CHAPTER SEVENTEEN

Understanding Financial Services

CHAPTER STRUCTURE

Section I Non-Banking Financial Company

Section II Venture Capital and Private Equity

Section VIII Alternative Investments

Section IX Consumer Rights and Protection Applicable to Financial Services

Annexures I

KEY TAKEAWAYS FROM THE CHAPTER

- Non-Banking Financial Company (NBFC) does not include any institution whose principal business is of agriculture activity, industrial activity, sale or purchase or construction of immovable property. It cannot accept deposits and cannot issues cheques. Under automatic route, 100 per cent FDI is permitted.

- With effect from December 6, 2006, they are classified as Asset Finance Company, Investment Company, Loan Company and Infrastructure Finance Company.

- Venture capitalist provides funds to new start-ups facing the problem of lack of funds.

- Against providing, they take some ownership rights of the business entity.

- There are five stages in VC Seed, Early Stage, Formative Stage, Later Stage and Last Stage.

- PE acquires mostly 100 per cent of the company (large investments), whereas VCs acquire 50 per cent of the company (new business start-ups).

- Credit card transaction is divided into two parts—one is authorization (when issuer bank authorizes the transaction after swipe of the card) an other is clearing and settlement (when the merchant is paid for the sale).

- Interchange fee is around 1–2 per cent of the transaction value.

- The purpose of a housing finance system is to provide the funds which home-buyers need to purchase their homes.

- Housing finance market’s performance and changes are routinely monitored.

- HF is considered one of the leading indicators of economic development.

- Securitization is a process through which an issuer creates a financial instrument by combining other financial assets and then marketing different tiers of the repackaged instruments to investors.

- Reverse mortgage is a financial product accessible for senior citizens who own a house. It facilitates them to mortgage their property with a lender and convert fraction of the home equity into tax-free income.

- An Underwriter is an Investment firm that plays the role of liaison between the organization selling its shares/securities and the investing public.

- Underwriter purchases shares from corporation and sells it to investors.

- Underwriters mostly make money from the spread between the price paid by investors and price paid to issuers. There are two main types of underwritings:

- Firm commitment underwriting (underwriter buys the entire issue)

- Best efforts underwriting (underwriter does not bear the risk of unsold shares)

- Microfinance includes farming, trifling trade, livestock, food processing, vending, smallscale labour incentive productions like weaving, craft, artisans, street vendors, small shops, services, etc.

- Microfinance is often confused with Microcredit. Microcredit is a subset of Microfinance.

- A pension scheme is simply a saving scheme with deferred return as the source of saving.

- Pension schemes that are arranged by government for the entire or segment of labour force are referred to as social security schemes.

- Schemes arranged by employers or other organizations are referred to as employer pension schemes.

- Commodities, Hedge funds, Real assets, Private equity, Structured products are the examples of alternative investment and they acts as a tool to diversification.

- Hedge funds can be defined as privately organized investment vehicle that generates investment opportunities by leveraging.

- Consumer protection consists of laws and organizations designed to ensure the rights of consumers as well as fair trade competition and the free flow of truthful information.

- The Banking Codes and Standards Board of India (BCSBI) develops standards, enhances transparency and improves relations between banks and customers.

SECTION I

NoN-BANKiNg FiNANCiAl ComPANy

A Non-banking Financial Company (NBFC) is a company registered under the Indian Companies Act, 1956, and is engaged in the business of loans and advances, acquisition of shares/stock/bonds/debentures/securities issued by the Government or a local authority or other securities of marketable nature, leasing, hire-purchase, insurance business, chit fund business, but does not include any institution whose principal business is that of agricultural activities, industrial activities, sale/purchase/construction of immovable properties. A non-banking institution which is a company with its principal business of receiving deposits under any scheme/arrangement/ any other manner, or lending in any manner is also considered as a non-banking financial company (residuary non-banking company).1

Most of the functions of NBFCs are akin to that of banks; however, there are a few differences:

- NBFC cannot accept demand deposits. Demand deposits are funds deposited at a depository institutions that are payable on demand, immediately or within a defined short notice like current or savings account.

- NBFC is not a part of the payment and settlement system. Therefore, NBFC cannot issue cheques drawn on it.

- Deposit insurance facility of Deposit Insurance and Credit Guarantee Corporation (DICGC) is not available for NBFC depositors, unlike in case of banks.

Hundred per cent FDI is permitted under the Automatic Route subject to minimum capitalization norms of:

| FDI Stake | Minimum Capitalization |

|---|---|

| Up to 51 per cent | USD 0.5 mn; to be brought upfront |

| Above 51 per cent and up to 75 per cent | USD 5 mn; to be brought upfront |

| Above 75 per cent | USD 50 mn; USD 7.5 mn; to be brought upfront and balance in 24 months |

NBFCs registered with RBI were classified as:

- Equipment leasing company is any financial institution whose principal business is that of leasing equipments or financing of such an activity.

- Hire-purchase finance company is any financial intermediary whose principal business relates to hire-purchase transactions or financing of such transactions.

- Loan company means any financial institution whose principal business is that of providing finance, whether by making loans or advances or otherwise for any activity other than its own (excluding any equipment leasing or hire-purchase finance activity).

- Investment company is any financial intermediary whose principal business is that of buying and selling of securities.2

However, with effect from December 6, 2006, the NBFCs registered with RBI have been reclassified as:3

- Asset Finance Company (AFC)

- Investment Company (IC)

- Loan Company (LC)

- Infrastructure Finance Companies (IFC)

Asset Finance Company (AFC) Can be defined as any company which is a financial institution carrying on as its principal business ‘financing of physical assets supporting productive/economic activity’ such as automobiles, tractors, lathe machines, generator sets, earth moving and material handling equipments, moving on own power and general purpose industrial machines.

Principal business for this purpose is defined as aggregate of financing real/physical assets supporting economic activity and income arising there from is not less than 60 per cent of its total assets and total income respectively. They are further classified as those accepting deposits or those not accepting deposits.

Investment Company (IC) Is a company which is a financial institution carrying on as its principal business ‘acquisition of securities’.

Loan Company (LC) Means any company which is a financial institution carrying on as its principal business ‘providing of finance whether by making loans or advances or otherwise for any activity other than its own’ but does not include an Asset Finance Company.

Infrastructure Finance Companies (IFC) Are in long term funding for developing or operating and maintaining or developing, operating and maintaining any infrastructure project in road, highway, port, airport inland port, waterways, water supply, irrigation project, water treatment, sanitation and sewage system or solid waste management, telecom services (basic or cellular), network and internet services, transmission or distribution of power, laying down and maintenance of gas, crude oil and petroleum pipelines.

The above-mentioned types of NBFCs are further classified into:

- NBFCs accepting public deposit (NBFCs-D)

- NBFCs not accepting/holding public deposit (NBFCs-ND)

Funding sources of NBFCs include debentures, borrowings from banks and FIs, Commercial Paper and intercorporate loans.

NBFCs are typically into funding of:

- Construction equipment

- Commercial vehicles and cars

- Gold loans

- Microfinance

- Consumer durables and two wheelers

- Loan against shares, etc.

List of major products offered by NBFCs in India are:

- Funding of commercial vehicles

- Funding of infrastructure assets

- Retail financing

- Loan against shares

- Funding of plant and machinery

- Small and Medium Enterprises Financing

- Financing of specialized equipment

- Operating leases of cars

Funding transactions of banks have inbuilt exposure on corporate; whereas in case of NBFCs, the benefit is that in most of the transactions, there is exposure on the asset and not on the corporate. Also, NBFCs are able to provide fund to non-banking regions (or where banks are not aggressive due to various constraints and reasons) on providing financial assistance. Thus, NBFCs have an edge over banks.

NBFCs have been playing a very significant role both from the macroeconomic perspective and the structure of the Indian financial system. With the gamut of services, they account for around 9 per cent of financial sector assets, have become an integral part of the financial system in India, playing a crucial role in broadening access to financial services, enhancing competition and bringing in greater risk diversification4. This intricate participation calls for strict vigilance and policy checks. Gaps in the regulation of the non-banking financial sectors are being continuously identified and plugged and the oversight mechanism strengthened. In cognition of the risks posed to the banking system on account of their exposure to NBFCs extending gold loans, exposure limits of banks to NBFCs have been tightened while loan to value (LTV) ratios have been prescribed on gold loans extended by NBFCs5.

SECTION II

VENTURE CAPiTAl ANd PRiVATE EqUiTy

During your market research and analysis, you come up with innovative idea of software that can bridge the gap in university communication system. Filled with zeal, you design a prototype with two other friends. But when it comes to developing the running actual software, you need to hire developers/programmers, invest on hardware and development software. Arranging money for this becomes a big challenge. To pursuit your idea, you need source of financing. Approaching bank may come up as a spontaneous solution, but banks need assets for security, but you need finance to purchase those assets. In order to come out of this deadlock, you need OPM (other people’s money) who are willing to invest on your idea being the only asset. Venture Capital market is the answer to this search for investment and capital.

The term, ‘venture capital’ generally refers to financing for new, often high-risk ventures. Venture capital funds pool investors’ cash and loan to start-up firms and small businesses with perceived, longterm growth potential. In exchange of the high risk that venture capitalists assume by investing in smaller and less mature companies, they usually gain significant control over company decisions, in addition to a significant portion of the company’s ownership (and subsequently value). For start-ups that do not have access to other capital, venture capital is a highly significant source of funding and it typically entails high risk (and potentially high returns) for the investor. The underlying sources of funds for venture capital firm include individuals, pension funds, insurance companies, large corporations, and even university bequest funds6.

FIGURE 17.1 BASIC FLOW OF FUNDS—IN AND OUT OF A VENTURE CAPITAL COMPANY.

Stages in Venture Capital (VC) Investing

Angel investors are individuals who help entrepreneurs get their businesses off the ground, and earn a high return on their investment. Mostly, they are the bridge for self-funded entrepreneurs that take their business ahead to the stage that they need venture capital. They typically offer expertise, experience and contacts in addition to money.

Stage 1: Seed: Seed-stage financing is the first stage, often involving a modest amount of capital provided to entrepreneurs to finance the early development of a new product or service. These early financings are infused for product development, market research, building a management team and developing a business plan. Seed-stage financing company has not actually set up operations yet, and R&D is the major cost centre.

Stage 2: Early Stage: For companies at a stage wherein they are able to begin operations but are not yet at the stage of commercial manufacturing and sales, early stage financing supports a step-up in capabilities. Business, being new, can consume vast amounts of cash at this stage.

Stage 3: Formative Stage: Financing includes both seed stage and early stage.

Stage 4: Later Stage: Capital provided after commercial manufacturing and sales have embarked on, and before any initial public offering falls in this stage. The operations have begun; product or service is in production and is commercially available. The company exhibits noteworthy revenue growth, but may or may not be showing a profit.

- Third Stage: Capital provided for major expansion such as physical plant expansion, product improvement and marketing.

- Expansion or Mezzanine Stage: Financing refers to the second and third stages.

- Bridge Financing: Finances the step of going public and represents the bridge between expanding the company and the IPO.

Stage 5: Balanced-stage: This refers to all the stages, seed through mezzanine7.

Private equity consists of investors and funds that make investments directly into private companies or conduct buyouts of public companies that result in a delisting of public equity. Capital for private equity is raised from retail and institutional investors, and can be used to fund new technologies, expand working capital within an owned company, make acquisitions, or to strengthen a balance sheet.

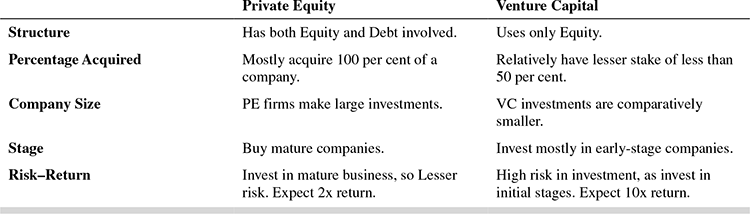

Venture capital is a subset of private equity. Therefore, all venture capital are private equity, but not all private equity are venture capital.

TABLE 17.1 DIFFERENCES BETWEEN PRIVATE EQUITY AND VENTURE CAPITAL8

FIGURE 17.2 ROLE OF VENTURE CAPITAL AND PRIVATE EQUITY IN BUSINESS LIFECYCLE.

SECTION III

CREdiT CARdS

Selling goods or services on credit, relying on the credibility of the consumer has been a custom of merchants since past. This practice has been mutually beneficial for both the merchant and the consumer. Introduction of credit cards has been an extension of this idea, with better defined terms and conditions and involving regulatory bodies for vigilance.

Credit Card is a card issued by a financial company giving the holder an option to borrow funds. Credit cards charge interest and are primarily used for short-term financing9. They are issued by banks or credit unions, and have shape and size according to the specification of ISO/IEC 7810 standards as ID-1 (defined as 85.60 × 53.98 mm in size)10. Credit cards are usually used at point of sale. This plastic card entitles its holder to buy goods and services based on holder’s promise to pay for these goods and services availed now, in near future. It is also known as ‘Plastic Money’.

Institutions issuing these credit cards need to use with due diligence while processing the applications of consumers. The critical step in the process is credit history check. This mainly includes validating the consumer’s ability to repay debts based on the responsibility and sincerity demonstrated in repaying previous debts. Though this check is not a guarantee that similar response would be repeated in future transactions too, it provides a primary check when carried meticulously. The consumer’s credit report thus prepared contains information, like number and types of credit accounts, duration for which each account has been opened, amount of available credit used and whether bills are paid on time. Information regarding whether the consumer has any bankruptcies, liens or judgments are also a part of the report that supplements the decision whether to extend credit to that consumer and also the credit limit to be granted.

Major Parties Involved in Credit Card Transaction

- Cardholder: Owner of credit card, who uses it to make a purchase of goods or services.

- Merchant: The individual or business who accepts credit cards for payment of the product or services sold to the consumer or cardholder.

- Issuer Bank11: The responsibilities of issuer bank are majorly administrative. The functions it handles covers various aspects of cardholder relationship, including card marketing, credit processing of applications, card issuance, cardholder billing, payment collection from cardholder, fraud control, collection from defaulters, and so forth.

- Acquirer Bank: Receiving side of the transaction, i.e., Merchant is managed by acquirer bank. It is the financial institution accepting payment on behalf of the merchant.

Operations of processing and reconciling all the credit transactions made at merchant’s end are also acquirer banks’ responsibility. They perform sales and marketing functions too by soliciting and signing up new merchants. Merchant’s application processing and authorization is done by acquirer bank. Institutions like J P Morgan Chase, Bank of America, HSBC, etc., are the bigger players in this role, accompanied by many more.

- Credit Card Association: Association of issuer banks like MasterCard, Visa, American Express, etc., is made to monitor, control, and manage transaction terms for all parties involved in transaction (merchants, issuer banks, acquiring banks).

- Transaction Network: It is the technology part of the transaction that enables the electronic transaction.

Working of Credit Cards

FIGURE 17.3 CREDIT CARD TRANSACTION PROCESSING DIAGRAM12

The credit card transactions can be majorly divided into two parts:

- Authorization: It is the process that happens immediately after each purchase transaction. Once the card is swiped at register for payment, issuer bank authorizes the transaction by validating the card and its outstanding limit.

- Clearing and Settlement: This is the second part of transaction cycle, wherein merchant is paid for the sales. Issuer bank gets interchange fee13, and acquirer bank earns discount fee as their share of profit in the transaction.

A typical credit card transaction involves the following steps:

Step 1: Consumer swipes his card at POS for payment of the purchases made.

Step 2: An intermediary, Authorize.Net, supports the intricate routing of data forward for authorization and processing.

Step 3: The secured transaction network passes the information via defined connection and finally submits the transaction information to the credit card network (like Visa or MasterCard) which further relays the transaction to the issuer bank that issued the credit card to the consumer.

Step 4: The issuing bank either authorizes or declines the transaction based on the customer’s available credit limit and passes the results back to the credit card network which is finally routed to Authorize.net.

Step 5: Authorize.net sends the results of authorization to the merchant and consumer (at website, in case of online transaction).

Step 6: After this authorization, merchant delivers the goods or services to the consumer.

Step 7: The issuer bank sends the calculated funds for the transaction to the credit card network, which passes the funds to the merchant’s bank (acquirer bank). The bank then deposits these funds into the merchant’s bank account. This process is called ‘settlement’.

Respective interchange fee and discount fee are also deducted by issuer bank and acquirer bank. Consumer pays outstanding credit card consolidated bills at defined interval, defined in the terms of contract.

Charges and Profits in Credit Card Transactions

- Issuer Bank: They issue cards to consumers and represent them during transaction. They bear the risk of default that cardholder or consumer might commit. In return, they charge; and therefore are benefitted in case of no defaults by interchange fees (generally 1–2 per cent of the total transaction value14) to merchants with every transaction.

- Acquirer Bank: They are the intermediary between Issuer bank and Merchant. They receive all credit card transactions from issuers, and present all payments in a time period to the merchant in lump sum. In exchange, the acquirer bank charges merchants a fixed amount for its services, as well as a variable sum dependent on the volume of the merchant’s sales15.

SECTION Iv

HoUSiNg FiNANCE

‘The purpose of a housing finance system is to provide the funds which home-buyers need to purchase their homes. This is a simple objective, and the number of ways in which it can be achieved is limited. Notwithstanding this basic simplicity, in a number of countries, largely as a result of government action, very complicated housing finance systems have been developed. However, the essential feature of any system, that is, the ability to channel the funds of investors to those purchasing their homes, must remain.’

Housing Finance in simple terms implies financing or loans for meeting array of needs relating to housing, including:

- Purchase of a house/flat

- Acquisition of land

- Construction/ extension of house/flat

- Renovation, repair or upgradation of house/flat

- Taking over of housing loans from other banks or housing finance companies

Housing finance market’s performance and changes are routinely monitored as it is considered one of the leading indicators of economic development. In case of emerging economies with population growth and rapid urbanization, robust financing systems are required. Considering these issues primarily focussing on growing middle-class, World Bank in its conference in October, 2012 has suggested five key strategic areas (Fig. 17.4) to be worked on17:

FIGURE 17.4 FIVE KEY-STRATEGIC AREAS OF HOUSING FINANCE RECOMMENDED BY THE WORLD BANK.

The aforementioned strategic areas in macro-perspective are intended to bridge the demand-supply gap that exists in the housing and housing finance sector.

Every country has its own regulatory framework and body, with variations in norms depending on the economic condition and demand of the country. National Housing Bank is such apex level institution for housing finance in India. The National Housing Policy, 1988, envisaged the setting up of NHB. NHB was set up in July 9, 1988, under the National Housing Bank Act, 1987. NHB is wholly owned by Reserve Bank of India, with the entire paid-up capital contributed by RBI18. Rural Housing Microfinance launch is one of the major milestones of NHB.

Housing finance sector in India has been growing at a remarkable pace. [Refer Annexure 1.] Indian housing finance has developed from a stage where it was solely government-driven to present stage of growth and multiple players. The structure of the financing system has been cited bellow:

Currently, housing finance in India in the organized sector is provided majorly by following institutions:

- Scheduled Commercial Banks

- Scheduled Co-operative Banks

- Agricultural and Rural Development Banks

- Housing Finance Companies

- State Level Apex Cooperative Housing Finance Societies

Funding Sources of these Housing Finance companies consist of:

- Public deposits

- Term deposits

- Domestic and International Institutional borrowing

- Capital Markets

- Securitization

- Refinance from NHB

Securitization: It is a long-term way of raising resources for housing finance organizations.

Securitization is a process through which an issuer creates a financial instrument by combining other financial assets and then marketing different tiers of the repackaged instruments to investors. The process can encompass any type of financial asset and promotes liquidity in the marketplace.19

Securitization creates liquidity in the market as is makes, otherwise unaffordable, big asset pool of mortgages approachable for retail investors. This also distributes the risks, previously confined to housing sector, among a greater number of players.

The process of processing loan application is tedious and complex for the institutions. For countries, like USA, where such records are centralized and easily available, it is a process driven procedure. Whereas in developing countries, like India, gathering all information of the loan applicant, like outstanding, other loans taken, etc., is slightly complex because of unorganized financial sector. Developing a central repository of this information would bring significant improvement in the process. Easy availability of verified land records and property data is also crucial and inevitable.

Reverse mortgage is a financial product accessible for Senior citizens who own a house. It facilitates them to mortgage their property with a lender and convert fraction of the home equity into tax-free income. They retain ownership of house. Unlike other loans, in this case, the lender makes payments to those senior citizens. There is no compulsion to service the loan as long as the borrower is alive and in occupation of the property. Later, through sale of property, the loan can be repaid.20

SECTION v

iPo (iNiTiAl PUBliC oFFERiNg)

Venture capital and Private Equity supports start-ups in their initial stages to set-up their operations, grow and turn to a profitable venture. Beyond this stage, when a privately held company needs financing to expand its business, or the existing stakeholders want to monetize their investment, they opt for IPO. IPO stands for ‘Initial Public Offering’. An IPO is the first time an organization introduces their shares to general public for sale to outside investors on securities exchange. Companies get an option of raising cash, after IPOS, by trading additional stocks in future.

There is a gamut of activities to be performed before IPO can be executed and after the IPO is offered. These tasks include, among many others, analytical working of the price to be offered, preparing processes and documents for statuary compliances, marketing the new issue, and stabilizing the stock performance after-market offering. These are the key activities performed by Underwriters.

An Underwriter is an Investment firm that plays the role of liaison between the organization selling its shares/securities and the investing public.21

Some of the leading IPO Underwriters are Goldman Sachs, Morgan Stanley, Merrill Lynch.22 Underwriters are the primary players in entire IPO process. Apart from supporting, guiding issuer organization to prepare for IPO, they are meticulously involved in the most critical step of IPO. The basic transaction that happens between issuer/corporation, Investment bank/underwriter and Investor is that underwriter purchases shares from corporation and sells it to investors. Investors pay for these shares to underwriters who further give cash to issuers. Underwriters mostly make money from the spread between the price paid by investors and price paid to issuers, apart from their fee.

There are two main types of underwriting:

- Firm commitment underwriting

- Best efforts underwriting

Firm Commitment Underwriting This is the prevalent type of underwriting, wherein the underwriter buys the entire issue. They take up the full risk and responsibility for unsold shares. They purchase all the shares from organization and sell them to investors at a higher price. So, underwriter makes profit on the spread between price paid to issuer organization and price received from public investors.

Best Efforts Underwriting This underwriter has reduced risks. Though they sell as much of issues as possible, they don’t bear the risk of unsold shares. The unsold issues can be returned to the issuer. Although underwriter doesn’t have financial responsibility for unsold shares, they must make their best efforts to sell the shares at the agreed offering price. In situation where issuer doesn’t find enough investors showing interest at the offered price, they can pull back the offer, as the company won’t make sufficient capital. They would have incurred significant flotation costs.

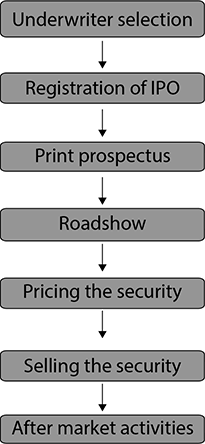

FIGURE 17.6 OVERVIEW OF PROCESSES INVOLVED IN IPO ISSUING PROCESS23

- Underwriter Selection: Once organization decides to go public, they select an underwriter. Selection criteria is based on their experience as underwriters, management fees and other anticipated expenses, proposed roles and strategies and general structure of the deal.

- Registration of IPO: Company needs to register with Public Exchange such as the Securities and Exchange Commission (SEC) in the United States. The issuer firm needs to prepare a registration statement that is to be registered with Public Exchange. The registration statement discloses all material information about the corporation making an initial public offering.

- Printed Prospectus: The prospectus is a legal document describing details of the corporation issuing IPO and also the proposed offering to potential investors. Most of the information in prospectus about the organization is contained in the registration statement. The initial prospectus is also often called a ‘red herring’, because it contains a passage in red that states the corporation is not endeavouring to sell its shares before the registration is sanctioned by the Public Excahnge.24

- Present Road-show: It is more of a marketing, as well as marketing research activity. Road-show is for potential institutional investors. It helps firm to generate interest in investors about the corporation. At the same time, it gives opportunity to firms and underwriters to collect information and interest level of potential purchasers.

- Pricing the Securities: Determining the price of security is instrumental in the success or failure of IPOs. Overpricing would lead to lower acceptance of IPO; thereby, underwriter would be stuck with shares as well as would hit underwriter’s reputation and credibility. Under-pricing on the other hand might bring more investors, but in essence would generate lesser capital than it could have. Issuing firm would bear the burden of expenses associated with IPO, without reaping the possible benefits. The two critical factors in determining the price of IPO are:

- Value of the company

- Expected demand for the securities

- Selling the Shares/Securities: All the possible efforts are done on the effective date of the registration statement. It is a part of underwriter’s duty to ensure that participating investors get their share on the issue date. Securities must be supplemented with a final prospectus.

- After Market Activities: Underwriters are responsible for sustaining and supporting the stock price by trading. If stock prices decline, they purchase the share to control the falling price. Whereas in case stock price goes up, they use over allocation alternative to cover short position. Only after ‘25 calendar days’ of IPO, also known as ‘quiet period’, underwriters and other syndicate members reach a state to analyse and comment on value of firm and convey earnings estimates.

TABLE 17.2 ADVANTAGES/DISADVANTAGES OF IPO

SECTION v I

miCRoFiNANCE

According to estimates, there are 500 million economically active poor people in the world operating microenterprises and small businesses.25 Active entrepreneurs who are running microenterprises not only address unemployment by option of self-employment, but also contributes to the economic growth of the country by increasing per capita income and prudent utilization of unproductive human resource. The lamentable fact is that these microenterprise entrepreneurs always don’t have access to sufficient finance. Though experts in developing and developed nations suggest promotion of self-employment, glaring problem is the inadequacy they face in fixed and working capital. Banks have a constraint as source for them, as banks ask for collateral as a prerequisite, which is not available to microenterprises. The evident resort for them is to avail credit services of local moneylenders and pawnbrokers who ask for high interest rates with stringent rules. Therefore to support self-employment, it gets imperative for government and other agencies to provide financial services to them at a subsidized rate.

Microfinance has evolved with intend to benefit microenterprises, small businesses, low-income households, and thereby support economic development. ‘These financial services may include savings, credit, insurance, leasing, money transfer, equity transaction, etc., that is, any types of financial services, provided to customers to meet their formal financial needs: lifecycle, economic opportunity and emergency’ (Dasgupta and Rao 2003).26 In generic terms, it is financial services in form of small-sized financial transactions for people who fall outside the range of formal finance. Activities that are mostly financed by Microfinancing include:

- In rural areas: Farming, trifling trade, livestock, food processing, vending, small-scale labour incentive production like weaving, craft, etc.

- In urban areas: Artisans, street vendors, small shops, services, etc.

Microfinance is often confused with Microcredit. Microcredit is a subset of Microfinance that includes gamut of activities like savings, insurance, market assistance, technical assistance, etc. Key features of Microfinance can be summed up as:

- Lends to poor

- Doesn’t ask for security or collaterals

- Uses group guarantees and appraisal as a substitute to security

- Gives preference to saving over borrowing

- Loans are short-term

Microfinance, though not restricted, is preferred source for women. Primary reason for this is the available evidences that demonstrate that women are less to default in repayment of loans, than men. The main incentive foreseen in doing so is that development of women has ripple effect on family and eventually on society. Empowerment of women results in improved in nutrition an education of their family, which is also an indirect aim of MFIs. As per the statistics on Nov 5, 2007, since 1996, the World Bank has reached more than 6 million poor in Bangladesh through microfinance projects; 90 per cent of these microcredit borrowers are women. Microfinancing has improved their lives in various aspects:27

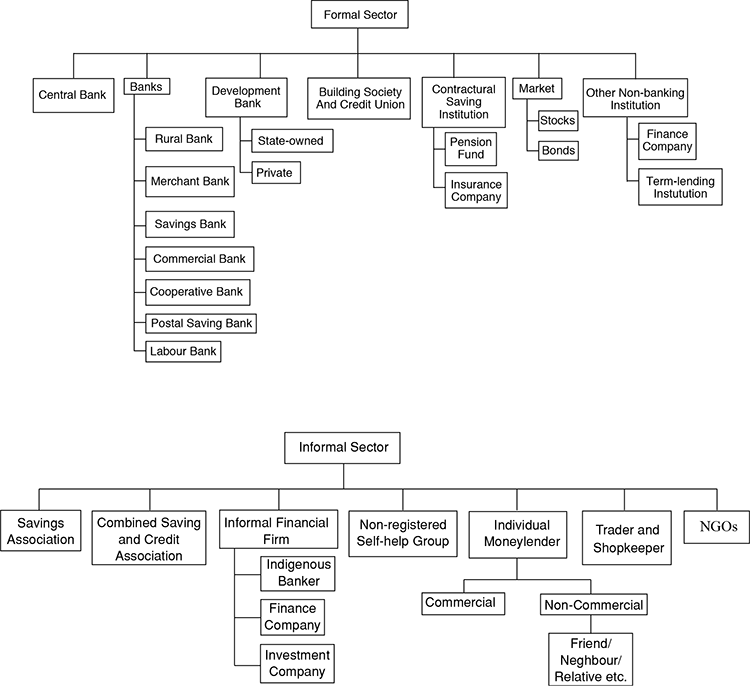

Microfinance programs are financed by loans, grants, guarantees and investments from individuals, philanthropists, social investors, local banks, foundations, governments, and international institutions.28 Major providers of Microfinance are categorized in 3 major categories:

- Formal sector

- Semiformal sector

- Informal sector

Informal sector is also specified in the category because it contributes a descent fraction to microfinance lending, and the drawbacks or limitations of informal lenders have, over a period of time, instigated the need of formal/ semiformal sectors. Few key contributors to Microfinance are:

Grameen Group: Pioneered by Mohammed Yunus in Bangladesh, it targets poor women in rural areas to setup a microenterprise. A bank branch, covering 15–22 villages, is set up with a field manager and bank workers. Their prime objective for successful operations is to develop an understanding of the local environment, clientele and their business. To begin with, they form a group of 5 prospective borrowers, of which 2 are given loan. The performance and loan repayment of these 2 borrowers is observed over a period of time (mostly 50 weeks) to decide the eligibility of other borrowers. Peer pressure and peer support drive these groups.

Rotating Savings and Credit Associations (ROSCAs): It is a type of Combined Saving and Credit Association. It is a group of individuals who unite and make cyclical contribution to a common fund, shared by them all. This fund is given to involved members cyclically, i.e., lump-sum amount of the saving is given to one individual member in each cycle. This amount is paid back in regular monthly contributions.

Self-Help Groups: It’s a voluntary association of 10-20 people, made to attain common collective objectives. It is a homogenous group of people who save portion of their emergent credit needs and revolve resources among the group members. Period and other term of loans are decided by members by consensus. If the group is not formally registered, it should not have more than 20 members.

A slightly detailed sub-categorization of these microfinance providers has shown below:29

Challenges

- The key challenge for lending organization is the Credit Risk involved in these transactions, and various factors that contribute in increasing this risk are:

- Dependency on Seasonality: The traditional activity of agriculture, the major fraction among all, have high seasonal dependency and variation, thereby making loan recovery schedule dependent on these factors, and not on the planning.

- Uncertain Market Conditions: The market, on which borrowers count for to sell their output and repay the loans, has high level of uncertainty of demand, price and competitors.

- Deficiency of Skills: The borrowers take loans for, and are dependent on, one particular skill they possess to repay loans. Failure of that skill to generate desired result would lead neither borrowers nor lenders with alternates.

- Lack of tangible history for income evaluation: Unavailability of income history makes it tough to predict future income.

- It is extremely difficult to monitor the diversion of funds in unproductive activities, instead of purpose loan was taken.

- A main disadvantage to microfinance is that the deal is too small for the lender to devote ample time and money to doing proper due diligence. The smaller deal size makes transaction cost comparatively higher. As the capital is low, the profits are also low.

- Lesser technology and doorstep service for loan initiation and monitoring makes the operational cost very high.

- The inability to reach the poorest of the poor is the biggest challenge and failure of such programs. As Gresham’s law reminds us, if the poor and non-poor are combined within a single program, the non-poor will always drive out the poor.30 To be effective, the system must ensure that it reaches the poor.

- Due to lesser default, women are preferred and targeted over men in microfinancing programs. This may result in men requiring wife to get loans for them.

SECTION vI I

PENSioN FUNdS

When employees reach the end of their working tenure and embark retirement phase, a series of monetary payments are paid to worker or worker’s survivor. Pension funds contribute on large scale to overall institutional investments. For instance, as quoted by Organization for Economic Co-operation and Development, pension fund assets in OECD countries contributes a record value of USD 20.1 trillion in 2011.

A Pension Scheme is the set of financial, administrative, legal, social, and other arrangements established for the purpose of providing pensions to a designated group of workers and their survivors.31

More generally, a pension scheme is simply a saving scheme with deferred return as the source of saving. Pension schemes can be organized in several ways with various organizers including:

- Employer

- Government

- Trade union

- Other type of organization

Pension schemes that are arranged by government for the entire or segment of labour force are referred to as social security schemes. Based on government’s overall fiscal policy as well as actuarial considerations, these schemes are created by, contribution made by and benefits are set by government.

Schemes arranged by employers or other organizations are referred to as employer pension schemes. These schemes are mutual agreements between employees and employer. The terms of such schemes are typically in the form of a legal contract. The terms of these schemes can be altered by mutual consensus of both the parties, by forming a new contract or agreement. Through employment, employees become eligible for participation in employer pension schemes. Employee’s right to pension begins right away, and he/she begins to accumulate or contribute to the fund, but the right becomes vested only after a specified years of employment. After specified time period, the employee becomes eligible to pension benefits.

Pension Schemes are categorized mainly on the type of benefits and contributions:

- Defined-contribution Scheme: In defined-contribution scheme, the employer is obliged by agreement to contribute a definite amount to the scheme on behalf of its employees. Normally this amount is derived as a percentage of the employee’s wages and salaries, but it can be a fixed or variable sum if different formulas are agreed upon for calculation. This amount can be matching employee’s contributions or according to legal limits. Employees also contribute to individual accounts and get tax advantage apart from future savings. The amount contributed by employee is excluded from current taxable income. These contributions are deposited in individual accounts for each employee. Since upon retirement, the employee or survivor receives benefits based on the contribution, employers invest these contributions in long-term financial assets in the meanwhile. These funds are invested in variety of assets, including shares, bonds, other financial assets, land, buildings, and valuables. The pension funds thereby have a liability to provide the committed pension benefits. The counterpart of the liability is a financial asset owned by the employees. This asset and its counterpart liability are classified as insurance technical reserves.

- Defined-benefit Scheme: In defined-benefit scheme, the employer is obligated to provide specific benefits. The level of benefits offered is typically defined by a formula centred on the years of employment, the wages and salaries earned. There is no obligation of contribution on either employee or employer. Either party may or may not make contributions to the scheme. In case contributions are made, the amount deficit to provide an agreed benefit is borne by employer.

Pension Funds in India

Pension funds in India, like in other countries, are structured and controlled by Government Regulatory bodies. PFRDA, established by Government of India on August 23, 2003, is the regulator for the pension sector development and regulation in India.

Pension funds and related norms have modified and improved over a period of time to find justifiable solutions to the problem of providing satisfactory retirement income. One of the major amendment introduced by the New Pension System for the reform was complete shift from a defined benefit pension to a defined contributionbased pension system, making it mandatory for new recruits (except armed forces) from January 1, 2004.32

There are two broad categories of pension schemes in India:

- Tier-I Account: In this option, a contribution of {10 per cent of basic + DA + DP components} in every month is mandatory. Though employees can contribute more than 10 per cent, government’s contribution is 10 per cent. Any withdrawal of saved amount before retirement (at age of 60) is not allowed. These contributions also help in tax advantages as it is exempted from taxable income, subject to certain defined range by government. Once the saving is withdrawn post-retirement, it’s taxable.

- Tier-II Account: It is a voluntary savings facility. Neither does it provide tax benefits, nor there is any restriction on the time period after which withdrawals be done. These savings can be withdrawn on need basis.

SECTION vI I I

AlTERNATE iNVESTmENTS

As is evident from the name, an alternative investment is an investment product other than traditional investments, such as stocks, bonds, cash or real estate. They are mostly short-term investments, unlike traditional sources. These investments include33:

It provides alternate source of investment and acts as a tool of diversification. These investments are expected to have low correlation with traditional financial investments, thereby reducing portfolio risk and diversifying investments. Initially, there was demand of retail investor to get into commodities, but it was difficult. The common way to trade commodities and currencies is through the futures and options market. However, trading futures is much more complicated than the ease of investing in equities. ETPs (Exchange-Traded products) were created with a familiar structure, thereby making investments in commodities and currencies easier to understand and more accessible like stocks.

Exchange Traded Funds: They are shares of a portfolio, not of any individual company. They are traded on stock market as common share.

Commodities

Commodities are raw materials, mostly natural resources that are sold in bulk, like silver, gold, oil, wheat, etc. The items traded as commodities are largely raw materials that are ultimately used to produce other goods. Commodities can be broadly categorised as34:

- Precious metals (e.g., silver, gold)

- Livestock (e.g., cattle, hogs)

- Agricultural products (e.g., wheat, sugar, rice, corn)

- Soft commodities (e.g., coffee, cocoa, cotton)

- Industrial metals (e.g., copper, aluminium)

- Energy commodities (e.g., crude oil, natural gas, gasoline)

Unlike traditional instruments, they cannot be evaluated using CAPM (Capital Asset Pricing Model) or NPV (Net Present Value). It is countercyclical asset, i.e., its performance is reverse of market instruments like bonds and stocks. Commodities and inflation have positive correlation, whereas inflation and stock/bonds have negative correlation. So, commodities help in diversification.

There are various ways of getting exposure to commodity market:

- Spot Market

- Pure Play

- Commodity Futures

- Commodity Indices

- Spot Market: It provides access to either the producer directly, or intermediary. In this case, the investor has to bear the storage cost too. This is feasible for some commodities, like precious metals, but not for all, like gas. It requires full payment at initial level itself. Its storage and other overheads are feasible and under control of investors. These markets provide better hedge against hostile price movements.

- Pure Play: This involves buying shares of the company or organization producing the commodity investor wants to deal with. For example, an investor wishing to trade in natural gas would trade in company producing natural gas. The movement of the stocks of those companies are expected to move in sync with the commodity market. But the assumption has an inherent operational risk of the company and its management’s performance.

- Commodity Futures: These contracts are well-defined standardized agreements. They are backed by faith of exchange on defined terms mentioned in agreement. The future written on these commodities is another way of gaining exposure in commodities. Unlike Spot market, there is no need of full initial payment. Commodity futures require an initial margin only. Depending on direction of spot prices, future calls are determined.

- Commodity Indices: Commodity indices provide access to commodities or commodities of a specific sector. Based on the total return on commodities, Commodity-linked Notes can also possible option to gain exposure in commodity.

Hedge Funds

Hedge funds can be defined as privately organized investment vehicle that generates investment opportunities by leveraging on its less controlled nature, unlike stringent and complicated requirements of mutual funds. They do not perform relative to some specific or index and seek to maximize returns in all market scenarios. Most hedge funds are in the form of either limited partnership or limited liability corporation or offshore corporation. The manager of the fund receives compensation, which has two components—base fee (independent of hedge fund performance) and incentive fee (percentage of the actual return of the fund). Hedge funds can be classified as follows:

- Long/Short: These funds take long and short common stock positions. They are not market-neutral but seek to make profit from greater returns on the long position that on the short positions.

- Market Neutral: They are modified long/short fund as they attempt to hedge against general market moves.

- Global Macro: These funds make bets on the direction of a market, interest rate or such factors.

- Event Driven: These funds attempt to capitalize on some distinctive chances in the market. This may be investment in a distressed company or in a probable merger and acquisition.

Real Assets: This involves direct ownership of nonfinancial assets. These assets have lesser dependence on valuecreating factors, unlike for organizations where management performance and market acceptability determine the valuation. In prior times, land was the only valuable asset. Buying and selling occurs intermittently in local market. Transaction cost involved is comparatively high.

Private Equity: Private equity includes both equity and debt that is not publicly traded. Debt, in short-term, has high risk and thereby cash flow is uncertain. So, in highly leveraged company, debt behaves more or less like equity, especially in short-term. In a typical transaction, a private equity firm buys majority control of a firm, can be mature firm too. This is different from a venture capital wherein the investors invest in young or emerging companies, and seldom gain majority control.

Structured Products: Structured products are synthetic investment tools created to meet definite needs that cannot be met from the standardized financial instruments available in the markets. They can be used to reduce risk exposure of a portfolio or to leverage on the existing market trends. The investment for structured products might focus on a single security, on specific asset classes, or on a related sub-sector. Examples of Structured products are Collateralized Debt Obligation (CDO) and credit derivatives.

SECTION Ix

CoNSUmER RigHTS ANd PRoTECTioN APPliCABlE To FiNANCiAl SERViCES

‘Consumer protection’ consists of laws and organizations designed to ensure the rights of consumers as well as fair trade competition and the free flow of truthful information in the marketplace. Consumer protection laws are government regulations formulated to protect the rights of consumers. The laws are intended to prevent businesses that engage in fraud, scams or unfair practices. Consumer protection can also be asserted via non-government organizations and individuals as consumer activism.

Financial sector has been growing at a fast pace. This growth has led to increase in competition, advances in information technology, which in turn steered devising of highly complex financial products introduced in marketplace. These products demand deep understanding of their operations which is lacking in nascent financial consumers. There is a continually widening gap between the complex financial offering and consumer’s skill to comprehend them. Consumer protection and financial literacy in developing countries are still in their initial stages. This leaves them vulnerable to unfair practices.

Economies of all countries across the world are deeply intertwined. The financial crisis of 2007–09 has been the recent demonstration of this. World Bank has been working upon the issue of Consumer Protection and Financial Literacy for the countries of the Europe and Central Asia Region, since 2005, by a pilot program. World Bank’s analysis suggests that the need for consumer protection arises from an imbalance of power, information and resources between consumers and their financial service providers, placing consumers at a disadvantage. It suggests that a set of good practices should be followed, which requires financial sector players to provide their consumers with:35

- Transparency by providing complete, accurate and simplistic comparable information about the prices, terms and conditions of financial products. The inherent risks should also be disclosed.

- Choice by ensuring impartial, non-coercive and rational practices in the selling and advertising of financial products, and collection of payments.

- Redress by providing economical and prompt mechanisms to address complaints and resolve issues.

- Privacy by guaranteeing control over access to personal information.

Consumer Protection and Regulation in India

Consumer protection in India is shielded by both statutory regulation and voluntary membership bodies (also called consumer activism). Strategic players in consumer protection in India are:36

- Reserve Bank of India (RBI)

- Banking Codes and Standards Board of India (BCSBI)

- Banking Ombudsman

- Indian Banking Association

- Consumer Courts

- Banks with Internal Customer Service Mechanisms

Reserve Bank of India, the main regulator for all financial institutions (like banks, NBFCs), establishes regulation and policy for consumer protection. The policy includes various aspects with provisions on pricing, transparency, recovery methods, and avoidance of multiple-borrowing. Financial institutions, like banks, adhere to these regulations. For instance, the Grievance Redressal Mechanism in Banks of 2008 recommends banks to implement an internal customer service mechanism that accepts and addresses customer complaints and resolves them with an unbiased and competent manner. These RBI guidelines are also specified by the BCSBI. Reserve Bank of India has set up local Banking Ombudsmen in majority of states in India. These Ombudsmen act as impartial watchdogs. In case of consumers’ disputes with banks, these arbiters handle them at an appellate level. These complaints and grievances have either not been fully resolved by the banks or not been satisfactorily resolved in the opinion of the consumer. The Banking Codes and Standards Board of India (BCSBI), started as a collective venture between the banking industry and the RBI in 2005, serves as an autonomous authority for the industry. The BCSBI develops standards, enhances transparency and improves relations between banks and customers. The BCSBI has developed:

- Banking Code Rules—covering member bank obligations to BCSBI

- Code of Bank’s Commitment to Customers Code—covering member bank commitments to customers

The Rules, also mentioned as the Fair Practices Codes, have to be complied by all member banks. The BCSBI also requires all banks to spread information to customers and manages a web-based helpline for customers. On a broader perspective, all those involved with regulation and protection of consumer rights work on set of good practices discussed by World Bank.

CHAPTER SUMMARY

- In NBFCs, most of the exposure is given to assets and it is a great help in non-banking regions.

- NBFCs are also playing a very important role for macroeconomic perspective and Indian financial system.

- NBFCs accounts for around nine per cent of financial assets and is continuously broadening the financial services with bringing in the high competition.

- Gaps in non-banking services are continuously been bridged up to strengthening its potential.

- Venture capitalist deals with the new and small business start-ups and bridges the gap of funds needed.

- VC allows business to open its wings completely by allowing it to execute each and every business activity.

- Private equity players always deal with large investments and mostly take 100 per cent of the ownership. It also helps in making new acquisitions.

- Basically, credit cards help you to buy goods and services even when you do not have money but for that you have to pay a certain amount to your issuer bank.

- A typical credit card transaction involves huge steps which are executed in couple of minutes only.

- Housing finance enables a person to buy, renovate and expand his house. The National Housing Policy, 1988, envisaged the setting up of NHB.

- NHB was set up on July 9, 1988, under the National Housing Bank Act, 1987. NHB is wholly owned by Reserve Bank of India with the entire paid-up capital contributed by RBI. Rural Housing Microfinance launch is one of the major milestones of NHB.

- Housing finance sector in India has been growing at a remarkable pace. Indian housing finance has developed from a stage where it was solely government-driven to the present stage of growth and multiple players.

- As IPO is interest free capital but the whole IPO process is very much expensive. Here, the corporate sectors are not forced to repay the debt but they can put limit on management freedom.

- IPO enhances liquidity for shareholders and investors as they cash out anytime but there is intense pressure on IPO to perform in the short term so that the shareholders can get their profit.

- Though microfinance is developing which is changing and developing business opportunities in context to Indian economy, it has got a lot of challenges also like dependency on seasons where the agricultural activities do not take place throughout the year along with the deficiency of skills as the borrower can only repay when he performs, otherwise he can repay the amount back.

- Pension funds in India, like in other countries, are structured and controlled by Government Regulatory bodies. PFRDA, established by Government of India on August 23, 2003, is the regulator for the pension sector development and regulation in India.

- There are two broad categories of pension schemes in India. Tier-I account in this option is a mandatory contribution of {10 per cent of basic + DA + DP components} in every month. Though employees can contribute more than 10 per cent, government’s contribution is 10 per cent. Any withdrawal of saved amount before retirement (at the age of 60) is not allowed.

- Tier-II account is a voluntary savings facility. Neither does it provide tax benefits, nor there is any restriction on the time period after which withdrawals be done. These savings can be withdrawn on need basis.

- Alternate investment provides alternate source of investment and acts as a tool of diversification. These investments are expected to have low correlation with traditional financial investments by reducing portfolio risk and diversifying investments.

- The Banking Codes and Standards Board of India (BCSBI) started as a collective venture between the banking industry and the RBI in 2005 serves as an autonomous authority for the consumer rights and protection applicable to financial services.

TEST YOUR UNDERSTANDING

- What is a NBFC and how is it different from banks?

- What are the recent classifications of NBFCs under RBI?

- Difference between VCs and PE.

- How the Credit card transaction can be divided?

- What is Securitization and Reverse mortgage?

- Define Underwriters and their role.

- What are the challenges in Microfinance?

- What are the two broad categories of Pension schemes in India?

- Comment on BCSBI.

- What are the advantages of Alternative Investment?

ENDNOTES

- http://www.rbi.org.in/home.aspx

- http://business.gov.in/business_financing/non_banking.php

- http://rbi.org.in/scripts/PublicationReportDetails.aspx?UrlPage=&ID=586#OVE

- http://rbi.org.in/scripts/PublicationReportDetails.aspx?ID=671

- Fundamentals of Corporate Finance, Vol. 1, Sixth Edition, Ross et al.

- CFA Level 1 Study Guide

- http://www.mbaknol.com/business-finance/stages-of-venture-capital-financing/

- http://www.mergersandinquisitions.com/private-equity-vs-venture-capital/

- http://www.investopedia.com/terms/c/creditcard.asp#axzz2E7esUwli on 12/04/2012

- http://www.dimensionsinfo.com/credit-card-dimensions/ on 12/04/2012

- Financial Services, 2E By Gurusamy

- http://www.authorize.net/resources/howitworksdiagram/ on 12/04/2012

- http://www.wikinvest.com/wiki/Interchange_fee on 12/05/2012

- http://www.mastercard.com/us/wce/PDF/MasterCard%20Interchange%20Rates%20and%20Criteria%20-%20April%202008.pdf on 12/05/2012

- http://www.wikinvest.com/industry/Credit_Services on 12/05/2012

- http://www.housingfinance.org/housing-finance/what-is-housing-finance

- http://www.nhb.org.in/AboutUs/about_us.php#Genesis

- http://web.worldbank.org/WBSITE/EXTERNAL/TOPICS/EXTFINANCIALSECTOR/0,,contentMDK:22217029~pagePK:210058~piPK:210062~theSitePK:282885,00.html

- http://www.investopedia.com/terms/s/securitization.asp#axzz2EOf6uMLj

- http://nhb.org.in/RML/RML_Index.php

- http://www.allbusiness.com/glossaries/investment-banker/4944014-1.html#axzz2Eg5TRBcR

- http://www.investopedia.com/terms/l/leadunderwriter.asp#axzz2EgDV7eWy

- http://www.investopedia.com/terms/r/redherring.asp#ixzz2EhC1uOAk

- Introduction to Corporate Finance, by William L. Megginson, Scott B. Smart

- http://external.worldbankimflib.org/uhtbin/cgisirsi/x/0/0/5/?searchdata1=643870%7Bckey%7D#_

- Microfinance: Concepts, Systems, Perceptions, and Impact: A Review of SGSY operations in India, by Soumitra Sarkar and Samirendra Nath Dhar

- http://web.worldbank.org/WBSITE/EXTERNAL/NEWS/0,contentMDK:21153910~pagePK:34370~piPK:34424~theSitePK:4607,00.html

- http://www.grameenfoundation.org/what-we-do/microfinance-basics

- http://www.csa.com/discoveryguides/microfinance/review3.php

- Microfinance Handbook: An Institutional and Financial Perspective: By Joanna Autor Ledgerwood

- http://www.investopedia.com/terms/p/pensionfund.asp#ixzz2FMYXJK9e

- http://www.docstoc.com.lax.llnw-trials.com/docs/1009228/The-Treatment-of-Pension-Schemes-in-MacroeconomicStatistics-a-discussion-paper-by-John-Pitzer-IMF-November-2002

- http://www.pfrda.org.in/indexmain.asp?linkid=100

- CAIA Level I: An Introduction to Core Topics in Alternative Investments, 2nd series, Mark J. P. Anson, PhD, CFA, Donald R. Chambers, Keith H. Black, Hossein Kazemi

- Alternative Investment Strategies and Risk Management, by Raghurami Reddy Etukuru, MBA

- http://siteresources.worldbank.org/INTECAREGTOPPRVSECDEV/Resources/GoodPractices_August2010.pdf