CHAPTER TWELVE

Managing Interest Rate and Liquidity Risks

CHAPTER STRUCTURE

Section I The Changing Face of Banking Risks

Section II Asset Liability Management

Section III Interest Rate Risk Management

Section IV Managing Interest Rate Risk with Interest Rate Derivatives

Section V Liquidity Risk Management and Basel III

Section VI Applicability to Banks in India

Annexures I, II, III, IV, V, VI (Case study)

KEY TAKEAWAYS FROM THE CHAPTER

- Understand why risk management is important for banks.

- Understand sources of asset liability risk, interest rate risk and liquidity risk.

- Learn how interest rate risk is managed.

- Learn how interest rate derivatives work.

- Learn how liquidity can be managed.

- Understand the International and Indian standards for measuring and managing interest rate and liquidity risks in banks.

“The business of banking is the business of risk management; plain and simple, that is business of banking.”

—Walter Wriston, Ex CEO, Citibank

SECTION I

THE CHANGING FACE OF BANKING RISKS

Consider a bank that borrows ₹100 crores at 5 per cent for a year, and lends the money at 5.5 per cent to a highly rated borrower for 5 years. For simplicity, let us assume interest rates are to remain fixed over the period of the loan; they are annually compounded and all interest accumulates to the maturity of the respective obligations. The net transaction appears profitable since the bank is earning a 50 basis point spread.

But the transaction is not without risks.

- At the end of a year, the bank will have to repay ₹100 crores to the depositor(s), and find new sources of financing for the loan, which still has 4 years to maturity. If the bank is not able to find sources for repayment, it runs a ‘liquidity’ risk, which could threaten the ‘solvency’ of the bank.

- At the end of the year, if interest rates have risen, the bank would have to pay a higher rate of interest on the new financing, thus narrowing the spread. Suppose, at the end of a year, an applicable 4-year interest rate is 6 per cent. The bank is in trouble. It is going to earn 5.5 per cent on its loan and pay 6 per cent on its financing. In short, the bank will be losing money on this transaction! Thus, the transaction has also entailed an ‘interest rate’ risk for the bank, which would impact the bank’s net income

Also consider the following scenarios:

- Ninety per cent of Bank A’s liabilities mature within the next 12 months. Bank A has invested 80 per cent of these funds in securities maturing after 5 years.

- Ninety per cent of Bank B’s liabilities mature within the next 12 months. Bank B lends 75 per cent of these funds to various infrastructure projects, where the repayments will start after an initial payment holiday of 2 years.

- Eighty per cent of Bank C’s liabilities mature after 3 years and have been borrowed at fixed cost. Interest rates are on a downward trend, and 80 per cent of Bank C’s loan portfolio consists of short-term loans to be fully repaid over the next 6 months.

- Bank D has entered into dollar forward contracts at a premium for 6 months on behalf of its importer borrowers, who form about 60 per cent of the bank’s loan portfolio. There is a fall in dollar value during this period.

What are the potential dangers in each of the above scenarios?

In the first two scenarios, the banks face a liquidity risk. When the liability holders demand their money in the next 12 months, the banks may not have enough cash to repay them, since the cash flow from the assets would be delayed beyond this period. In the third scenario, Bank C faces an interest rate risk. The short-term loans would be repaid, and the cash inflow will have to be lent by the bank at the prevailing lower rates, while the bank will have to continue paying interest on liabilities at the original contract rates till they mature. The bank’s spreads would narrow further and impact the net earnings. Bank D, evidently, faces an exchange rate risk.

The primary problem in these examples was a ‘mismatch’ between the bank’s assets and liabilities. Prior to the 1970s, many firms in developed countries intentionally mismatched their balance sheets, and borrowed short and lent long to earn a spread, taking advantage of the upward sloping yield curves. Interest rates in developed countries experienced only modest fluctuations, so losses, if any, due to asset-liability mismatches were trivial.

Things started to change in the 1970s, which ushered in a period of volatile interest rates that continued into the early 1980s. The 1980s and 1990s also saw a new wave of banking crises in the developed world and emerging markets. These events challenged the traditional view that ‘runs’ on solvent banks were at the heart of banking panics and that panics were the main causes for banking crises. The striking fact here was that ‘bank runs’ had played a negligible role in most of these events.

With new financial instruments such as derivatives, new participants such as hedge funds and new technologies such as e-banking, the informational efficiency of markets to match savings with investment opportunities improved substantially in the early years of the 21st century.

The growth in derivatives markets has no doubt increased the tools available to firms to take on and manage risks, but has also made risk exposure assessment tougher for regulators, as the financial crisis of 2007 has amply demonstrated. For example, a bank can take large risks through trading of derivatives, without making the exposure visible on its balance sheet. Traditionally, banks exposed themselves to interest rate risks by taking deposits, making loans or buying securities. With derivatives, banks can use swaps to take on the same interest rate risk as, say, in the case of buying bonds. However, the swaps are not recorded on the banks’ balance sheets because the value of swaps at inception is typically zero. After inception of the swap, mark-to-market accounting requires the banks to record the market value of the swap, but that market value provides little indication of the magnitude of banks’ interest rate exposure.

Moreover, banks could improve their traditional ‘return on equity’ measure through taking on risks for feebased activities, without capital outlay.

Such developments have forced bank regulators and market participants to look for risk management approaches that would go beyond mere accounting numbers to capture realistic assessments of adverse outcomes, and reveal the actual risks borne by financial institutions. Figure 12.1 illustrates the sources of banking risks.

From Figure 12.1 and our discussions in earlier chapters, it is evident that banks are subject to various interdependent risks. Though, for convenience of measurement and analysis we isolate them, in reality, what starts off, say as a credit risk event, can snowball into a bundle of other risks as well. For the same reason, it appears difficult to conclude about the overwhelming cause of the financial crisis of 2007—was it subprime lending practices, or financial instruments, such as the Credit Default Swap or CDOs, or was it transactions such as securitization, or was it excesses in human greed and negligence?

However, one inference is clear—all banks and financial institutions will have to undertake a profound revision of their approach to risk management.

A relook at risk management does not imply that banks scale down their risk appetite, which is essential for future progress and survival in a competitive and developing environment. The implication only highlights the need for banks to state their risk policies more clearly and stringently, and ensure strict adherence to the policies and safeguards.

To complement the published work of a number of eminent bodies on the financial crisis of 2007, a unique private sector initiative termed the Counter party Risk Management Policy Group III (CRMPG III) was formed in April 2008, chaired by top bankers from HSBC and Goldman Sachs.1 The Policy Group members are drawn from various leading multinational banks. The scope of this initiative was designed to focus primarily on the steps that the private sector should take to avoid future financial shocks.

The Policy Group identifies some common features characterizing the post 1980 financial crises—(a) credit concentrations, (b) broad-based maturity mismatches, (c) excessive leverage, and (d) the illusion of market liquidity. It also includes a ‘wild card’ in the form of macroeconomic imbalances. Overarching all these factors is collective human behaviour, where financial institutions tend to take on disproportionate risks on the upside of business or financial market cycles, and pull back fiercely when the cycle is on the downturn. In this context, the Group recognizes the need for private initiative to ably complement supervisory oversight to mitigate banking risks.

The Group has developed ‘core precepts’ to provide the broad framework for risk management in banks that focus on the basics of (a) corporate governance, (b) risk monitoring, (c) estimating risk appetite, (d) contagion effects, and (e) enhanced oversight. The salient features of the recommendations in respect of these precepts call for the highest quality of risk management and governance within the bank, and supervision by external administrators.

We have discussed credit, market and operational risks in earlier chapters. In the following sections of this chapter, we will discuss the ‘wild card’ risk that broadly translates into interest rate risk, and most important, liquidity risk, a product of the various factors listed above.

SECTION II

ASSET LIABILITY MANAGEMENT

Risk management is uniquely important for financial institutions because, in contrast to firms in other industries, their liabilities are a source of wealth creation for their shareholders.2

Over the years, banks have been focusing on ‘asset-liability risk’ to mitigate balance sheet weaknesses. The problem is not that the market value of assets might fall or that the value of liabilities might rise. It is that capital might be depleted by narrowing of the difference between assets and liabilities, since the values of assets and liabilities may not always move together, in the same direction. Asset-liability risk, therefore, is a ‘leveraged’ risk. As we have already seen, the capital of banks is small relative to the firm’s assets or liabilities, so small percentage changes in assets or liabilities can translate into large percentage changes in capital.

The Asset-liability risk described above could manifest itself in more than one form, but what would concern bankers most would be two important risks—‘interest rate’ risk and ‘liquidity’ risk. While interest rate risk would directly impact the net income of the bank, the liquidity risk would endanger the very solvency of the bank.

The above need for risk management led to the evolution of Asset-liability management (ALM) in the 1980s. In a way, ALM was seen to substitute for market-value accounting3 in a context of accrual (book value) accounting. Traditionally, banks and insurance companies have been using accrual accounting for essentially all their assets and liabilities. They would take on liabilities, such as deposits, life insurance policies or annuities. They would invest the proceeds from these liabilities in assets such as loans, bonds or real estate. All assets and liabilities were held at book values. Doing so did not recognize the possible risks arising from how the assets and liabilities were structured, or how the markets were moving. To overcome these shortcomings, a combination of ALM and market value accounting was advocated.

However, many of the assets and liabilities of financial institutions cannot be marked to market. A firm can earn significant mark-to-market profits but go bankrupt due to inadequate cash flow. Market-value accounting was therefore not the ideal solution.

However, where found suitable, banks are increasingly using market-value accounting for certain business lines. This is true of universal banks with trading operations, which find techniques of market risk management such as Value at Risk (VaR),4 market risk limits, etc. more appropriate. On the other hand, ALM is associated with those assets and liabilities—those business lines—that are accounted for on an accrual basis. This includes bank lending and deposit taking.

In short, ALM is concerned with strategic balance sheet management. Risks caused by changes in interest rates and exchange rates, credit risk and the bank’s liquidity position have to be monitored and mitigated. With profitability of banking operations and the long-term solvency of banks becoming key factors, it has now become imperative for banks to move away from partial asset management (credit, non-performing assets) and partial liability management (deposits) to integrated balance sheet management. In such an approach, all components of a bank’s balance sheet, their maturity mix, their pricing and risks will be looked at not only from the angle of profitability, but also from the angle of solvency and long-term sustenance.

Techniques of ALM have been evolving over time. Banks typically have an Asset Liability Management Committee (ALCO) that comprises of a group of top or senior management personnel entrusted with the responsibility of managing the bank’s assets and liabilities to balance the various risk exposures, to enable the bank achieve its operating objectives.

Table 12.1 depicts the shift from traditional ALM objectives and practices to modern ALM techniques.

TABLE 12.15 TRADITIONAL ALM OBJECTIVES AND PRACTICES TO MODERN ALM TECHNIQUES

At present, in almost all banks, ALCO has the responsibility to devise broad strategies for handling banks’ competing long-term needs, and also monitor and manage interrelated risk exposures on a daily basis. Therefore, the ALCO of a bank is the focal point for coordinating the bank’s diverse activities to accomplish its operating objectives. Towards this objective, the ALCO receives and analyzes a wide variety of reports that bring together information on the bank’s asset/liability positions, its capital level, its internal plans and current and projected external conditions. Some typical types of information and analyzes the ALCO might receive include (a) information on current and projected national and local economic conditions, (b) interest rate forecasts, (c) current loan and deposit positions, showing the asset and liability mix, highlighting concentrated exposures, (d) forecasts of cash inflows and outflows on account of assets and liabilities, based on commitments and likely trends, (e) the current and projected liquidity position for the bank, and (f) an analysis of the potential effects of interest rate risk on the bank’s income and capital position.

Most ALCOs primarily focus on managing the bank’s liquidity and interest rate risks, while a separate committee would be involved in managing credit risks. In practice, evaluating interest rate and liquidity risks involve the consideration of different possible scenarios. For example:

- What if the bank experiences an unexpectedly large volume of deposit withdrawals?

- What if loan repayments occur earlier than anticipated? Or later than due date? Or not at all?

- What happens if interest rates suddenly rise by x basis points?

- What happens if counterparties do not keep up commitments? Or off-balance sheet items turn into real cash outflows?

The ALCO’s challenge is to assess the probability with which similar events would occur, and position the bank to handle the most likely scenarios with the minimum impact on the bank’s expected performance and solvency.

The ALCO will therefore operate with the objectives of (a) assessing the probability of various liquidity shocks, (b) assessing the probability of various interest rate scenarios and their impact on the bank’s net income, (c) positioning the bank to handle the most likely of these scenarios at minimum cost (impact on net income and the bank’s capital), while achieving a reasonable profitability level, and (d) allocating the bank’s remaining assets and liabilities to meet risk and profitability objectives.

ALM departments also handle foreign exchange and other risks. The growth of derivatives markets helped in ALM by facilitating a variety of hedging strategies, while securitization allowed banks to directly address assetliability risk by removing assets from their balance sheets.

Of the important risks that ALM addresses, interest rate risk and liquidity risk are accorded paramount importance. We shall study these in detail in the following sections.

SECTION III

INTEREST RATE RISK MANAGEMENT

Simply stated, interest rate risk is the exposure of a bank’s financial condition to adverse movements in interest rates. If accepted and managed as a normal part of banking business, interest rate risk can be used to enhance profitability and shareholder value. However, excessive interest rate risk could lead to substantial volatility in earnings and thus also affect the underlying value of the bank’s assets, liabilities and off-balance sheet instruments. Hence, an effective risk management process that aims at sound financial health of a bank would have to maintain interest rate risk within prudent levels. The two most common perspectives for assessing a bank’s interest rate risk exposure are (a) the earnings perspective that focuses on short-term earnings, and (b) the economic value perspective that looks at the long-term economic viability of the bank

Why are two approaches necessary? The ‘earnings perspective’ assesses the impact of changes in interest rates on the ‘net interest income’ (NII) (difference between total interest earned from loans and investments and total interest paid on deposits and borrowings) of the bank. This is the traditional method of risk assessment since reduced net interest earnings could threaten the financial stability of the bank and also impair market confidence. However, banks have been able to generate non-interest income from fee-based activities, such as loan servicing, transaction processing, off-balance sheet transactions or managing securitization pools, most of which depend on the way credit markets perform. Hence, a major portion of the fee-based income could also be interest rate sensitive, and banks would have to look at the impact of interest rate variations on net income as well.

‘Value’ or ‘economic value’ generally represents the present value of expected future net cash flows, discounted at appropriate market rates. For a bank, expected net cash flows would arise as the difference between expected cash flows on assets and the expected cash flows on liabilities, plus the expected net cash flows arising from off-balance sheet activities. We have seen earlier how variations in market interest rates can impact the economic value of banking assets, liabilities and off-balance sheet positions (contingent liabilities). Thus, the sensitivity of a bank’s economic value to fluctuations in interest rates is of great importance to all stakeholders—investors, management and supervisors—since it reflects the sensitivity of the bank’s ‘net worth’ to changes in interest rates. It is evident that the economic value perspective is more comprehensive and long term than the earnings perspective, since it considers the potential impact of interest rate fluctuations on future cash flows. This long-term perspective is valuable since short-term changes in earnings of a bank, which is the focus of the earnings perspective, cannot indicate realistically the impact of interest rate movements on the bank’s overall positions, and hence, its financial health in the long run.

But it is not always future interest rates that impact a bank’s financial performance. Past interest rates also have a continuing impact on future performance. For example, a long term, fixed-rate loan contract (as in the example quoted at the beginning of this chapter) may have to be refinanced at higher interest rates over the tenor of the loan. Securities not marked to market may contain embedded gains or losses due to past rate movements, which would be reflected over time in the bank’s earnings. Hence, the impact of such ‘embedded’ losses or gains due to past interest rates would also have to be assessed realistically.

Assessment of the extent of a bank’s interest rate risk by any of the perspectives given above would not be a simple exercise. Every asset on the bank’s balance sheet has different risk and return characteristics, different possible sources, repricing6 periods and so on. Box 12.1 presents some of the common sources of interest rate risk. The exercise would be rendered more complex by the discretion that the bank can exercise in adjusting the rates on assets and liabilities, or the likelihood of a change in bank customer behaviour (early repayment of loans or withdrawal of deposits) due to changes in market rates, or the interest rate sensitivity of fee-based income (non-interest income) and off-balance sheet exposures. In practice, banks will generally have a mix of all types of interest rate risk, with the effects potentially offsetting or reinforcing one another. It is the complexity of the resulting combination of factors that makes interest rate risk difficult to manage.

BOX 12.1 SOURCES OF INTEREST RATE RISK

As financial intermediaries, banks encounter interest rate risks arising from several factors fundamental to the business of banking. Some of the most discussed sources of interest rate risk are given as follows:

- Repricing risk: The primary and frequently discussed form of interest rate risk arises when the average yield on a bank’s assets or the average cost of its liabilities is more sensitive to changes in market interest rates. The difference in sensitivity could arise from possible mismatches in the asset and liability characteristics of the bank. First, fixed rate assets and liabilities could have different maturities. Second, floating rate assets and liabilities could have different repricing periods, with different base rates. For example, assets could reprice annually based on a 1-year rate and liabilities could reprice quarterly based on a 3-month base rate. Third, floating rate assets and liabilities could have base rates of different maturities, such as assets that reprice annually based on a long-term rate and liabilities that reprice annually based on a 1-year rate. Fourth, in countries with deregulated interest rates, banks can adjust pricing at will, and the rate-setting policies that banks follow determine the effective repricing behaviour of such instruments. The pricing decisions in these cases would then depend on a variety of factors in addition to market interest rates, such as the expected behaviour of bank customers and the extent of competition in the markets concerned. Finally, in some cases, bank customers have the option either to repay loans or withdraw their deposits at low (or no) cost, and the decisions of such customers would influence the response of the average pricing of such assets or liabilities to changes in market interest rates. Such repricing mismatches, though inherent to the business of banking, can expose a bank’s income and underlying economic value to unanticipated fluctuations as interest rates vary. For instance, a bank that funded a long-term fixed-rate loan with a short-term deposit could face a decline in both the future income arising from the position and its underlying value if interest rates increase. These declines arise because the cash flows on the loan are fixed over its lifetime, while the interest paid on the funding is variable, and increases after the short-term deposit matures.

- Yield curve risk: Even if, on an average, the yields on a bank’s assets and liabilities adjust to changes in market rates to the same extent, a bank may still be subject to yield curve risk. Yield curve risk is the possibility that changes in the shape of the yield curve7 could have differential effects on the bank’s assets and liabilities. For example, if a bank’s assets and liabilities reprice annually, it might want to balance a medium-term base rate for its assets with a mixture of short-term and long-term base rates for its liabilities. In that case, increased curvature of the yield curve would boost medium-term yields relative to short- and long-term yields, and thus raise the rate on the bank’s assets relative to the average cost of its liabilities, and reduce short-term earnings volatility.

Repricing mismatches can also expose a bank to changes in the slope and shape of the yield curve. Yield curve risk arises when unanticipated shifts of the yield curve have adverse effects on a bank’s income or underlying economic value. Annexure I provides an overview of the theory of interest rates, to enable understand the concept of yield curves.

- Basis risk: If the instruments have different base rates, the bank will be subject to basis risk. For example, yields on a bank’s floating rate assets could be tied to government security yields, while those on its floating rate liabilities could be based on an interbank rate such as the Libor. There is a possibility that the two base rates will diverge unexpectedly owing to differing credit risk or liquidity characteristics, which might increase private yields relative to government yields. In that case, the cost of bank liabilities would increase, relative to the yield on assets, thus lowering the bank’s earnings.

- Optionality: An increasingly important source of interest rate risk arises from the options embedded in many bank assets, liabilities, and off-balance sheet portfolios. Simply stated, an option provides the holder the right, but not the obligation, to buy, sell, or in some manner alter the cash flow of an instrument or financial contract. Options may be stand-alone such as exchange-traded options and over-the-counter (OTC) contracts, or may be embedded within otherwise standard instruments. While banks use exchange-traded and OTC options in both trading and non-trading accounts, instruments with embedded options are generally more important in non-trading activities. For example, bonds/securities may include options. Call options are typically exercised by the issuers to redeem bonds before maturity, while put options are exercised by investors to seek redemption before maturity. Such options could expose banks to interest rate risk. For example, if call option on the bonds are exercised when interest rates are declining, the bank investing in these bonds would run a ‘reinvestment risk’, since the intermediate cash flows from bond redemption would have to be reinvested at a lower rate. If, on the other hand, the bank has issued bonds with a put option, and interest rates are rising, the bank would face a ‘prepayment risk’ when investors seek redemption before maturity. The bank, in such cases, may have to borrow from the market at higher rates to pay the bondholders. Both these options, therefore, would cause earnings volatility for the bank.

Other examples of instruments with embedded options would be loans that give borrowers the right to prepay balances, or transaction deposit instruments that give depositors the right to withdraw funds at any time, often without any penalties.

If not adequately managed, the asymmetrical payoff characteristics of instruments with optionality features can pose significant risk particularly to those who sell them, since the options held, both explicit and embedded, are generally exercised to the advantage of the holder and the disadvantage of the seller. Moreover, an increasing array of options can involve significant leverage which can magnify the influences (both negative and positive) of option positions on the financial condition of the firm.

- Other sources of risk: Banks may also be subject to interest rate risk through interest sensitivity of their non-interest income. For example, lower interest rates could lead to prepayments (with the intention of refinancing the loans) that deplete the pool of loans serviced by a bank, thereby reducing its fee income, and also leading to a ‘prepayment’ risk. In a declining interest rate scenario, the cash inflows from prepayments could be invested only at lower rates, thus leading to more earnings volatility. More significant would be the substantial interest rate exposures embedded in the off-balance sheet positions of large banks, held either as a hedge for their on-balance sheet interest rate exposures or as a result of their trading activity in derivatives markets.

In order to understand interest rate risk, one has to understand the nature of interest rates. The management of interest rate risk depends substantially on predicting how interest rates would behave in future. If interest rates can be forecasted with a great deal of accuracy, interest rate risk is mitigated to a very large extent. Predicting future interest rates essentially involves predicting the shape of the future ‘yield curve’. Annexure I provides an overview of the various theories of interest rates, and how they could be used in predicting interest rate movements.

Interest rate risk in the banking book – Basel committee standards – Salient features

(Source: The Basel Committee on Banking Supervision, April 2016, “Standards : Interest rate risk in the Banking Book (IRRBB)” (http://www.bis.org/bcbs/publ/d368.pdf).

The concepts embodied in the foregoing part of this section is reflected in the current Basel committee standards on interest rate risk, its measurement and management.

In the global scenario following the financial crisis of 2007, interest rates in many countries are at very low levels, with some countries staring at negative interest rates. When interest rates normalize in the future banks in these countries would face a significant interest-rate risk.

IRRBB refers to the current or prospective risk to a bank’s capital and to its earnings, arising from the impact of adverse movements in interest rates on its banking book.

When interest rates change, the present value and timing of future cash flows change. This in turn changes the underlying value of a bank’s assets, liabilities and off-balance sheet items and hence its economic value (EVE). Changes in interest rates also affect a bank’s earnings by altering interest rate-sensitive income and expenses, affecting its net interest income (NII). Excessive IRRBB can pose a significant threat to a bank’s current capital base and/or future earnings if not managed appropriately.

The document includes the revised Principles, which replace the 2004 IRR (Interest Rate Risk) Principles for defining supervisory expectations on the management of IRRBB. Banks are expected to implement the revised standards by 2018. (Banks whose financial year ends on 31 December would have to provide the disclosure in 2018, based on information as of 31 December 2017.)

Types of risks

The Basel document identifies three main sub-types of interest rate risk. It is noteworthy that all three sub-types of IRRBB potentially change the price/value or earnings/costs of interest rate sensitive assets, liabilities and/or off-balance sheet items in a way, or at a time, that can adversely affect a bank’s financial condition

- Gap risk arises from the term structure of banking book instruments, and describes the risk arising from the timing of instruments’ rate changes. The extent of gap risk depends on whether changes to the term structure of interest rates occur consistently across the yield curve (parallel risk) or differentially by period (non-parallel risk).

- Basis risk describes the impact of relative changes in interest rates for financial instruments that have similar tenors but are priced using different interest rate indices.

- Option risk arises from option derivative positions or from optional elements embedded in a bank’s assets, liabilities and/or off-balance sheet items, where the bank or its customer can alter the level and timing of their cash flows. Option risk can be further characterised into automatic option risk and behavioural option risk.

Apart from the above three risks directly linked to the interest rate risk, there is a related risk that has to be measured and monitored for interest rate risk management. The Committee calls it Credit Spread Risk in the Banking Book (CSRBB)

CSRBB refers to any kind of asset/liability spread risk of credit-risky instruments that is not explained by IRRBB and by the expected credit/jump to default risk.

Revised Principles for IRRBB

There are 12 revised principles, as compared with the 15 Principles in the 2004 guidelines. The key enhancements in the revised principles are given below:

- An updated Standardized framework: The choice before the Committee was to shift the emphasis of interest rate risk management from Basel Pillar 1 to Pillar 2, or an enhanced Pillar 2 approach. Pillar 1 approach would apply a standardized regulator-designed approach with minimum capital requirements, and the existing Pillar 2 relied more banks’ internal measures that also covered elements of Pillar 3 on market discipline. After extensive discussions and industry feedback, a Standardized Pillar 2 framework was proposed. (For more details on Pillar 1 and Pillar 2 of the Basel Committee standards, please refer to the previous chapter- Capital- Risk, Regulation and Adequacy)

- More extensive guidance on the expectations for a Bank’s IRRBB management process: Greater guidance has been provided in areas such as the development of shock and stress scenarios, the key behavioural and modelling assumptions and internal validation for the banks’ Internal Measurement System (IMS) and models, while measuring and managing interest rate risk. This kind of standardization is expected to promote uniformity among practices followed by banks

- Updated disclosure requirements to promote greater consistency, transparency and comparability: Banks must disclose, among other requirements, the impact of interest rate shocks on their change in Economic value of equity (∆EVE) and net interest income (∆NII), computed based in a set of prescribed interest rate shock scenarios

- Stricter criteria for outlier banks: Supervisors are required to publish tightened criteria, which should include comparison between the bank’s ∆EVE with 15% of its tier 1 capital (Tier 1 capital is described in the previous chapter) under a set of prescribed interest rate shock scenarios

Principles for Banks

Principle 1: IRRBB is an important risk for all banks that must be specifically identified, measured, monitored and controlled. In addition, banks should monitor and assess CSRBB.

Principle 2: The governing body of each bank is responsible for oversight of the IRRBB management framework, and the bank’s risk appetite for IRRBB. Monitoring and management of IRRBB may be delegated by the governing body to senior management, expert individuals or an asset and liability management committee (henceforth, its delegates). Banks must have an adequate IRRBB management framework, involving regular independent reviews and evaluations of the effectiveness of the system

Risk Management framework

Principle 3: The banks’ risk appetite for IRRBB should be articulated in terms of the risk to both economic value and earnings. Banks must implement policy limits that target maintaining IRRBB exposures consistent with their risk appetite.

Principle 4: Measurement of IRRBB should be based on outcomes of both economic value and earnings-based measures, arising from a wide and appropriate range of interest rate shock and stress scenarios.

Principle 5: In measuring IRRBB, key behavioural and modelling assumptions should be fully understood, conceptually sound and documented. Such assumptions should be rigorously tested and aligned with the bank’s business strategies.

Principle 6: Measurement systems and models used for IRRBB should be based on accurate data, and subject to appropriate documentation, testing and controls to give assurance on the accuracy of calculations. Models used to measure IRRBB should be comprehensive and covered by governance processes for model risk management, including a validation function that is independent of the development process.

Principle 7: Measurement outcomes of IRRBB and hedging strategies should be reported to the governing body or its delegates on a regular basis, at relevant levels of aggregation (by consolidation level and currency).

Principle 8: Information on the level of IRRBB exposure and practices for measuring and controlling IRRBB must be disclosed to the public on a regular basis.

Principle 9: Capital adequacy for IRRBB must be specifically considered as part of the Internal Capital Adequacy Assessment Process (ICAAP) approved by the governing body, in line with the bank’s risk appetite on IRRBB.

Principles for Supervisors

Principle 10: Supervisors should, on a regular basis, collect sufficient information from banks to be able to monitor trends in banks’ IRRBB exposures, assess the soundness of banks’ IRRBB management and identify outlier banks that should be subject to review and/or should be expected to hold additional regulatory capital.

Principle 11: Supervisors should regularly assess banks’ IRRBB and the effectiveness of the approaches that banks use to identify, measure, monitor and control IRRBB. Supervisory authorities should employ specialist resources to assist with such assessments. Supervisors should cooperate and share information with relevant supervisors in other jurisdictions regarding the supervision of banks’ IRRBB exposures.

Principle 12: Supervisors must publish their criteria for identifying outlier banks. Banks identified as outliers must be considered as potentially having undue IRRBB. When a review of a bank’s IRRBB exposure reveals inadequate management or excessive risk relative to capital, earnings or general risk profile, supervisors must require mitigation actions and/or additional capital.

The standardised framework

Supervisors could mandate their banks to follow the framework set out in this section (section IV), or a bank could choose to adopt it.

Overall structure of the standardised framework

The steps involved in measuring a bank’s IRRBB, based solely on EVE, are:

Stage 1. Interest rate-sensitive banking book positions are allocated to one of three categories (ie amenable, less amenable and not amenable to standardisation).

Stage 2. Determination of slotting of cash flows based on repricing maturities. This is a straightforward translation for positions amenable to standardisation. (Amenable positions fall into two categories—fixed rate positions and floating rate positions—and include positions with embedded automatic interest rate options )

For positions less amenable to standardisation, they are excluded from this step. For positions with embedded automatic interest rate options, the optionality should be ignored for the purpose of slotting of notional repricing cash flows. A common feature of less amenable positions is the optionality that makes the timing of notional repricing cash flows uncertain.

Positions not amenable to standardization include non-maturity deposits (NMD), fixed rate loans subject to prepayment risk, and term deposits subject to early redemption risk. For positions that are not amenable to standardisation, there is a separate treatment for:

- NMD (Non Maturity Deposits) – according to separation of core and non-core cash flows via the approach set out in paragraphs 109 to 114.

- Behavioural options (fixed rate loans subject to prepayment risk and term deposits subject to early redemption risk) – behavioural parameters relevant to the position type must rely on a scenario-dependent look-up table set out in paragraphs 123 and 128.

Stage 3. Determination of ∆EVE for relevant interest rate shock scenarios for each currency. The ∆EVE is measured per currency for all six prescribed interest rate shock scenarios.

Stage 4. Add-ons for changes in the value of automatic interest rate options (whether explicit or embedded) are added to the EVE changes. Automatic interest rate options sold are subject to full revaluation (possibly net of automatic interest rate options bought to hedge sold interest rate options) under each of the six prescribed interest rate shock scenarios for each currency. Changes in values of options are then added to the changes in the EVE measure under each interest rate shock scenario on a per currency basis.

Stage 5. IRRBB EVE calculation. The ∆EVE under the standardised framework will be the maximum of the worst aggregated reductions to EVE across the six supervisory prescribed interest rate shocks

Components of the standardised framework

Cash flow bucketing

Banks must project all future notional repricing cash flows arising from interest rate-sensitive:

- assets, which are not deducted from Common Equity Tier 1 (CET1) capital and which exclude (i) fixed assets such as real estate or intangible assets and (ii) equity exposures in the banking book;

- liabilities (including all non-remunerated deposits), other than CET1 capital under the Basel III framework; and

- off-balance sheet items; onto

- 19 predefined time buckets (indexed numerically by kk as set out in Table 1, page 23) into which they fall according to their repricing dates, or onto

- the time bucket midpoints (as set out in Table 1), retaining the notional repricing cash flows’ maturity.

A notional repricing cash flow CF(kk) is defined as:

- any repayment of principal (eg at contractual maturity);

- any repricing of principal; repricing is said to occur at the earliest date at which either the bank or its counterparty is entitled to unilaterally change the interest rate, or at which the rate on a floating rate instrument changes automatically in response to a change in an external benchmark; or

- any interest payment on a tranche of principal that has not yet been repaid or repriced;

- The date of each repayment, repricing or interest payment is referred to as its repricing date.

- Floating rate instruments are assumed to reprice fully at the first reset date. Hence, the entire principal amount is slotted into the bucket in which that date falls, with no additional slotting of notional repricing cash flows to later time buckets or time bucket midpoints

Calculation of change in Economic Value of Equity (∆EVE)

- Banks should exclude their own equity from the computation of the exposure level.

- Banks should include all cash flows from all interest rate-sensitive assets, liabilities and off-balance sheet items in the banking book in the computation of their exposure. (Interest rate-sensitive assets are assets which are not deducted from Common Equity Tier 1 (CET1) capital and which exclude (i) fixed assets such as real estate or intangible assets as well as (ii) equity exposures in the banking book).

- Cash flows should be discounted using either a risk-free rate or a risk-free rate including commercial margins and other spread components (only if the bank has included commercial margins and other spread components in its cash flows).

- ∆EVE should be computed with the assumption of a run-off balance sheet, where existing banking book positions amortise and are not replaced by any new business. (As against this, in the constant balance sheet, total balance sheet size and shape are maintained by assuming like-for-like replacement of assets and liabilities as they run off. The maturing or repricing cash flows are replaced by new cash flows with identical features with regard to the amount, repricing period, and spread components.)

Calculation of change in projected Net Interest Income (∆NII)

- Banks should include expected cash flows (including commercial margins and other spread components) arising from all interest rate-sensitive assets, liabilities and off balance sheet items in the banking book.

- ∆NII should be computed assuming a constant balance sheet, where maturing or repricing cash flows are replaced by new cash flows with identical features with regard to the amount, repricing period and spread components.

- ∆NII should be disclosed as the difference in future interest income over a rolling 12-month period.

Components of interest rates

(Annex I of Basel document, Section 1.3. page 33)

Every interest rate earned by a bank on its assets, or paid on its liabilities, is a composite of a number of price components – some more easily identified than others. Theoretically, all rates contain five elements:

- The risk-free rate: this is the fundamental building block for an interest rate, representing the theoretical rate of interest an investor would expect from a risk-free investment for a given maturity.

- A market duration spread: the prices/valuations of instruments with long durations are more vulnerable to market interest rate changes than those with short durations. To reflect the uncertainty of both cash flows and the prevailing interest rate environment, and consequent price volatility, the market requires a premium or spread over the risk-free rate to cover duration risk.

- A market liquidity spread: even if the underlying instrument were risk-free, the interest rate may contain a premium to represent the market appetite for investments and the presence of willing buyers and sellers.

- A general market credit spread: this is distinct from idiosyncratic credit spread, and represents the credit risk premium required by market participants for a given credit quality (eg the additional yield that a debt instrument issued by an AA-rated entity must produce over a risk-free alternative).

- Idiosyncratic credit spread: this reflects the specific credit risk associated with the credit quality of the individual borrower (which will also reflect assessments of risks arising from the sector and geographical/currency location of the borrower) and the specifics of the credit instrument (eg whether a bond or a derivative).

In theory these rate components apply across all types of credit exposure, but in practice they are more readily identifiable in traded instruments (eg bonds) than in pure loans. The latter tend to carry rates based on two components:

- The funding rate, or a reference rate plus a funding margin: the funding rate is the blended internal cost of funding the loan, reflected in the internal funds transfer price (for larger and more sophisticated banks); the reference rate is an externally set benchmark rate, such as Libor or the federal funds rate, to which a bank may need to add (or from which it may need to subtract) a funding margin to reflect its own all-in funding rate. Both the funding rate and the reference rate incorporate liquidity and duration spread, and potentially some elements of market credit spread. However, the relationship between the funding rate and market reference rate may not be stable over time – this divergence is an example of basis risk.

- The credit margin (or commercial margin) applied: this can be a specific add-on (eg Libor + 3%, where the 3% may include an element of funding margin) or built into an administered rate (a rate set by and under the absolute control of the bank).

In practice, decomposing interest rates into their component parts is technically demanding and the boundaries between the theoretical components cannot easily be calculated (eg changes to market credit perceptions can also change market liquidity spreads). As a result, some of the components may be aggregated for interest rate risk management purposes. Changes to the risk-free rate, market duration spread, reference rate and funding margin all fall within the definition of IRRBB. Changes to the market liquidity spreads and market credit spreads are combined within the definition of CSRBB.

Diagram 12.1 gives a visual representation of how the various elements fit together.

DIAGRAM 12.1 VARIOUS COMPONENTS OF INTEREST RATES

IRRBB and CSRBB

The main driver of IRRBB is a change in market interest rates, both current and expected, as expressed by changes to the shape, slope and level of a range of different yield curves that incorporate some or all of the components of interest rates.

When the level or shape of a yield curve (see Annexure I of this chapter) for a given interest rate basis changes, the relationship between interest rates of different maturities of the same index or market, and relative to other yield curves for different instruments, is affected. This may result in changes to a bank’s income or underlying economic value.

CSRBB is driven by changes in market perception about the credit quality of groups of different creditrisky instruments, either because of changes to expected default levels or because of changes to market liquidity. Changes to underlying credit quality perceptions can amplify the risks already arising from yield curve risk. CSRBB is therefore defined as any kind of asset/liability spread risk of credit-risky instruments which is not explained by IRRBB, nor by the expected credit/jump-to-default risk.

This Basel document focuses mainly on IRRBB. CSRBB is a related risk that needs to be monitored and assessed.

We have seen earlier in this chapter that a bank’s ALCO, alternatively known as the ‘Risk Management committee’ is responsible for measuring and monitoring interest rate risk. This brings us to the next important question: How do we measure interest rate risk, with all the complexities described above?

Measuring Interest Rate Risk8

Banks use various techniques to measure the exposure of earnings and economic value to changes in interest rates. These techniques range from simple calculations relying on basic maturity and repricing tables based on current and projected on- and off-balance sheet positions, to highly sophisticated dynamic modelling techniques. These measures can assess interest rate risk exposure from the earnings, or economic view perspectives or both. The methods also vary in their ability to capture different forms of interest rate exposure—the simpler methods aim at capturing risks arising from maturity and repricing mismatches, while the more sophisticated methods are designed to capture a fuller range of risk exposures.

An ideal approach to measuring interest rate risk would have to capture the entire range of potential movements in interest rates, taking into account specific characteristics of each interest rate sensitive asset and liability of a bank. However, this may not be possible in practice, and simplified assumptions will have to be incorporated into the approaches. Hence, the various measurement approaches would have their unique strengths and weaknesses in terms of accurately and realistically measuring interest rate risk exposure of a bank. For instance, in some approaches, positions may be aggregated into broad categories, rather than taken separately, injecting a degree of measurement error into the estimation of their interest rate sensitivity. In some approaches, the nature of interest rate movements that can be incorporated may be limited. In other approaches, only a parallel shift of the yield curve may be assumed or less than perfect correlations between interest rates may not be taken into account. Importantly, the various approaches differ in their ability to capture the optionality inherent in many positions and instruments.

Before we examine the various approaches, we will have to understand what determines interest rate ‘sensitivity’. Typically, a bank’s asset or liability is classified as rate sensitive within a specified time interval or ‘bucket’, if:

- It matures during the time interval.

- The interest rate applied to the outstanding advance changes contractually during the interval.

- It represents an interim or partial principal payment.

- The outstanding principal can be repriced when some base rate or index changes, and there is an expectation that the base rate or index may change during the interval.

We will elucidate further. For example, if the bank is considering interest rate risk that would arise in the 0–90 day time interval, the primary issue will be to identify the assets and liabilities on the balance sheet that will be repriced during the ensuing 90 day period, given the specific interest rate forecast or expectation. Any asset or liability that matures during this period will have to be repriced since the bank must reinvest the proceeds from the asset. Similarly, any deposit that matures for payment during this period will have to be replaced, or the deposit rate will have to be reset. Thus, any investment security, loan, deposit, or longer-term liabilities or assets that mature during this 90-day period would be ‘rate sensitive’. In more general terms, any principal payment expected to be received during this 90-day period—final or interim—is rate sensitive. Further, some assets and liabilities earn or pay rates that are contractually linked to a changing index or base rate. These instruments are termed ‘rate sensitive’ if a change is expected in the index or base rate during the 90-day period, since any change in the index or base rate will lead to repricing. However, even when there is no definite knowledge of when the base rate will change, the instrument will remain rate sensitive, since there is a possibility that its yield can change at any time.

TEASE THE CONCEPT

Are these assets and liabilities rate sensitive during a 6-month period?

- 3–month treasury bills.

- Short term consumer loans.

- Savings bank deposits.

- a 7–year floating rate industrial loan with semi annual interest payments.

- a 15–year fixed rate housing loan with quarterly interest payments.

There are several modelling approaches to judge a bank’s earnings and capital exposure to changing interest rates. The focus here is on three of the most popular of these approaches: Gap analysis, Earnings at Risk (EAR) models and Economic Value of Equity (EVE) models. Typically, Gap and EAR are used to assess earnings exposure to interest rate movements. EVE is used to assess capital risk.

Method 1: Measuring Interest Rate Risk—Traditional GAP Analysis Traditional GAP. models are the most basic interest rate risk exposure measurement techniques employed by banks. These models focus on GAP as a static measure of risk and NII as the target measure of bank performance.

This method requires preparation of a repricing gap report that distributes rate sensitive assets, rate sensitive liabilities and off-balance sheet positions into different time buckets according to their residual maturity or time remaining to their next repricing, whichever is earlier. The assets and liabilities that do not have contractual repricing intervals or maturities are assigned to maturity buckets based on statistical analysis or judgement. Interest rate risk is measured by calculating gaps over different maturity buckets. The GAP is defined as the absolute difference between Rate Sensitive Assets (RSA) and Rate Sensitive Liabilities (RSL) for each time bucket. Since interest rate risk is measured by calculating GAP over different time intervals based on aggregate balance sheet data at a fixed point in time, the measure is known as ‘static GAP’.

The objective is to measure expected NII and then identify strategies to stabilize or improve it. The steps to static GAP analysis are as follows:

- Forecasting interest rates for the time period during which interest rate risk is to be measured—based on historical experience, simulation of future interest rate movements, or management judgement.

- Determining a series of sequential time intervals, called ‘buckets’.

- Grouping assets and liabilities of the bank, including contingent liabilities, into these time intervals, according to the time until the first repricing. The effects of off-balance sheet positions, such as those associated with futures, interest rate swaps and so on, are added to the grouping, based on whether the item effectively represents a rate sensitive asset or liability.

- Calculating the bank’s static GAP as the difference between RSAs and RSLs for each time bucket.

- Multiplying the GAP by the forecasted interest rate to obtain expected NII.

Thus, there would be a periodic GAP and a cumulative GAP for each time bucket. For example, the cumulative GAP for the period 0–90 days would be the sum of, say, the periodic GAP of 0–28 days, 29–60 days and 61–90 days.

A negative, or liability-sensitive GAP occurs when liabilities exceed assets (including OBS positions) in a given time band. Conversely, a positive or asset-sensitive GAP occurs when the assets exceed liabilities.9

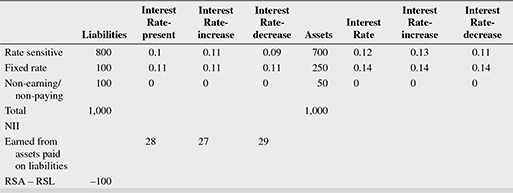

From Illustration 12.1, the effect of interest rate risk on the bank’s earnings can be gauged:

ILLUSTRATION 12.1

Balance sheet composition and average interest rates over a specified time interval, say, 1 year, for a hypothetical bank (₹ in crore) can be explained as follows:

Case 1 Rate sensitive assets exceed rate sensitive liabilities, hence GAP is positive.

Case 2 Rate sensitive liabilities exceed rate sensitive assets, hence GAP is negative.

The following inferences can be drawn from Illustration 12.1:

- When GAP is positive, it indicates that the bank has more RSAs than RSLs across the time interval. Such a bank is termed as ‘asset sensitive’

- When GAP is positive, and interest rates rise by equal amounts at the same time for both assets and liabilities, NII increases. The bank would then be paying higher rates on all repriceable liabilities over the time horizon, and earning higher yields on repriceable assets. However, since more assets are repriced than liabilities, NII increases.

- When GAP is positive, and interest rates decrease by equal amounts at the same time for both assets and liabilities, NII decreases for the reason discussed above.

- When GAP is negative, it indicates that the bank has more RSLs than RSAs across the time interval. Such a bank is termed ‘liability sensitive’.

- When GAP is negative, and interest rates rise by equal amounts at the same time for both assets and liabilities, NII decreases. Though both interest income and interest expenses increase, the latter rise more because more liabilities are repriced.

- When GAP is negative, and interest rates fall by equal amounts at the same time for both assets and liabilities, NII increases for the reason discussed in (5).

- Therefore, the sign of a bank’s GAP would indicate whether interest income or interest expenses are likely to change more when interest rates change.

- It also follows that the bank can have a ‘zero GAP’ when RSAs equal RSLs. In this case, equal interest rate changes do not alter NII since changes in interest income equal changes in interest expenses.

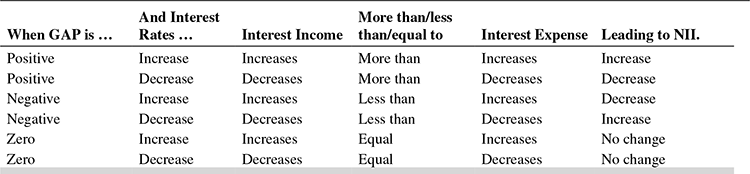

These findings can be generalized in the Table 12.2.

TABLE 12.2 CHANGES IN GAP—SUMMARY OF RESULTS

The following simple formula summarizes the framework:

Where ∆NII [expected] represents change in NII from an existing base over a specified period of time,

GAP represents cumulative GAP over the chosen time interval, and

∆r[expected] represents expected changes in the interest rates over the time period

The sign and magnitude of the gaps in various time buckets can be used to assess potential earnings volatility arising from changes in interest rates. A positive gap indicates that RSA are more than RSL and from an earnings perspective, the position benefits from a rise in interest rates. A negative gap on the other hand indicates that RSL are more than RSA and from an earnings perspective the position would benefit from a fall in interest rates. The size of the GAP indicates how much interest rate risk a bank assumes. The utility of this simple approach is that banks can take positions to improve NII for a given level of GAP and forecast of rise or fall in interest rates.

Strengths and weaknesses of this approach: Static Gap analysis is one of the most commonly used approaches to assessing interest rate risk exposure. The principal advantage of this approach is that it is easy to understand and compute. Specific balance sheet items responsible for the risk can be clearly identified, and, once cash flow characteristics of each instrument are determined, GAP measures can be easily calculated.

However, the approach has a number of shortcomings.

First, the analysis makes the simplifying assumption that all positions within a time band mature or reprice simultaneously, thus leading to aggregation that might impact precision of the estimates.

Second, the analysis ignores ‘basis risk’, which arises when loans and other instruments are tied to different base rates or indexes. It is not easy to forecast the frequency or magnitude of changes in market-driven base rates or indexes. This could lead to serious measurement errors.

Third, the analysis ignores the time value of money. The maturity buckets do not clarify whether cash flows arise at the beginning of the period or at the end. For example, if investment in a 1-month treasury bill is financed by an overnight borrowing in the money market, the 1-month GAP is zero, and suggests no interest rate risk. However, when overnight rates rise, the transaction exposes the bank to losses. Therefore, a bank’s gains or losses could also arise from the timing of the repricing or the interest flows within each time interval. Thus even with a zero GAP, the bank’s NII may fluctuate.

Fourth, the short-term focus of GAP measures ignores the long-term impact on fixed rate assets and liabilities. Interest rate changes could have long-term effects on the total risk of the bank’s assets and liabilities.

Fifth, the rate sensitivity of liabilities that bear no interest is ignored. Many banks consider non-interest bearing demand deposits as non-rate sensitive. When interest rates fluctuate, customers’ willingness to maintain demand deposits with banks also changes. It is thus difficult to estimate the exact rate sensitivity of such instruments.

Sixth, the analysis fails to account for differences in the sensitivity of income arising from options embedded in the securities and deposits that banks deal with. Depositors have the option of withdrawing their money before maturity. Similarly, long-term borrowers have the option of prepaying and foreclosing their loans. Such options have different probabilities of being exercised at different interest rate levels. If they are exercised, they can alter the GAP and, hence, the NII as well.

Finally, most GAP analyzes fail to capture variability in non-interest revenue and expenses due to interest rate fluctuations. Volatility in non-interest revenue and expenses is a potentially important source of risk to current net income of the bank.

Hence, GAP analysis, though prevalently used, would provide only a rough approximation of the actual change in NII resulting from the forecasted pattern of change in interest rates. The sign of the GAP does not impact the volatility of NII. It merely indicates whether NII rises or falls when interest rates are expected to fluctuate.

Measuring interest rate risk—Linking the GAP and net interest margin. Some ALM measures focus on the ‘GAP ratio’ while evaluating interest rate risk. The GAP ratio is defined as the ratio of RSAs to RSLs. Thus

When the GAP is positive, the GAP ratio is greater than unity. When the GAP is negative, the GAP ratio will be less than unity.

However, the deficiency in this measure is that does not reflect the size of the interest rate risk a bank assumes. Illustration 12.2 depicts this feature.

ILLUSTRATION 12.2

| Bank A (₹ in crore) | Bank B (₹ in crore) | |

|---|---|---|

| Total assets | 1,000 | 1,000 |

| RSAs | 40 | 400 |

| RSLs | 20 | 200 |

| GAP (RSAs – RSLs) | 20 | 200 |

| GAP ratio (RSAs/RSLs) | 2 | 2 |

| NII (assumed) | 200 | 400 |

| Decrease in interest rate | 2% | 2% |

| Change in NII (GAP × ∆r) | –0.4 | –4 |

In the above example, though the asset size and the GAP ratio are identical for both banks; it is evident that Bank B assumes greater risk since its interest income will be more volatile when interest rates change.

Since interest rate risk is more associated with the volatility in NII, a better risk measure would be one that relates the absolute value of a bank’s GAP to its assets—particularly the earning assets. This ratio can be directly linked to the NIM10 of the bank (see Box 12.3)—the greater this ratio, the greater would be the interest rate risk. The practical implications are that:

- the bank management can determine a target NIM based on the specific risk characteristics of its assets.

- it can determine an allowable variation in the NIM without affecting stakeholder interests.

- based on the above, an acceptable GAP is arrived at.

BOX 12.3 RELATIONSHIP BETWEEN TARGET GAP, EARNING ASSETS AND NIM

The relationship can be evolved as follows:

Hence, NII = NIM × earning assets

The bank determines the acceptable variation in NIM as ∆c. Then, the acceptable variation in NII would be

Since ∆ NII = GAP × ∆r,

Effectively therefore, the relationship between Target GAP and Earning assets can be expressed as a ratio of the product of the expected NIM and the % variability in NIM that can be tolerated, to the expected change in interest rates.

For example, if a bank with earning assets of ₹100 crores expects NIM of 2.5 per cent, but can tolerate variability in the NIM to the extent of ±10 per cent during a year, NIM should fall between 2.25 per cent and 2.75 per cent. If, further, interest rates are forecasted to vary up to 2 per cent during the year, the bank’s ratio of 1-year cumulative target GAP to its earning assets should not exceed 12.5 per cent, as given by the final equation in Box 12.3.

Hence, the bank’s decision to allow only a 10 per cent variation in NIM limits the variation in GAP from –₹12.5 crores to +₹12.5 crores, based on ₹100 crores of earning assets.

It is important to note here the close relationship between a bank’s GAP and its NIM. Hence, in practice, banks limit the size of GAP as a fraction of earning assets, thus, limiting the variation in the NII.

Method 2: Measuring Interest Rate Risk—Earnings Sensitivity Analysis Earnings Sensitivity analysis is an extension of the static GAP analysis. It essentially assesses the impact on net income using ‘what if’ models, carrying out iterations of static GAP analysis assuming different interest rate forecasts and potential interest rate environments. The broad steps of the analysis are as follows:

Step 1 Forecast interest rates assuming various potential interest rate environments

Step 2 Assess the likely changes in the bank’s assets and liabilities by volume and composition under each of these likely environments. The assessment will also examine which of the potential interest rate environments would lead to exercise of embedded options such as loan prepayments or premature deposit withdrawals

Step 3 Assess the likelihood that assets and liabilities would reprice under each of the identified environments. Similarly, identify the implications on off-balance sheet items

Step 4 Calculate the NII under each of the environments, and compare with the ‘base case’ and other scenarios.

The above framework thus helps evaluate the impact of different interest rate environments on the NII, and allows the bank management to set limits for variability of NII or NIM. This approach is sometimes termed as Earning-at-Risk (EAR).

Method 3: Measuring Interest Rate Risk—Rate-Adjusted GAP This method is a simpler variation of the Earnings Sensitivity analysis method described above, and is typically used under circumstances where the complexity and size of a bank’s assets and liabilities and off-balance sheet items are not likely to change dramatically in the short run. The advantage of this approach is that, though simpler, it recognizes the existence of embedded options and different repricing timings. This method is also called ‘Income Statement GAP’ since it uses the balance sheet data to assess the differential impact of interest rate change on each asset and liability class of the bank.

The steps to adopting this approach are as follows:

Step 1 Assess the balance sheet GAP for all items in the balance sheet. This is done by including all balances whose rates are likely to change in, say, the next 12 months

Step 2 Compute the relevant ‘Earnings volatility factor’ (EVF) for each of the balance sheet items. The EVF would reflect the change in the rate applicable to a rate sensitive asset or liability for every 100 bps change in the base rate.

Step 3 The product of the balance sheet GAP and the EVF will reflect the ‘Income statement GAP’, which is the effective GAP estimate, were the interest rates to change as forecasted.

Step 4 Arrive at the impact on NII using the earlier formula

Similarly, the effect on NIM can also be determined using the formula given earlier.

The important advantage of this approach is that it recognizes the value of options and repricing timing in bank assets and liabilities, while being simple to compute. However, the results will depend on the skill of the forecaster to accurately judge the impact of interest rate changes on each class of assets and liabilities.

Illustration 12.3 depicts a simplified usage of this approach. In the example given in Illustration 12.1, we impose differing EVFs on the rate sensitive assets and liabilities.

ILLUSTRATION 12.3

It is evident that assuming different responses to interest rate changes by different assets and liabilities of the bank lead to conclusions quite at variance with the conclusions reached in Illustration 12.1. The rate sensitive GAP is negative and the change in NII is in the opposite direction.

It is, therefore, important that assumptions regarding interest rate movements and their impact on changes in rate sensitive liabilities and assets are done with care and precision in order that misleading conclusions are avoided.

Box 12.4 explores if yield curves do matter for banks’ profitability.

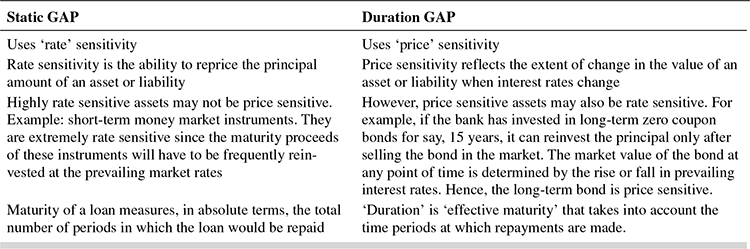

Method 4: Measuring Long-Term Interest Rate Risk—Duration GAP Analysis A fundamental criticism of the static GAP and Earnings Sensitivity analyzes pertain to their preoccupation with short-term interest rate risk in banks. A bank’s assets and liabilities, however, may be mismatched beyond 1 or 2 years and thus expose the bank to substantial risk in the medium or long term. Such risks may go undetected by the traditional GAP approaches.

Hence, banks will also have to look at alternate methods of measuring interest rate risk over the entire life of the assets and liabilities. Duration gap (DGAP) analysis is one such method. As the name suggests, it incorporates estimates of ‘duration’ of assets and liabilities that reflect the value of promised cash flows up to maturity. Hence, it is considered a more comprehensive interest rate risk measure.

Stated in its simplest form, ‘duration’ is the average life of an asset or liability, and is measured as the weighted average time to maturity using present value of the cash flows, relative to the total present value of the asset or liability as weights.

‘Duration’ measures the sensitivity of any instrument to a small change in any of the underlying risk factors. Simply, it is an elasticity measure, providing information on how much a security’s price will change with changes in market interest rates. Annexure II provides the basic concepts, applications and measurement approaches for ‘duration’ and ‘convexity’.

The reasons for using both static GAP and DGAP analyzes in estimating interest rate risk are outlined in Table 12.3.

BOX 12.4 DO YIELD CURVES MATTER FOR BANKS’ PROFITABILITY?

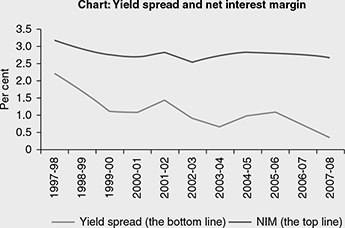

According to theory, it appears logical that the NIM of banks—the difference between interest received and paid as a percentage of earning assets—should be impacted by the slope of the yield curve, i.e., the spread between short- and long-term interest rates. Hence, a flattening yield curve would have an important macroeconomic impact—it may lead to slowing economic growth and consequent pressure on bank earnings. This relationship was seen to be true up to the 1990s. Figure 12.2 shows the trend in relationship in the case of banks in India.

FIGURE 12.2 TRENDS IN RELATIONSHIP BETWEEN YIELD SPREAD AND NIM IN INDIAN BANKS

Interestingly, in the recent past, banks’ NIMs appear to show lower sensitivity to yield curve movements. The RBI report on currency and finance (2006–08) attributes the following reasons to this new trend:(a) banks’ diversification into nontraditional activities, (b) banks’ increasing use of derivatives to hedge interest rate risk and(c) banks’ increasing use of noninterest bearing liabilities such as equity and demand deposits to fund assets, when interest yields on assets are declining.

In the case of India, the RBI report notes that there has been a flattening yield curve over the last decade (up to 2006–07). The reason attributed to this is the decline in long-term rates and relative stability of short-term rates. The report also points out that the NIM follows yield spreads with a lag, possibly because lending and borrowing rates of banks are not adjusted instantly to market rate movements.

TABLE 12.3 COMPARISON OF BASIC FEATURES OF STATIC GAP AND DURATION GAP

TEASE THE CONCEPT

As ‘maturity’ of a loan increases, what happens to its ‘duration’?

DGAP analysis examines how interest rate changes would affect the market value of shareholder equity. Similar to the static GAP analysis, the duration of assets and liabilities of a bank are compared over different interest rate environments. After evaluating the impact of interest rate change on the market value of shareholder equity, the DGAP analysis also throws up options for bank management to immunize or insulate market value of equity (MVE) from rate changes.

The steps involved in DGAP analysis are as follows:

Step 1 Forecast interest rate changes for the planning horizon

Step 2 Estimate current market value of the bank’s assets, liabilities and shareholders’ equity

Step 3 Estimate the weighted average duration of assets and the weighted average duration of liabilities, also incorporating the effects of off-balance sheet items, based on the estimated market values.

Step 4 Calculate DGAP

Step 5 Forecast changes in the bank’s MVE under various interest rate environments.

Step 6 Formulate strategies to insulate MVE from interest rate volatility

Box 12.5 derives the relationship between DGAP and the market value of assets and liabilities of a bank.

BOX 12.5 DERIVING THE RELATIONSHIP BETWEEN MVA, MVL AND MVE

The weighted average duration of a bank’s assets is calculated as

and the variables are defined as follows:

wai = the market value of each asset ‘ai’ of the bank divided by the market value of all bank assets (MVA = a1 + a2 + … + an)

Dai = Macaulay’s duration11 of the ith asset

n = number of different bank assets

The weighted average duration of bank liabilities (Dl) is calculated as follows:

And the variables are defined as follows:

wlj = the market value of each liability ‘lj’ of the bank divided by the market value of all bank liabilities (MVL = l1 + l2 + … + lm)

Dlj = Macaulay’s duration of liability j and

m = number of different bank liabilities

We know that Duration is a measure of interest rate sensitivity or elasticity of a liability or asset, which can be represented as follows:

From the above basic equation, we can represent ![]() representing the interest rate.

representing the interest rate.

Since the focus is on insulating MVE from interest rate risk, let us define MVE as the difference between market value of assets and the market value of liabilities, i.e.,

implying that changes in MVE would result from changes in the market values of assets and liabilities.

In the same manner used to determine the change in price given above, we can find the change in the MVE using duration

The expression ![]() is the DGAP, and hence

is the DGAP, and hence

The important point to be noted from the expression denoting MVE are as follows:

- The weighted average duration of both assets and liabilities reflect the present value of all promised cash flows in future. Therefore, the need for classifying assets and liabilities into time buckets does not arise.

- The DGAP is ‘leverage adjusted’. Note that DGAP is the difference between weighted average duration of assets and a ‘leverage-adjusted’ weighted average duration of liabilities. This implies that DGAP serves as a rough estimate of the sensitivity of MVE to interest rate changes. The leverage adjustment also denotes how much equity is present to finance the assets and cushion unexpected losses. The interest rate r typically represents an average yield on earning assets. The interest rate assumed here would be an ‘economic interest’ that generates ‘economic income’ as contrasted with ‘accounting income’. ‘Economic Interest’ is simply the product of the market value of each asset and liability and its market interest rate.

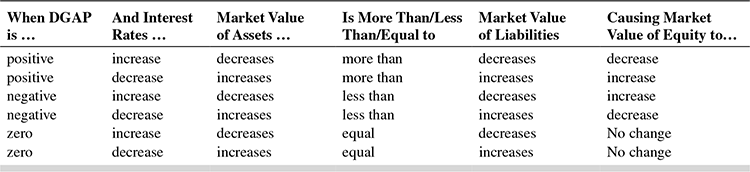

- The greater the DGAP, the greater would be the size of the ‘interest rate shock’—the potential volatility in the MVE for a given change in interest rates. Therefore, DGAP serves as a measure of the interest rate risk assumed by the bank, as well as gains and losses to the bank arising from interest rate movements. For example, when DGAP is positive, an increase in interest rates would lower the MVE, while a decrease in interest rates would have an opposite effect and increase the MVE. And when DGAP is negative, an increase in interest rates would increase the MVE while a decrease in interest rates would lower the MVE. These results are in sharp contrast to those from similar static GAP analysis. It also follows that the closer the DGAP is to zero, the smaller the potential change in MVE.

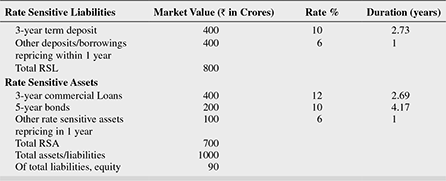

Continuing with the example given in Illustrations 12.1 to 12.3, let us see how duration analysis can be applied to the data. This is demonstrated in Illustration 12.4.