CHAPTER THIRTEEN

Banking Functions, Retail Banking and Laws in Everyday Banking

CHAPTER STRUCTURE

Section II Retail Banking—Nature and Scope

Section III Customer Relationship Management (CRM)

Section IV Laws in Everyday Banking

KEY TAKEAWAYS FROM THE CHAPTER

- Understand the basic banking terms.

- Examine the banking functions and obligations of banks to customers.

- Understand the scope and SWOT analysis of retail banking.

- Information on CBM in banking.

- Examine the laws in everyday banking.

SECTION I

BASIC CONCEPTS

Commercial banking activities can be broadly categorized as retail banking and corporate banking. Retail banking refers to the banking functions undertaken by individuals whereas corporate banking refers to the banking services offered to the firms irrespective of their size (small, medium and large-scale organizations). The distinction has already been elucidated in our earlier chapter on banks’ lending function.

A third type of banking—investment banking—has been in the news during the last two decades. How is investment banking different from retail and corporate banking?

Pure investment banks typically do not accept deposits from or make loans to individuals, as commercial banks do. They provide fee-based financial services such as acting as advisors, managers or underwriters to public share issues, facilitating mergers and acquisitions, corporate restructuring, private equity deals, or corporate bond placements, or acting as brokers/dealers/custodians in the capital markets, and so on.

Negotiable Instruments

Negotiable instruments have a great significance in the modern business world. These instruments have gained prominence as the principal instruments for making payment and discharging business obligations. Negotiation implies transfer by endorsement if payable to the order or by delivery if payable to bearer. ‘Instrument’ implies a documentary means of transferring ownership.

Section 13 of the Negotiable Instruments Act, 1881 defines a negotiable instrument to be ‘a promissory note, bill of exchange or cheque, payable either to order or to bearer’.

The major negotiable instruments are bill of exchange and cheque payable either to order or bearer. For example, when a cheque is transferred to any person, the cheque (instrument) is said to be negotiated.

Bill of Exchange It is an instrument in writing, containing an unconditional order, signed by the maker, directing a person to pay a certain sum of money to a certain person or to the order of that certain person or to the bearer of the instrument (Refer to the Negotiable Instrument Act (N. I. Act), Section 5, India, for more information and also the earlier chapters on bank lending. In the United States, the Uniform Commercial Code Article 3 covers the use of such negotiable instruments.).

Cheque The characteristic features of a cheque can be specified as follows:

- As per the Negotiable Instrument Act, a cheque is a bill of exchange.

- It is always drawn on a bank and is payable on demand.

- It has three parties:

- Drawer: A person who draws the cheque on a bank.

- Drawee: A bank on whom the cheque is drawn.

- Payee: A person to whom the payment is to be made by the bank.

- A cheque can be payable either to order or to bearer.

- When a cheque is crossed, the banker shall not pay the amount over the counter.

- When a payee accepts a cheque and if it is dishonoured, he can claim the money from the drawer.

- A customer has the right to ‘stop payment’ before the due date, after he issues the cheque.

It is a common practice to return cheques where the amount differs in words and figures. The customer is not expected to draw cheques by leaving any blank space that would facilitate insertion of words/figures.

The banker has to cross-check the signature, with the specimen available in the branch, when a cheque is presented for payment.

Difference Between Cheque and Bill of Exchange Every cheque is a bill of exchange. However, every bill of exchange is not necessarily a cheque. The essential differences are as follows:

- A bill of exchange need not necessarily be drawn on a banker.

- A bill of exchange may be payable on demand or payable on a future date.

- A bill of exchange payable on a future date is called usance bill.

Types of Deposits

Deposits1 can be classified into demand deposits and time deposits.

Demand Deposits These are of two types:

- Saving deposits

- Current deposits

- Saving deposits: As saving accounts are meant to encourage savings habit, organizations whose purpose is profit are not allowed to open such accounts. Interest is paid on a half-yearly basis in these accounts. A minimum balance is stipulated by each bank. A balance amount above the minimum stipulated amount is eligible for a 3.5 per cent interest rate in India at present.

- Current deposits: Since this account is to meet the transaction needs of the customer, there is no restriction on the number of transaction in the account or in the type of customers eligible to open these accounts. Account holders are not entitled to any interest from the bank.

Time Deposits These are also called as fixed deposits or term deposits. These are repayable after the expiry of a specified period varying from 7 days to 120 months.

Senior citizens get higher interest rates. Hence, joint deposits with them make sense.

Non-Resident Indian (NRI) Accounts

The present menu of bank accounts for Non-Resident Indians (NRIs) has three categories:

- Non-resident (external) rupee accounts (NRE)

- Non-resident (ordinary) rupee accounts (NRO)

- Foreign currency non-resident (banks) accounts [FCNR] (B)

These accounts can be distinguished as follows:

- While NRO and NRE accounts can be kept in the form of current, savings or term deposit accounts, FCNR (B) deposit can be kept only in the form of term deposits, for periods ranging from 6 months to 3 years.

- Remittances from abroad can be credited to any of these accounts. But earnings of NRIs on the property held by them in India, which are non-repatriable, can be credited only to NRO accounts.

- Money from an NRO account is non-repatriable, but NRE and FCNR deposits are repatriable.

- The entire interest earned on NRO accounts is eligible for repatriation. Persons of Indian nationality who have been NRIs for a period of not less than 1 year and have returned to India are eligible to open a RFC (Resident Foreign Currency) account.

- An NRO account may be jointly held with residents.

- NRE and FCNR (B) accounts cannot be jointly held with residents. But resident power of attorney is permitted for local payments and investments in India.

- Balances held in NRE/FCNR accounts are exempted from wealth tax and interest earned is exempted from income tax. There are no tax exemptions on interest earned on NRO accounts.

Mandates and Power of Attorney

An account holder can appoint a third person to act on his behalf to do certain acts like drawing cheques or instructing bank to debit the account for various purposes like issuance of drafts.

Mandates The following are the salient features of mandates:

- It is an unstamped letter signed by the customer, authorizing a person to operate the account on his behalf.

- Signature of the mandatory should be obtained in the letter of mandate.

- A letter of mandate is generally issued for a short and temporary period.

Power of Attorney The following are the salient features of power of attorney:

- It is a stamped document and generally executed in the presence of a notary/magistrate of a court.

- Two types of powers are granted—special and general powers of attorney. Special power of attorney is often for a single transaction and general power of attorney confers an agent very extensive powers.

Lien Lien is the right of the creditor to retain possession of the goods and securities owned by the debtor until the debt due from the latter is paid. General lien gives a right to possess the goods, banker’s lien adds to it, the right of sale in case of default by the latter. Therefore, it is called an implied pledge.

SECTION II

RETAIL BANKING—NATURE AND SCOPE

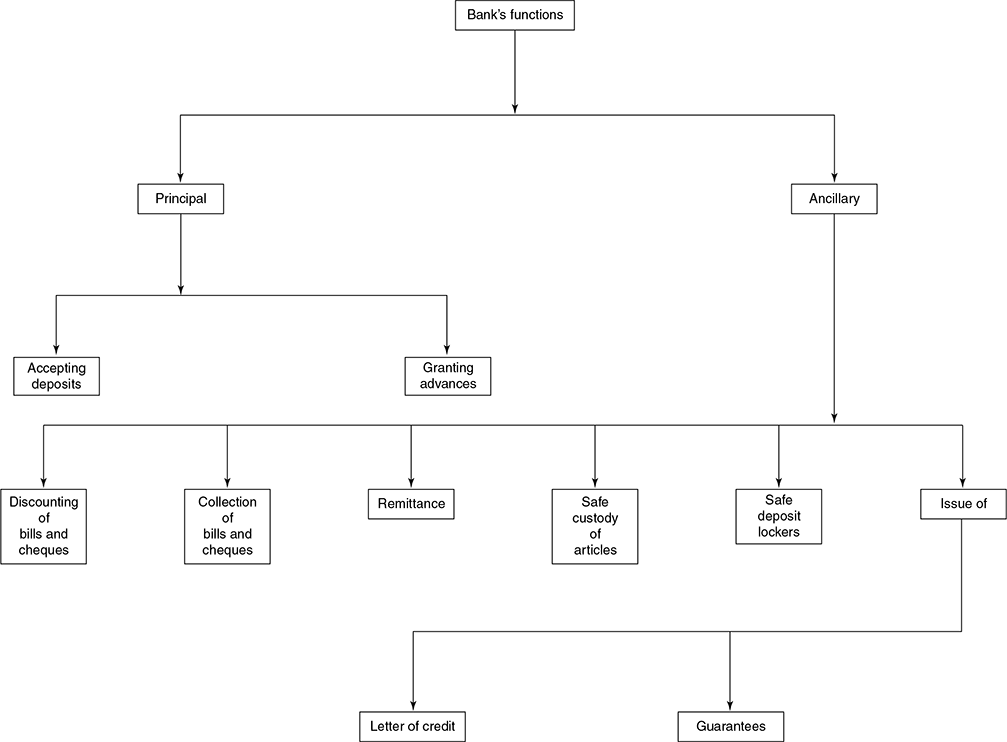

Retail banking encompasses retail deposit schemes, retail loans, credit cards, deposit cards, insurance products, mutual funds, depository services including demat facilities. It includes various products and services forming a part of the assets as well as the liabilities segment of the banks. A simplistic definition could be ‘banking catering to the multiple requirements of individuals relating to deposits, advances and associated services’. See Figures 13.1 and 13.2.

Why Banks Focus on Retail Business

Financial Disintermediation

Traditionally, banks have been catering to demands of economic developments; finance for manufacturing activities had a greater priority. Reliance of commercial banks was on blue-chip companies for deployment of funds.

A scenario has emerged wherein there is a lack of demand for credit from large corporates, primarily due to two reasons:

- Near demise of working capital requirements due to enhancement in activities like productivity and increased sales realization.

- Corporates have their own avenues, e.g., tapping public deposits and issuance of shares and debentures.

Advent of Economic Liberalization Privatization and globalization has opened the gate for a lot of new players in the banking sector, which has resulted in competition with each other for market share. The confluence of increased purchasing power, consumerism and competition with the banks has resulted in a retail chase. The identity of banks has changed from those known for their roles in development of business/economy to the ones helping in the development of the family.

Instant Solution for the Ills in the Banking Business Retail banking has the potential to provide decent ret urns for banks with an extended clientele base in an era of thinning margins and non-performing advances.

Retail banking is based on the principle ‘banking for the people, by the people and of the people’.

Emerging Issues in Handling Retail Banking

Knowing the Customer A concept which is easier said than practised. Each branch should set up data warehouse wherein meaningful data on customers, their preferences, spending patterns, etc. can be mined.

Technology Issues Retail banking calls for huge investments in technology, e.g., providing anytime, anywhere convenience to vast number of customers and delivery channels through asynchronous transfer modes (ATMs), which requires a huge investment by the banks.

Product Innovation All new products may not become successful. Products should be introduced to create value, not amusement. The days of selling products on the shelves are gone in the banking sector.

Pricing of Products The banking sector is witnessing a pricing war with each bank wanting to have a larger slice of the market share. The much needed transparency in pricing is also missing with many hidden charges. For example, ‘minimum amount due’ and ‘total amount due’ in the credit card application form and processing charges are not advertised.

Issues Related to Human Resources

- Motivating the front line staff by projecting them as sales managers of products rather than as clerks at work.

- Changing the image of the bank from a transaction provider to a solution provider.

Low-Cost and No-Cost Deposits Bank managers are in need of more savings bank and current accounts so that their cost of liability would be less.

- Three AAAs (anytime, anywhere and anyhow banking).

- With the advent of ATMs, ‘anytime banking’ has become a reality.

- Satellites and telecom networks across the world have made ‘anywhere banking’ possible.

- Now, it is the turn of ‘anyhow banking’.

SWOT Analysis of Retail Banking

The strengths, weaknesses, opportunities and threats of retail banking have been analyzed and given in Table 13.1.

Strategies for Success in Retail Banking

Banks can formulate the following strategies in order to achieve success in the retail banking segment:

- Advanced techno logy and adoption of this latest technology

- Skilled manpower in all branches and offices

- Balanced and sustained growth in deposits and advances

- Strategic cost management

- Market research and market intelligence, in order to formulate competitive and innovative products

- Risk management

- Customers relationship management

- Universal banking/financial supermarkets

- More delivery channels

- Service quality with a human touch

SECTION III

CUSTOmER RELATIONSHIP mANAGEmENT (CRm)

The objectives of this section are:

- To highlight the importance of Customer Relationship Management (CRM).

- To provide inputs on how to market bank products.

- To discuss the increased relevance of CRM in light of the growing competition in the banking sector with the entry of foreign and new generation banks.

Marketing—Coin

| Head | — CRM |

| Tail | — Advertisement |

Customer relationship management and advertising are an integral part of marketing. However, CRM and advertising are two different sides of the coin called marketing. Advertising is too expensive. On the other hand, CRM is based on word of mouth. Hence, meeting customer needs is most important in the competitive banking sector.

Although CRM is a recent concept, its tenets have been around for some time. CRM has three application areas:

- Customer acquisition

- Customer value maximization

- Customer retention

A banker must keep CRM in mind from the time he acquires a new customer and each time the customer is serviced. CRM is based on word of mouth, hence, a pleasant experience for the customer would ensure retention and possibly, new customers. Furthermore, how a bank handles complaints also goes a long way in building an image in the customer’s mind.

CRM Strategies/Steps

Some of the important CRM strategies/steps are as follows:

- Appeal to the self-interest of the customer, during discussions. Steer conversation to topics like areas of interest, profession, native place and hobbies. ‘Recognize’ the customer. All human beings need recognition. Most of us seek recognition in the company of others. Managers can give customers individual recognition with some small talk and friendliness. It is worth noting that the correlation between the enthusiasm of manager and customer satisfaction is always high. It would be useful for bankers to know the preferences of customers (time/service/money) and treat them accordingly.

- Make use of logic and emotional appeal to motivate the customer. Courtesy and concern are prime necessities for a bank. Offering a seat, bidding farewell, using the right blend of formality and informality, demonstrating civility to aged people are all important.

- Be patient (have self-control) with difficult customers. It will pay-off in the long run.

- Know the strength and weaknesses of competitors so that you will be prepared to face competition. The competition in the sector is escalating day by day. PSU banks, private banks, foreign banks have all formulated strategies for more customers.

- Smile while serving the customer. The smiling face of a banker brings reassurance to the customer who develops goodwill for the bank.

- Importance of ‘Greeting and Meeting.’ All banks offer identical products and polite service. Customers go back to the bank, where officers greet him/her with a smile. Marketing efforts and CRM have to be laced with humour and smile.

Three Tip Questions for Managers

Managers can do self-introspection by way of asking a set of questions as follows:

- Can I recall the names of customers and people?

- Do I mingle with the customers?

- Did I appear active and cheerful or do I present a gloomy appearance?

Image-Building Exercises

Officers and staff in a bank normally undertake the following exercises to build the image of their organization in their efforts to build brand.

- Marketing activities are closely tied to the cleanliness and aesthetic aspects of bank premises.

- Marketing activity would be incomplete without making ‘customer calls’ and gathering their perception about products offered by the bank.

- Cultivating relationship is the specialty of the modern day banker. From college days, banks give credit cards free of cost to students of reputed institutes.

- Some banks undertake payment of phone and electricity bills for clients.

- Bank of Tokyo Mitsubishi, one of the leading banks in Japan does not advertise, but relies on the word of mouth of its customers.

Blending Tradition with Technology

All banks focus on automating and improving business with customers in the areas of sales, marketing and support. Today, with the use of information and communication technology, banks can offer personalized service. Services like anywhere banking to their customers, mobile banking and loan melas for customers have been implemented by all banks.

Customers are becoming more dynamic in their behaviour. Banks use CRM tools to identify which customers are to be ‘targeted.’

CRM is based on the idea ‘banking for the customers, by the customers and with the customers’.

Historically, banking had a limited standard product range. Currently, it is moving with a larger range of products, aimed at specific customer base segments to a future where marketing will deal with customers as individuals, providing ‘tailor-made’ solutions to cater to their needs (e.g., monthly/quarterly installments, 1/2/3/4/5 year loans for car purchase).

Banks are moving from a product-focused, mass marketing approach to a customer-focused micro-marketing approach. CRM is based on database-driven marketing to communicate with a customer in response to his behaviour. Success depends on attitude and culture of employees to serve the customer better.

SECTION IV

LAwS IN EVERyDAy BANKING

Key Acts That Govern the Functioning of the Banking Sector2

The Reserve Bank of India Act, 1934

Establishment and preamble

The Reserve Bank was established on 1 April 1935 in accordance with the provisions of the Reserve Bank of India Act, 1934, with its central office at Mumbai since inception.

The preamble of the act prescribes the objective of the Reserve Bank as follows:

‘… to regulate the issue of bank notes and keeping of reserves with a view to securing monetary stability in India and generally to operate the currency and credit system of the country to its advantage’.

The Reserve Bank of India Act, 1934 has defined the main functions of the RBI as follows:

- Monetary authority

- Regulator and supervisor of the financial system

- Manager of exchange control

- Developmental role

- Related functions

The Negotiable Instrument Act, 1881

A few key points regarding the act are as follows:

- This act was passed to define the law relating to promissory notes, bills of exchange and cheques. The act was originally drafted in 1866 by the Law Commission of India. The bill was redrafted in 1877, because of the objections.

But the bill could not reach the final stage. In 1880, by the order of the secretary of state, the bill had to be referred to a new law commission. On the recommendation of the new law commission, the bill was redrafted.

- The draft thus prepared for the fourth time was introduced in the Council and was passed into law in 1881 as the Negotiable Instruments Act, 1881 (26 of 1881).

The Banking Regulation Act

The Banking Regulation Act was passed as the Banking Companies Act, 1949 and came into force with effect from 16 March 1949. Subsequently, it was changed to the Banking Regulation Act, 1949 with effect from 1 March 1966.

Some important sections of this act are given as follows:

- Banking means accepting for the purpose of lending or investment of deposits of money from the public repayable on demand or otherwise and withdrawal by cheque, draft order or otherwise [5(I) (b)].

- Banking company means any company which transacts the business of banking [5(I) (c)].

- Demand liabilities are the liabilities which must be met on demand and time liabilities means liabilities which are not demand liabilities [5 (I) (f)].

- A banking company may be engaged in businesses, like borrowing, lockers, letter of credit, travellers cheque and mortgages [6(1)].

- Cash reserve—Scheduled banks to maintain 3 per cent of the demand and time liabilities by way of cash reserves with themselves or by way of balance in a current account with the RBI (18).

- Every bank is to maintain a percentage of its demand and time liabilities by way of cash, gold, unencumbered securities 25–40 per cent as on the last Friday of second—the preceding fortnight (24)—known as the Statutory Liquidity Ratio (SLR).

- Every bank has to publish its balance sheet as on 31st March, (29).

- The balance sheet is to be audited by qualified auditors (30(I)).

- A published balance sheet and auditor’s report should be available to the public within 3 months from the end of the period to which they refer. The RBI may extend the period by a further 3 months (31).

Different Customers—Different Laws

There are different laws that apply to different groups which are classified as follows:

- Joint hindu family

- Societies

- Trust

- Company

- Sole proprietor/partners

Joint Hindu Family A Hindu undivided family (HUF) or joint family possesses ancestral properties and carries on an ancestral business. The ownership of such property passes on to the member of the family according to Hindu Law. In the case of a joint Hindu family governed by the Mitakshara school of Hindu Law, every male member of a family acquires an interest in the joint property by birth.

Societies Voluntary societies committed to promotion of art, science, literature or to charitable purpose may be incorporated under the following acts:

- The Societies Registration Act, 1860

- The Companies Act, 1956

- The Co-operative Societies Act

A society gets the legal recognition as an entity separate from its members only after its incorporation under one of these Acts.

A registered society is governed by the provision of the act under which it is registered. It may have its own constitution, character, memorandum of association, rules and by-laws to carry on its activities.

Trusts According to the Indian Trusts Act, 1882, a trust is an obligation annexed to the ownership of the property, arising out of a confidence reposed by the owner, or declared and accepted by the owner for the benefit of the author, or of the author and the owner.

- Author: The person who reposes the confidence.

- Trustee: The person on whom the confidence is reposed.

- Beneficiary: The person for whose benefit the trust is formed.

- Trust deed: The document by means of which the trust is formed.

Joint Stock Company A joint stock company is an artificial entity with perpetual section succession brought into existence under the provision of the Companies Act. Legally, a company is considered as an entity separate from its member and hence possesses all powers to enter into a valid contract.

A joint stock company has to submit the following important documents while giving an application to open a bank account.

- Certificate of incorporation and certificate of business

- Memorandum of association

- Articles of association

- Board resolution

Sole Proprietor and Partnership An individual running a business or commercial activity under a name other than his/her own is known as a sole proprietor.

Partnership is defined as relation between two or more persons who have agreed to share the profit of business run by all or any of them acting for all.

Bankers will have to take precautions while opening an account in the name of a partnership firm. These precautions can be specified as

- Partnership letter or mandate

It is a letter signed by all partners and contains the following details:

- Name of all partners

- Nature of business

- Limitation on the number of partners

- Minimum two

- Maximum for banking business—10; others—20

Bank–Customer Relationship

A customer’s deposit is a debt given to a bank for the bank’s use, repayable on demand. The bank becomes the customer’s debtor and the customer becomes the unsecured creditor with no claim over the bank’s assets as security.

When the customer takes a loan, he/she becomes the bank’s debtor. As the bank normally obtains security for the loan it gives, the bank becomes a secured creditor for the customer.

When the customer deposits securities or other valuables with the bank for safe custody, the bank becomes the trustee of these assets. The customer remains the owner.

When the bank buys or sells securities on behalf of the customer or pays the utility bills of the customer, it acts as the customer’s agent. Such services are rendered for the convenience of the customer.

So what is the relationship between the banker and customer when a cheque is sent for collection to another banker? The answer is Trustee.

Rights of a Banker

The important rights of a banker are as follows:

- Right of general lien

- Right of setoff

- Right of appropriation

- Right to change interest, levy charges, etc.

Let us now understand each of these rights.

Right of General Lien The right of a general lien is as follows:

- Lien is the right of a creditor to retain the goods and securities owned by his debtor until the debt is repaid.

- This right has some important features and conditions. When a lien applies to a specific debt, it is known as a particular lien. When a tailor retains the clothes stitched by him till his tailoring charges are paid, the tailor is exercising a particular lien. A general lien applies to all amounts due from the debtor.

Right of Setoff The right of a setoff is as follows:

- Under this right, the bank may use the credit balance in another account, when both accounts belong to the same customer. The accounts may be held in different branches.

- Normally, the bank takes a letter in advance from the customer authorizing the setoff without prior notice to the customer.

The main condition of right of setoff is ‘same name, same right’. Both the accounts must be held in the same name and in the same capacity. This is to avoid misuse of funds belonging to someone else but standing in the name of the customer.

Right to Appropriation: Who and How The right to appropriation is as follows:

At times, a customer takes several loans from the bank. When the banker receives the payment from the customer, against which loan should the deposit be appropriated? Who is the deciding authority on this? According to the Indian Contract Act, the right of appropriation vests with the debtor. Alternatively, the payment may be made under circumstances clearly implying the debt to be discharged. In the absence of such circumstances and instruction from the debtor, the bank, as the creditor can exercise the right.

Right to Charge Interest and Levy Charges As a creditor, the bank has the implied right to charge interest on loans given to customers. Periodically, the customer account is debited with the interest due. The banks may also levy charges to meet incidental expenses incurred on a current account.

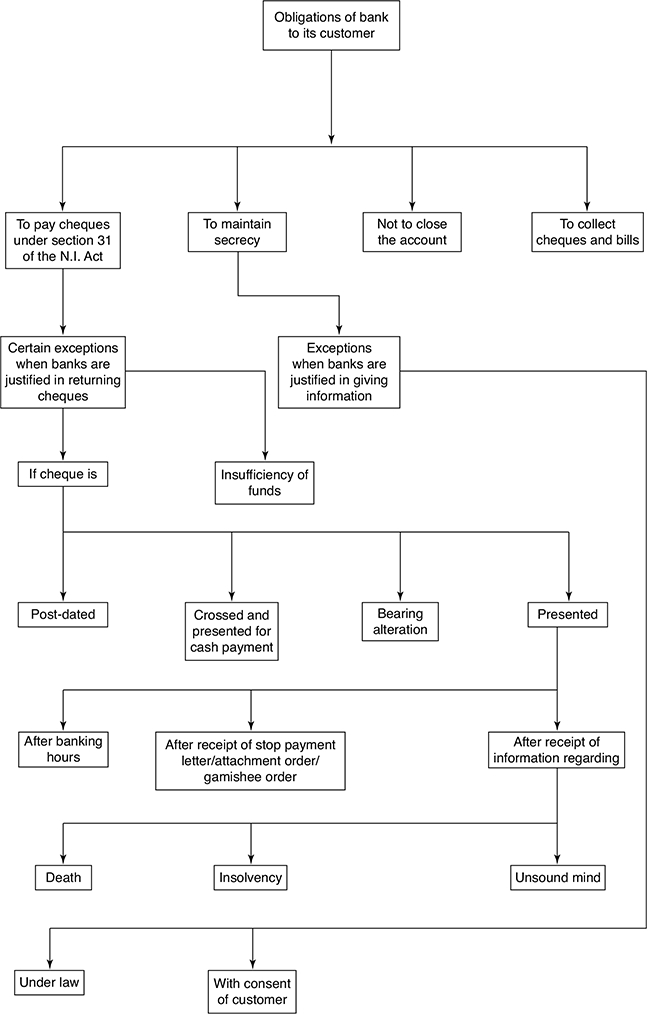

Obligations of a Banker

The banker is essentially a debtor or creditor to the customer. However, such a relationship imposes certain obligation on the bankers.

Honour Cheques The following points are related to honour cheques:

- There must be sufficient funds.

- They must be properly applicable to a cheque.

- They must be properly presented in proper time.

Wrong Dishonour of Cheque This may happen due to following causes:

- The mistake in posting that reduces the correct balance to the customer’s credit.

- Fraud committed by employee.

- Honouring a post-dated cheque.

The banker is responsible not only for the monitory loss but also for the injury to the customer’s reputation. The latter is more important to a customer.

Maintain Confidentiality A customer account reflects his/her true financial position. This information is very sensitive and may directly reflect on the customer’s reputation. Therefore, the banker should:

- not disclose any information regarding the account to a third party.

- ensure no such information leaks out of the account books.

- prevent such disclosure even after the account is closed.

The exceptions are as follows:

- When required by the law.

- Practice and usage among bankers.

Premature Closure A bank may allow premature encashment of a fixed deposit at the request of customer. In this case, the banker’s obligations are as follows:

- Ensure that the customer has the information about the bank’s penal interest rates for the premature withdrawal of term deposits, if the bank charges such an interest.

- Inform the customer while opening the account whether the bank disallows premature withdrawals of large deposit held by entities other than individuals and HUF.

Act in Good Faith Without Negligence The banker collects numerous cheques on behalf of the customers and cannot verify the validity of each instrument. The Negotiable Instrument Act protection to the banker can be specified as follows:

- The cheque must be crossed before it is deposited.

- The cheque must be received as an agent of the customer whose account is to be credited with the amount of the cheque.

- Payment is received in good faith and without negligence.

Examples of negligence of bankers are as follows:

- Opening an account without proper instruction.

- Overlooking irregularity of endorsement (e.g., spelling, signature).

- Collecting ‘account payee’ cheques for another person.

Deceased Depositors The key points to be considered regarding deceased depositors are as follows:

- If depositor dies, the banker is obliged to pay the amount to the credit of a deposit account to the nominee survivor or claimant.

- If death occurs before maturity of the deposit, the interest is payable at the rate applicable to the deposit up to the actual date of payment. If death occurs before maturity, the claimants may be paid at the saving rate of interest prevalent on maturity date for the period from maturity to the payment date.

- A succession certificate is not mandatory; however, the bank may obtain an indemnity bond. Where there is a dispute among legal heirs who are unable to provide a unanimous indemnity bond, the bank should obtain the succession certificates.

- If there are doubts about the claimants, the bank should insist on succession certificates.

Payment to Nominee The payment to the nominee is made in the following conditions:

- Nomination may be made in the name of individuals.

- In case of a joint account, there can only be one nominee and the nominee may receive the dues only after the death of all the depositors.

- Nomination may be altered at any time in the prescribed manner.

Closure of Accounts The banker must comply with a written directive from the customer to dose his/her account. The customer must be asked to return unused cheques.

Other possible occasions on which a bank can close the accounts are on receiving notice of a customer’s insanity or death or when the customer becomes insolvent.

BOX 13.1 DEMONETIZATION:

Demonetization is a procedure by which certain cash or currency notes are replaced with the other modes of financial transactions such as cheques, electronic payment etc.. Demonetization of currency notes (Rupees 500 and 1000) was implemented on November 8, 2016, in India. The government declared the withdrawal of 500 and 1000 rupee notes so as to battle the black money and fake currency. As expected, the sudden deficiency of currency prompted a void in the business. Serpentine lines in the ATMs and banks saw the normal open quickly trading the old notes with the new ones and keeping the old notes in the banks. This move centered to a greater amount of computerized, online exchanges consequently upgrading the installments of machines such as Automatic tellers to replace the cash. Another 2000 rupee note was brought into the monetary system as high-esteem cash. New notes of 500 and 1000 rupees were likewise discharged in the market in the consequent days.

The total currency available for use in India was Rs. 17.77 lakh crore (US$260 billion). The Indian government reported a prompt prohibition on two noteworthy bills that record for most by far of all currency available for use. Indians were given approximately two months time to replace/ change those notes for different bills, including recently printed ones. The demonetization has resulted in paving the way of new trend in the transaction, i.e. online shopping and digital payments and implications on the rural consumer4.

The reasons behind demonetization, according to the Government were to control black money and to give a boost to digitalization of banking and financial services. Impact of Demonetization can be seen in terms of digital wallets and its suppliers, customers, and the market prepared for mass selection of advanced wallets. Many experts have argued for Digital wallet industry5 as an alternative to the demonetization. The demonetization has been instrumental in increasing the transaction volumes of online bank transactions, e-clearing, e-KYC etc. The demonetization is to fight against illegal monetary streams in India6. In India demonetization was a praiseworthy endeavor to battle the country’s different monetary issues, but that it is probably going to shake the economy7.

Demonetization history in India

- This is not the first time when Indian currency was demonetized in India.

The first case was in 1946 and the second in 1978 when a statute was proclaimed to eliminate notes with the division of ₹ 1,000, ₹ 5,000 and ₹ 10,000. The most valuable currency at any point printed by the Reserve Bank of India was the ₹ 10,000 note in 1938 and again in 1954. Be that as it may, these notes were demonetized in January 1946 and again in January 1978, as per RBI information. ₹ 1,000 and ₹ 10,000 banknotes were available for use preceding January 1946. Higher category banknotes of ₹ 1,000, ₹ 5,000 and ₹ 10,000 were reintroduced in 1954 and every one of them were demonetized in January 1978. The ₹ 1,000 note made a rebound in November 2000. ₹ 500 note came into course in October 1987. The move was then supported as an endeavor to contain the volume of banknotes available for use because of expansion. However, this is the first occasion that ₹ 2,000 currency note is being presented (In the year 2016 ).

Reasons for Demonetization

There can be many reasons for Demonetization in any economy. Some of them are:

- Introduction of New Currency,

- To discourage black currency in the economy (The move is evaluated to scoop out more than more than Rs 5 lakh crore Black currency from the economy).

- To bring down the trade flow out the nation this is specifically identified with corruption

Demonetization Advantage and disadvantage

Demonetization alludes to stopping of current currency units and replaces those currency units with new currency units. It is a noteworthy decision and it impacts every resident in light of the fact that overnight all the money you have turned into a bit of paper which has no esteem in the event that you don’t exchange it with new currency units or deposit it in the banks. So as to comprehend demonetization better we should take a look at its advantages and disadvantages.

Advantage of Demonetization

The greatest advantage of demonetization is that it helps the government to track individuals who are having substantial totals of unaccounted currency on which no income tax has been paid on the grounds that many individuals who acquire black money keep that cash as trade out their homes or in some mystery pot which is outstandingly difficult to find and when demonetization happens all that cash is of no regard and such people have two option one is to deposit the currency in bank A/c and pay tax on such aggregate amount and the second option is to let the estimation of that cash value reduce to zero.

Since black money is utilized for illicit activity like terrorism activity’s funding, betting, tax evasion and furthermore blowing up the rate of assets classes like land, house, property, gold and because of demonetization all such activity will get decreased for quite a while and furthermore it will take years for individuals to create that measure of black money again and thus in a way it helps in putting an end to this hover of individuals doing unlawful activity to acquire black money and utilizing that black money to accomplish more unlawful activity. Another advantage is that because of individuals uncovering their wage by keeping cash in their financial balances government gets a decent measure of duty income which can be utilized by the legislature towards the advancement of society by giving great framework, clinics, instructive foundations, streets and numerous offices for poor and destitute segments of society

Disadvantage of demonetization

The disadvantage of demonetization is that once individuals become acquainted with it than at first for few days there is turmoil and craze among them as everyone needs to dispose of demonetized notes Destruction of old currency units and printing of new currency units include costs which must be borne by the legislature and if the expenses are higher than advantages then there is no utilization of demonetization. Majority of times this move is focused towards black money yet in the event that individuals have not kept money as their black money and turned or utilized that cash in other resource classes like land, gold et cetera then there is no certification that demonetization will help in getting degenerate individuals.8

Class room Exercise: Watch the video on demonetization on the author page facebook.com/drjustinpaul and discuss the insights.

References

Dr. Partap Singh, V.S., 2012. Impact of Globalization on Indian Economy. Golden Research Thought, 1(8), pp.290–300.

Gajjar, N., 2016. Black Money in India : Present Status and Future Challenges and Demonetization. International Journal of Advance Research in Computer Science and Management Studies, 4(12), pp.47–54.

Gupta, D.K. & Ph.D, Haryana School of Business, GJU S & T, H., 2016. DEMONETIZATION IN INDIA 2016--MOTHER TONGUE FRIENDLY E- DELIVERY BANKING CHANNELS FOR CASHLESS GROWTH, (Posted: 11 Jan 2017), p.8 Pages. Available at: https://papers.ssrn.com/sol3/Papers.cfm?abstract_id=2894129.

KAUSHIK BASUNOV. 27, 2016, 2016. In India, Black Money Makes for Bad Policy., p.2017.

Krishnan, D. & Siegel, S., 2017. Effects of Demonetization: Evidence from 28 Slum Neighborhoods in Mumbai.

Kumar, P., 2017. Demonetization and Its Impact on Employment in India. Available at: http://arxiv.org/abs/1702.01686.

Kumar, S.V. & Kumar, T.S., 2016. DEMONETIZATION AND COMPLETE FINANCIAL INCLUSION. International Journal of Management Research & Review, 6(12), pp.52–57.

Newsletter, T.M. & November, S., 2016. On Demonetization., 6(11).

P.RamaKrishnamRaju & Raju, P.V.R., 2016. DEMONETIZATION IN INDIA. Volume 3, Issue-12(4), December, 2016 International Journal of Academic Research, Publications, Sucharitha, 3(12), p.166.

Vinish Parikh, 2017. Demonetization Advantages and Disadvantages., pp.1–5.

CHAPTER SUMMARY

Commercial banks have been relying on corporates for a long time as their main source of income because the latter have not had access to any other avenues like capital markets. In the last few decades, the focus of commercial banks has changed from corporate banking to retail banking. The retail banking segment offers an extended client base which, in turn, minimizes the risk for banks. It is evident that the banks that formulate strategies and implement practices like Customer Relationship Management emerge as winners in this era of competition and globalization.

CASE STUDY

SAVINGS ACCOUNT IS NOT AN INVESTmENT TOOL3

The Mumbai suburban Borivali-bound fast local train was overcrowded and Ravi Kumar had boarded the train from the starting point CST station after his work. He had to get down at Andheri which is located before the last station. He thought it would be better to stand at the door. However, when the train halted, Kumar as usual, got pushed out. As a matter of habit, he checked if his wallet was in place. To his horror, he realized it was not. His wallet was already stolen by someone. Though Kumar was carrying a little cash, he had a debit card, linked to his savings account, which had ₹65,000. Now, he had to act fast and get his debit card blocked. This was tough as the bank would have closed down for the day by now.

With the extra cash he always kept aside for days like this, he managed to reach home. He frantically searched for the ‘welcome kit’ he had received from the bank on opening the account. The kit contained a detailed booklet on debit card usage. He had to call up the 24-hour customer service number of the bank and report the loss. From that moment on, he would be insured against fraudulent purchase transactions. But his insurance would not be available for ATM transactions as he was the only one who had the password and there was no way anyone could withdraw money from his account using the ATM. Having done this, Kumar had a bigger question to answer—Why did he has so much money in his savings account that gave him a miniscule interest of 3.5 per cent? He knew he had been extremely lazy about putting his money to better use, despite the fact that the requirement of a minimum average quarterly balance of ₹5,000 in the account was driving him paranoid.

His laziness had been costing him dearly. The interest rate of 3.5 per cent was on the minimum balance in the account between the tenth and the last day of the month. Also, banks could pay this interest either monthly or quarterly, and his bank chose to pay quarterly.

Even the interest on a 15-day fixed deposit was somewhere around 5.5 per cent. All one needed to do was log on to the net and do a fixed deposit. And the certificate would be delivered at the specified address with in a few days.

Further, with all the money in the savings account, there was always the danger of carrying too much money in the wallet.

When Kumar opened this savings account, he had been told about the requirement of maintaining a minimum quarterly average balance of ₹5,000. In the good old days, all one needed to do was have a balance of ₹500 and if one went under the limit, most public sector banks simply slapped a fine of ₹10. Things had become far more complicated since then.

In order to calculate the average quarterly balance, his bank considered the period between the 25th day of the last month of the previous quarter to the 24th day of the last month of the present quarter. In other words, Kumar was expected to maintain an average balance of ₹5,000 in his savings account on each day of this 90-day period. Alternatively, he could have ₹4,50,000 in the account for a single day to meet the average quarterly balance requirement of ₹5,000 (₹4,50,000/90 = ₹5,000).

In case he did not maintain the minimum average quarterly balance, the bank would charge for non-maintenance. The charge in his case was ₹250 if the average quarterly balance was between ₹2,500 and ₹5,000 and ₹500 if it was below ₹2,500.

Kumar felt the charges were too high, but he had the satisfaction of knowing that there were other banks which charged as high as ₹750 for non-maintenance. Indeed, wasn’t it for charges like these that the fee-based incomes of new generation private sector banks had gone up dramatically in the last few years?

Case Questions

- Why does a savings account offer low interest rates?

- Distinguish between minimum balance, average quarterly balance and average monthly balance.

- Discuss the methods of calculating average quarterly balance.

TEST YOUR UNDERSTANDING

- Banker’s lien is a (n) ____________.

- hypothecation

- mortgage

- implied pledge

- pledge

- Mandate is (a) n ___________.

- stamped agreement

- order of the court of law

- memorandum of understanding

- unstamped letter to the bank

- Power of Attorney is a ________.

- signed letter to the bank

- promissory note

- garnishee order

- stamped documents

- Person to whom a power of attorney is given is called _______ and the person who gives the power of attorney is called _________.

- Debtor-Creditor

- Bailor-Bailee

- Agent, Principal (donor, donee)

- Negotiate instrument (N I) are easily ________.

- transferable

- gifted

- sold

- A cheque is drawn on a (n) _____.

- owner of a ship

- agent of a principal

- bank

- Two parallel transverse lines across the cheque is called ____.

- endorsement

- transfer

- assignment

- crossing

- When a cheque is drawn on a bank, the bank is called the _______.

- drawer

- endorser

- acceptor

- drawee

- The crossing in a crossed cheque can be cancelled by ______.

- drawer

- endorser

- acceptor

- drawee

- When a banker makes payment of a cheque after banking hours, he will be held _____.

- liable

- reasonable

- acceptable

- One of the conditions to honour a cheque by the paying banker is that amount in words and figures should __________.

- differ

- tally

- be clear

- Where a customer, by a letter, has advised the bank directing the banker not to honour or pay a particular cheque, such a letter is called a _______.

- Where the signature of the drawer of a cheque is not genuine, such a cheque is called a _______.

- post-dated cheque

- forged cheque

- clearing cheque

- stale cheque

- Demand deposits are those which can be withdrawn ______.

- on demand

- at any future date

- after 1 year

- after 5 years

- Current deposits are not entitled to _____.

- a cheque book

- statements

- customer service

- interest

- Introduction in all deposit accounts is ______.

- optional

- compulsory

- at the discretion of the bank

- A bank has the obligation to maintain confidentiality of customers’ accounts. The only exceptions are

- no exceptions as bank is liable for financial loss

- with the concurrence of the Reserve Bank of India

- when the different laws warrant so

- the banker has to use its discretion and selectively reveal the balance

- both ‘a’ and ‘b’

- Which of the following is NOT a feature of a recurring deposit product?

- Amount periodicity and tenure of investment fixed

- Identical to fixed deposit in terms of interest rates

- TDS as per the applicable rates

- Loan against deposits available

- All of these

- Which of the following is NOT one of the functions of the RBI?

- monetary authority

- manager of exchange control

- corporate finance

- supervisor of financial system

- developmental role

- A ‘society’ cannot be incorporated under one of the following acts:

- The Societies Registration Act, 1860

- The Companies Act, 1956

- The Co-operative Societies Act

- The Partnership Act, 1932

- NRNR and FCNR (B) accounts can be kept in the form of ______.

- term deposits

- current deposits

- saving deposits

- recurring deposits

- Accounts jointly with residents can be opened in the case of _______ accounts.

- FCNR (B) and NRE

- NRO and NRNR

True or False

- Payment of a post-dated cheque by a banker is in order.

- Right of setoff is not a discretionary right with the bank.

- A forged cheque is a valid cheque.

- In savings deposits, interest is paid on the minimum balance in the account between the 10th and the last working day of the month.

- A FCNR (B) account can be kept in the current, savings and recurring deposits.

- Credit card offers revolving credit for a certain period.

TOPICS FOR FURTHER DISCUSSION

- A holds ₹820 to his credit in a bank. He presents five cheques of ₹200 each for payment at the same time. Can the banker refuse payment of all the cheques?

- A payee of a cheque informs the bank, on which it is drawn, that the cheque drawn in his favour is lost and requests the bank to stop payment of the cheque pending an advice from the drawer. But before the stop-payment instructions are received from the drawer, the cheque is presented through clearing. How should the drawee bank act?

- A teacher deposits into his account an outstation cheque for ₹800 issued by the state education authorities. He demands immediate credit in his account against the cheque. Explain your reply.

- Mr. A opens a well-introduced savings account with you. He deposits a cheque crossed ‘account payee’ in the account and withdraws the amount. A few days later, the paying banker informs you that the drawer of the cheque has learnt that the real Mr. A has not received the cheque and it was stolen in transit. On further inquiry, it appears that the man who opened the account with you is not traceable at the address given. The paying banker calls upon you to pay back the amount as the cheque was wrongly collected by you. As the branch manager how would you deal with the above situation?

- Distinguish between

- Cheque and bill of exchange

- Mandate and power of attorney

- NRE, FCNR (B) and NRO accounts

- Savings bank account and current account

- Analyze the strengths, weaknesses, opportunities and threats of retail banking.

SELECT REFERENCES

- Aleida, R. A. (2003). ‘Retail banking—A Focus’, IBA Bulletin, November, pp. 5–8.

- Manoj, P. K. (2003). ‘Retail Banking—Strategies for Success’, IBA Bulletin, November, pp. 18–21.

- Pathrose, P.P. (2003). ‘Marketing Retail Products: Strategic Perspectives for Banks’, IBA Bulletin, November, pp. 29–34.

- Sood, Rajesh Kumar (2003). ‘Retail Banking—Growth Drivers and Analysis of Associated Risks’, IBA Bulletin, November, pp. 9–17.

- Indian Institute of Banking and Finance (2005). Legal Aspects of Banking Operations, MacMillan. India.

ENDNOTES

- More details on bank deposits can be found in the chapter on ‘Sources of bank funds’.

- An illustrative list of legal provisions can be found in the chapter on ‘Sources of bank funds’.

- This is a substantially modified version of the write-up published by Vivek Kaul, ‘Personal Finance’, DNA Money.

- Kumudha, A. & Lakshmi, K.S., 2016. Digital Marketing : Will the Trend Increase in the Post Demonetization Period., 4(10), pp.94–97.

- Smita, M. & Pachare, M., 2016. Demonetization : Unpacking the Digital Wallets., 1(4), pp.180–183.

- Mehta, S., 2016. Demonetisation : Shifting Gears From Physical Cash To Digital Cash., 5(3), pp.47–52.

- KAUSHIK BASU NOV. 27, 2016, 2017. In India, black money makes for bad policy., 1(607), p.14853.

- http://www.letslearnfinance.com/demonetization-advantages-and-disadvantages.html (Vinish Parikh 2017)