sample of concerts (Table 13.2). The new information is found in the next columns of Table 13.5 which report statistics on the variability across artists. These statistics differ greatly from Table 13.2, which reported statistics for the entire sample.

Table 13.5

Summary statistics (price discrimination and rationing): artist-level data.

The table reports the artists’ average propensity to price discriminate and sell out. The statistics are based on 122 artist-specific mean values for second-degree price discrimination and rationing, 108 for third-degree price discrimination. The second-degree price discrimination variable is the proportion of concerts by a given artist with more than one pricing category. The frequency of modal pricing policy is the proportion of concerts by a given artist that uses the combination of prices that is most commonly used within a tour. The sold out variable is the proportion of sold out concerts by a given artist.

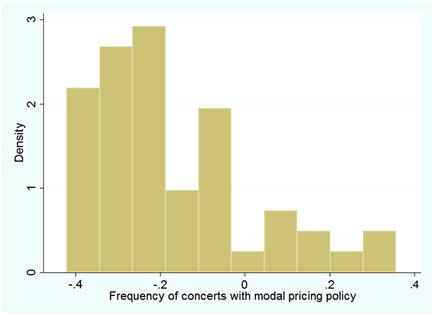

There is a large SD (26%) in artists’ average use of price discrimination. The range across artists is also very large. Billy Joel uses price discrimination in 4% of his concerts, Garth Brooks in 8%, and KORN in 22%. However, Madonna, the Eagles, and Pink Floyd almost always price discriminate. Figure 13.3 plots the distribution of E(di|a) for our sample of 122 artists. The height of the histogram corresponding to x on the horizontal axis, for example, measures the fraction of artists who use uniform pricing about x% of the time. The spread of the density mass is distributed across the two extremes of 0 (never use second-degree price discrimination) and 1 (always use it). This confirms that there is much variation across artists in the use of price discrimination.

Going back to Table 13.5, 10% of the artists use price discrimination in at most 38% of their concerts. At the other extreme, a quarter of the artists almost always use second-degree price discrimination (in 97% of their concerts or more). The same holds if we look at the average difference between the highest and lowest priced seats. Ten percent of the artists set an average price premium of 15% or less. At the other extreme 10% of the artists set an average price premium of 214% or more.

13.6.2 Third-Degree Price Discrimination

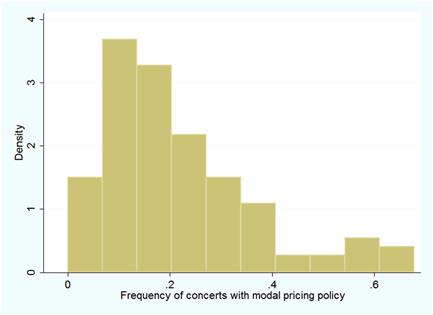

Table 13.5 also reports statistics on our measures of third-degree price discrimination averaged at the artist level. Again, the means do not change much. For example, artists use the modal pricing policy on average for 22% of their concerts (no change in the mean relative to Table 13.2). What is relevant for us are the statistics on the distribution across artists. The SD across artists in the use of modal pricing is 15%. There are on average 80 tours per artist. If modal pricing were random across artists, the use of modal pricing would average out at the artist level around the sample value of 22% and we would expect to observe little variation across artists in the use of modal pricing. This is not the case.

This is confirmed by Fig. 13.4, which reproduces Fig. 13.3 for modal pricing. Again the density mass is spread across the 0–1 interval. About 25% of the artists use modal pricing on average in less than 11% of concerts, while 10% use modal pricing in 47% of concerts or more. Consider the distribution of Gini–Simpson coefficients across artists. There is a great deal of heterogeneity across artists in the chance that any two concerts in a tour are equally priced. The SD across artists in the Gini–Simpson coefficients is 0.10 (recall that the average Gini–Simpson coefficient across all tours was 0.074). For 10% of the artists, the probability that two concerts in a tour use the same prices is 20% or higher. At the other extreme, 10% of artists never set the same price for any two concerts in a tour.

Figure 13.4 Third-degree price discrimination: the distribution of artist-specific average proportion of concerts with modal pricing policy.

The same conclusion holds when we look at the intensive measures of third-degree price discrimination. Ten percent of the artists have an interquartile range of the average price that is 11% of their average tour price; while at the other extreme, 10% of the artists have an interquartile range that is 41% of the average tour price. The amount of price variation across cities within a tour varies greatly across artists.

13.6.3 Summary

There is much heterogeneity in the extent to which artists use second- and third-degree price discrimination. This is true for our binary indicator for uniform pricing and also for the measures of price discrimination that take account of differences in prices.7 This confirms that the difference between Bruce Springsteen and Michael Bolton is not specific to these two artists. In the next section, we investigate possible explanations for the observed differences in pricing across artists.

13.7 Identifying Artists’ Pricing Styles

Differences in pricing across artists may be due, for example, to the fact that artists play different music, in different venues, in different years, and in front of different audiences. Such heterogeneity could play through different channels. One channel considered in the industrial organization literature is that competition may vary across markets. As argued earlier, we do not believe this to be a major issue in the concert industry, but we can empirically investigate this possibility by controlling for city and year fixed effects. However, we believe that there are other channels that are more relevant in our application.

The return to price discrimination may vary from one concert to the other. To see how this could generate differences in our measures of price discrimination across artists, it helps to step back and ask the question of when price discrimination is expected to be used according to the existing theoretical literature. In a frictionless world, a profit-maximizing artist always price discriminates, at least as long as consumers have preferences for seat quality (second-degree) or as long as the public differ across cities (third-degree). There is no obvious reason for why this should not be the case.

If there is a fixed cost associated with the implementation of price discrimination, however, some artists may find it more profitable to use uniform pricing. In practice, artists have to do some research to adjust ticket prices to local market conditions. In the case of second-degree price discrimination there are also costs associated with ticketing and enforcing that each attendee sits in the assigned seat. Hence, the return from implementing price discrimination may not always justify the costs. Variations in the return from price discrimination or in the implementation cost may explain why price discrimination is not always used.

We can now return to our interpretation of the finding that pricing practices vary across artists. To avoid confusion, in the rest of the chapter we use the term pricing practice to say that our measures of price discrimination vary across artists. We use the terminology pricing style to say that individual artists deliberately price concerts differently, as a result of, for example, differences in objective functions or individual skill endowments.8

Evidence of differences in pricing practices does not necessarily imply the existence of pricing styles. It is also consistent with the existence of unobserved demand and product heterogeneity correlated with artist unobserved characteristics. To clarify the distinction, consider a simple thought experiment. Say one observes differences in pricing decisions across sellers and wants to find out whether these differences are due to individual pricing styles. The dream experiment for testing this hypothesis would be to ask each seller to set prices for the same set of goods. Doing so, one would hold constant demand and product characteristics; hence, the variability in pricing practices would have to be attributed to individual styles. Unfortunately, in our dataset each concert is a unique pricing problem. We can, however, try to hold constant concert characteristics as much as possible, in an attempt to investigate the role of individual pricing styles.

This section presents a simple theoretical framework to show that under fairly general assumptions on the structure of demand, we can interpret differences in pricing practices (after controlling for demand and product characteristics) as evidence of artist pricing styles. To be clear, field data cannot provide definite evidence of artist pricing styles as in our thought experiment. This is because one cannot fully rule out the possibility of unobserved demand or product heterogeneity that is correlated with artist-specific characteristics. Still, in Section 13.8 we go a long way towards decomposing the variations in pricing choices that can be attributed to demand heterogeneity and individual pricing styles.

In Section 13.9, we follow a second approach to demonstrate the existence of pricing styles. We investigate whether artists are biased in a systematic way for different pricing choices. We argue that any systematic artist-specific bias is consistent only with individual pricing styles. The case is convincing if the decisions that are found to be associated have no reason to be connected according to classical theory. This delivers a powerful test in our application because there is no reason for which the decision to second- and third-degree price discriminate should be correlated across artists.

13.7.1 Theoretical Framework: When Should Artists Use Price Discrimination?

Assume an artist sells tickets to two different audiences. The tickets could be for the same concert in two different venues or for two different seats for the same concert. Accordingly, the public could live in two different towns or buy two different types of seating categories. In this latter interpretation, we make the simplifying assumption that consumers are interested in only one seating category. Allowing for the possibility of substitution across seating categories adds realism, but does not change our main conclusions.

The inverse demand by consumer c = 1,2 for seat category c and for artist a is P(q|c,a) = αc,a – βq. The marginal cost is χ (typically small or zero in the concert industry). We assume that differences across consumers and artists can only influence the intercept αc,a. This is to establish a benchmark; later we will revisit this assumption.

Under price discrimination, the artist chooses prices in order to maximize q(αc,a – βq – χ) in each market. Profits from audience c are (1/4β)(αc,a – χ)2. Under uniform pricing, overall profits are (1/8β)(α1,a + α2,a – 2χ)2. The increase in profits, or the return from price discrimination, is:

![]()

where F is the fixed cost of implementing price discrimination. Consider the benchmark case where the demand intercept for a concert performed by artist a in front of audience c is additively separable.

Additivity assumption: αc,a = αa + αc.

The net profits from price discriminating simplify to R = (1/8β)(α1 – α2)2 – F.

Proposition 1 is important for two reasons. (i) Artists are expected to use price discrimination when there is enough difference across audiences. For example, they should use second-degree discrimination when seating categories are perceived to be sufficiently different. This could stem from physical differences in seating categories within a venue or heterogeneity in willingness to pay for seats of different quality. Similarly, they should use third-degree price discrimination if the local audiences where the tour stops are sufficiently different or if the venues are sufficiently different. (ii) The decision to price discriminate does not depend on the characteristics of the artist that equally affect all consumers. Proposition 1 says that we should control for demand shifters that influence quality differences or difference in willingness to pay for quality. After controlling for product and demand shifters, the decision to price discriminate should not depend on the artist’s identity as long as the additivity assumption holds.

13.7.2 Summary

Proposition 1 helps interpret the results presented in the previous section. For example, the differences across artists in the use of second-degree price discrimination could be rationalized if artists perform in front of different audiences with different willingness to pay for seating quality. The differences in the use of third-degree price discrimination could be rationalized if artists tour different subsets of cities. Coming back to Figs. 13.1 and 13.2, it could be that Michael Bolton visits very different cities and performs in venues with very heterogeneous seating experiences, while Bruce Springsteen tours similar cities and books venues where all seats are similar.

The next section initially assumes that the additivity assumption holds, and investigates whether the variations in the use of price discrimination can be explained by demand and product characteristics. In the rest of the section, we relax the additivity assumption and consider a number of other explanations for the variations in artist pricing practices.

13.8 Candidate Explanation for the Use of Price Discrimination

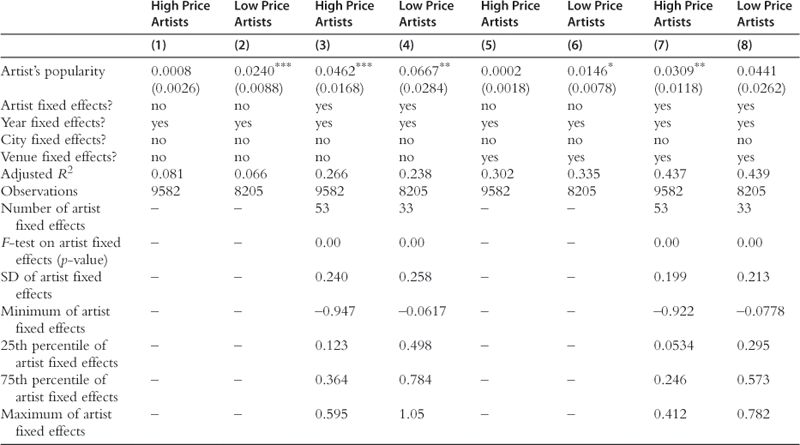

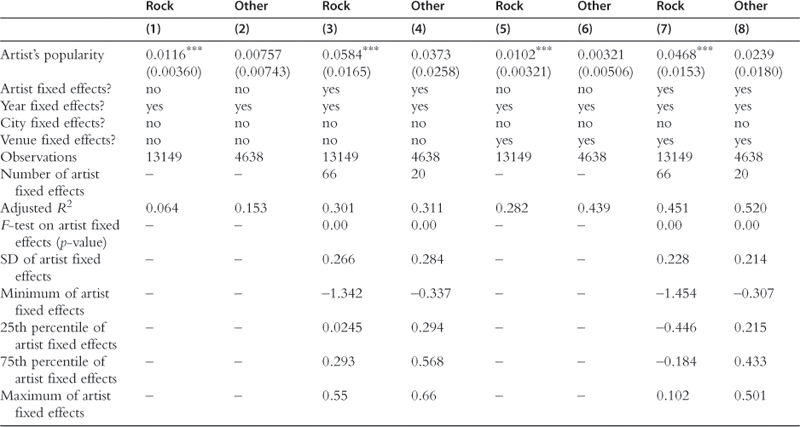

13.8.1 Second-Degree Price Discrimination

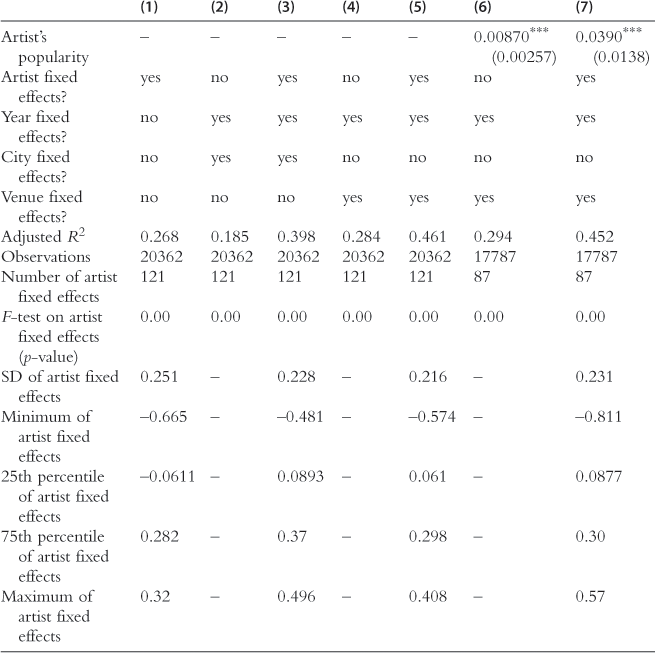

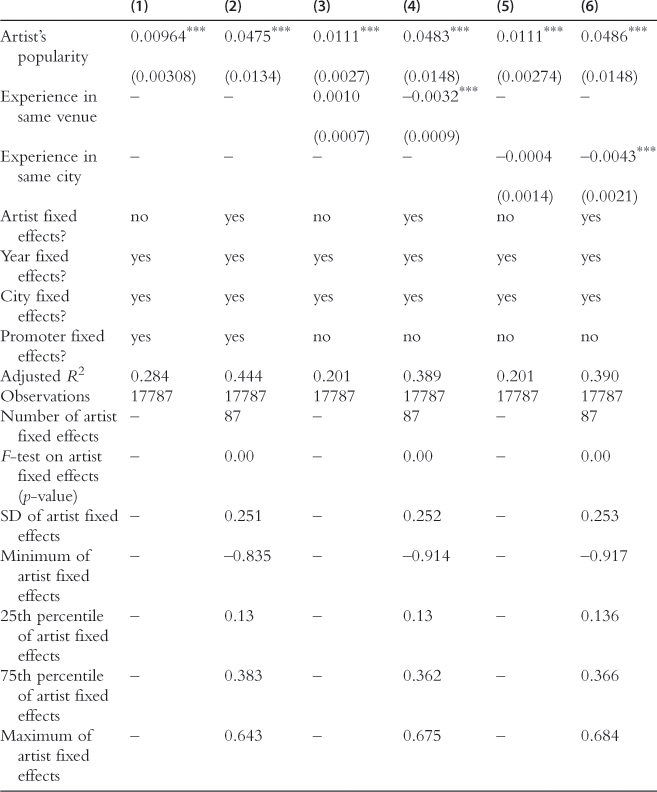

We propose to explain the decision to price discriminate with controls for demand, product heterogeneity, and artist fixed effects. Assuming that the additivity assumption holds, we follow the empirical methodology proposed by Bertrand and Schoar (2003) to identify the existence of managing styles. In a nutshell, we estimate artist fixed effects θartist from model:

where θcity denotes city fixed effects that control for differences in local audiences and for differences in venue characteristics for all the cities where there is a single venue (more than half the cities in our sample), θvenue denotes venue fixed effects that control for venue characteristics more precisely than city fixed effects do, θyear denotes year fixed effects that control for changes over time in public taste, public preferences for seating quality, or in the cost of implementing price discrimination, Popularitya,y controls for heterogeneity in artist popularity as we will explain shortly. City and year fixed effects control for unobserved differences in the level of competition across cities and over time.

We estimate Eq. (13.2) using a linear probability model, instead of a non-linear model (logit or probit). This is without loss of generality in a saturated model where all right-hand side variables are dummies or categorical. The fitted probabilities are simply the conditional probability of using second-degree price discrimination within each cell defined by the different values of the dummy variables.9

Like Bertrand and Schoar (2003), we look at three sets of statistics: changes in adjusted R2 associated with the artist fixed effects, F-tests that the artist fixed effects are equal to 0, and summary statistics on the distribution of the artist fixed effects.

We can answer several questions:

• Do the controls increase the explained variation in the use of price discrimination? According to Proposition 1, the answer should be yes if the controls capture relevant variations in demand and product characteristics.

• Does the addition of control variables decrease the explanatory power of artist fixed effects? This should be the case if the artist heterogeneity documented in Section 13.6 is caused by heterogeneity in demand or product characteristics. We can answer these two questions by looking at changes in adjusted R2 and testing the significance of artist fixed effects.

• After including the control variables, what fraction of the variation in price discrimination is attributed to the artist fixed effects (i.e. artist pricing styles)? The distribution of the artist fixed effects gives some information on the economic magnitude of heterogeneity across artists.

Table 13.6 reports the results. Column (1) shows that artist fixed effects explain 27% of the variations in the use of second-degree price discrimination. Column (2) shows that year and city fixed effects explain about 18% of the variations in the use of price discrimination. The adjusted R2, however, goes from 18% to 40% as we add artist fixed effects (move from column (2) to column (3)). This shows that the variations explained by city and year fixed effects are to a large measure orthogonal to the variations explained by artist fixed effects.

Table 13.6

Artist effects on second-degree price discrimination.

The table reports ordinary least-squares (OLS) estimation results. The dependent variable is the second-degree price discrimination binary variable, equal to 1 if a concert has more than one price category. Artist’s popularity is the cumulative number of singles and albums in top charts in previous years (time varying for each artist). In computing the statistics for the estimated artist fixed effects, each artist fixed effect is weighted by the inverse of its standard error to account for estimation error. Robust standard errors in parentheses, clustered at the artist level. ***p < 0.01, **p < 0.05, *p < 0.1.

Note that artist fixed effects are economically highly significant in the sense that they explain a large fraction of the variations in price discrimination. This result will remain in all our specifications. In contrast, manager fixed effects in Bertrand and Schoar (2003) explain only 4% of the variations in corporate behavior.

The bottom of Table 13.6 shows statistics on the distribution of the artist fixed effects. The SD of estimated artist fixed effect is 0.25, which is very close to the 0.26 figure in Table 13.5, as can be expected. The SD corresponding to Table 13.6, column (3) is only slightly lower than in Table 13.6, column (1). The percentile estimates change very little.

We repeat the same exercise in Table 13.6, columns (4) and (5), with venue fixed effects instead of city fixed effects. The conclusion remains the same. The adjusted R2 increases from 28% to 46% when we add artist fixed effects (compare columns (4) and (5)). Interestingly, year and venue fixed effects explain about 10% more of the variations than year and city fixed effects (compare columns (2) and (4)). This suggests that venue fixed effects capture some variations in product characteristics.

We conclude that local market characteristics and venue characteristics explain a large portion of the variations in the decision to second-degree price discriminate – a finding consistent with Proposition 1. Still, even after controlling for these potential sources of unobserved heterogeneity, the proportion of variation in the use of price discrimination explained by artist fixed effects does not decrease much. In fact, Fig. 13.5 reproduces Fig. 13.3, but using the estimated fixed effects of the specification controlling for venue and year fixed effects. If local market and venue characteristics explained much of the variability across artists in the decision to price discriminate, then heterogeneity across artists, captured by the range of the distributions, would decrease after controlling for venue and year fixed effects. This is not the case. Heterogeneity in pricing styles still seems to play an important role.10

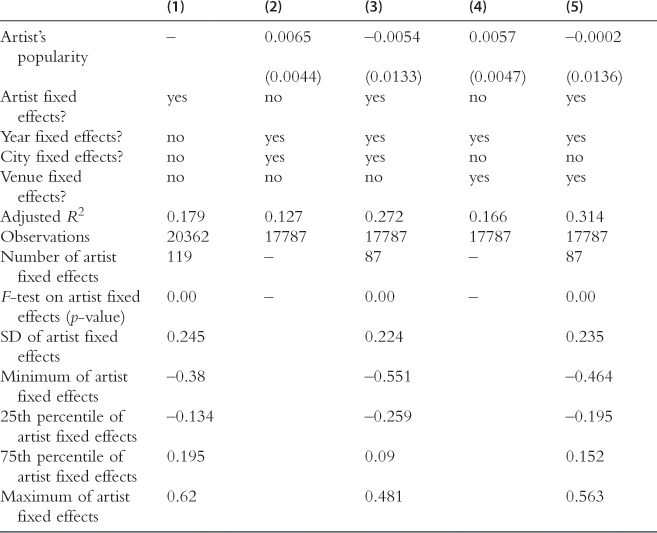

13.8.2 Third-Degree Price Discrimination

In the case of third-degree price discrimination, Proposition 1 says that we should control for the fact that different tours stop in different subsets of markets with possibly different venue characteristics and local audiences. Holding the set of cities within a tour constant should go a long way toward controlling for the mix of audience and venue characteristics. However, there are 579 cities in our sample and no two tours visit the same set of cities. One option would be to focus on the set of most visited cities. However, doing so would still leave many differences in the set of cities visited across tours.

We cannot use our measure of third-degree price discrimination computed at the tour level and also hold the set of cities visited constant. Therefore, we instead leverage the fact that there are many individual cities that are visited by a large fraction of tours. The nuance is that each city is visited by a slightly different subset of tours. Instead of measuring price discrimination at the tour level, we consider pairs of cities. For each pair, we can identify those artists who use the same pricing policy in the two cities and those who do not. We then aggregate this information across all pairs of cities and compute differences in pricing style across artists after holding city-pairs constant.

The exact procedure is as follows. We first select the top 10 cities most visited and form the 45 possible city-pair combinations. For each pair, we construct an observation for each tour that visits that pair of cities. We construct a variable that is equal to 1 if the two pricing policies for that tour are identical and equal to 0 otherwise. This produces a dummy variable describing uniform pricing that assumes the value of 0 or 1 each time one of the 779 tours in our sample stops in one of the 45 possible city-pairs. The dummy variable for uniform pricing is equal to 1 in 16% of these observations. In Table 13.7, we explain the variation in this dummy variable with artist fixed effects (column (1)), with city-pair fixed effects (column (2)), and both sets of fixed effects (column (3)). The adjusted R2 with artist fixed effect alone is 0.18 (column (1)), and with city fixed effect alone it is 0.14 (column (2)). The first result is consistent with our earlier finding that there is much heterogeneity across artists in the use of third-degree price discrimination. In fact, the SD of the artist fixed effects is 0.19.11 The second result is consistent with Proposition 1 stating that the use of third-degree price discrimination should depend on differences in local market characteristics. City-pair dummies control for differences in audience and venue characteristics. Price discrimination should be more likely to take place in pairs of heterogeneous cities. Most interestingly, the 18% figure is identical to the increase in adjusted R2 when we add in column (3) the artist fixed effect to the city fixed effects (0.32 – 0.14 = 0.18).

Table 13.7

Artist effects on third-degree price discrimination for city-pairs.

The table reports OLS estimation results. An observation describes a pair of cities (among the top 10) in which an artist performed a concert within the same tour. The dependent variable is an indicator variable equal to 1 if the two concerts have identical pricing policy. The model identifies 53 artist fixed effects. In computing the statistics for the estimated artist fixed effects, each artist fixed effect is weighted by the inverse of its standard error to account for estimation error.

Table 13.7 also presents summary statistics on the artist fixed effects. We find no decrease in the SD of the artist fixed effects after controlling for differences in local market characteristics. The SD of the artist fixed effect is 0.19 in columns (1) and (3). There is significant heterogeneity across artists. The probability that two concerts have the same pricing policy in the same pair of cities varies by 0.77 across all the artists in our sample. Figure 13.6 reproduces Fig. 13.4, but by using the estimated artist fixed effects from Table 13.7, column (3). The spread of the distribution does not change much relative to Fig. 13.4.

Figure 13.6 Third-degree price discrimination: distribution of estimated artist fixed effects in regression with city-pair fixed effects.