CHAPTER EIGHTEEN

Insurance Services

Chapter Structure

Section II The Insurance Sector—An Overview

Section III Banks and Insurance Services—Bancassurance in India

Section IV The Global Insurance Industry—Opportunities and Challenges

Key TakeAways From The Chapter

- Understand the principles on which insurance is based on, and the broad classification of insurance products.

- Review the past, present and future of insurance sector.

- Look at the functioning of organizations like LIC, GIC and ECGC.

- Learn the process of liberalization in the insurance sector and look at new private sector firms.

- Learn why bancassurance adds value.

SECTION I

BASIC CONCEPTS

Insurance is a protection against a financial loss, arising on the happenings of an unexpected event. Insurance is a contract between two parties whereby one party called insurer takes a fixed sum called premiums, in exchange to pay the other party on the happening of a certain event. A loss is paid out of this premium collected from the insuring public. The insurance company acts as a trustee for the amount collected through these premiums. Insurance is generally classified into three main categories—life insurance, health insurance and general insurance. In order to get insured, an individual or an organization can approach an insurance company directly, through an insurance agent of the concerned company or through intermediaries.

In legal terms, insurance is a ‘uberrimae fidae’ contract—a contract of ‘utmost good faith’. The compensation is contingent upon happening or non happening of a certain event. Insurance provides monetary compensation for the loss, damage or death, provided it falls within the framework of the specific terms of the insurance contract.

What will the amount of compensation of ‘loss’ be based on? The most important factor is ‘value’ – perceived value of the insured object or its potential value in future, or the value for which insurance has been taken. This implies that only those entities or activities that have ascertainable value can be insured. Assessment of ‘value’ is possible in all ‘non life’ (general insurance) contracts – say, insurance on property or vehicles – where the current market price as well as the future revenue generating capacity of the asset can be evaluated with reasonable data or assumptions.

But how does one value ‘life’ – and hence ‘life insurance’? Unlike general insurance, no compensation can be considered adequate for loss of life. In fact, what is compensated is the loss of future income of the individual whose life was insured. Of course, this value would again depend on the age, health and earning capacity of the individual. Once a value is placed on these factors, the policy ‘insures’ the life. Hence, the essential difference between life and general insurance is that life insurance considers the future stream of cash that the insured person would be able to generate over his/her lifetime, while general insurance considers the present value of future cash flows possible from the asset.

Box 18.1 provides an illustrative list of the important terminologies used in respect of Insurance.

BOX 18.1 AN ILLUSTRATIVE LIST OF UNIQUE INSURANCE TERMINOLOGIES

Policy: The contract sold by the Insurance company

Policy falling due: Date of payment by insurance company—either due to contract terms or because the insured risk has translated into actual loss. Once a policy falls due for payment (as in the case of life insurance), the ‘life’ of the policy is over and insurance cover under the policy is no more available.

Premium: The amount to be paid by the insured person to enter into the contract or to maintain continuity of the policy.

Sum insured: The amount promised by the insurance company in case of claim at maturity, as in the case of life insurance or when actual loss occurs.

Surrender value: This term is applicable to life insurance policies. In case the person who has taken insurance decides to discontinue paying premiums after a few years before maturity, the insurance company would pay back ‘surrender value’, a value less than the actual amount of premiums already paid.

Assurance versus insurance: Though both terms are often used interchangeably, there is a subtle difference. Insurance refers to protection against loss that may or may not happen, as in the case of fire or theft. Assurance is protection against an event that is bound to occur sooner or later. Hence, ‘life assurance’ is possible, but not ‘fire assurance’.

Basic features of Insurance Contracts

A contract of insurance should contain certain essential features. Though some of these features may be found in contracts other than insurance, the following are the characteristic features that every insurance contract should contain:

- Insurable interest: The person entering into the contract (buyer of insurance or policyholder) should have valid interest in the item being insured. This is called ‘insurable interest’. This implies that the policyholder should be able to establish that a loss incurred in the item being insured would lead to direct monetary loss to the policyholder. Any insurance contract without insurable interest is considered in the nature of ‘wagering contracts’. (In terms of Section 30 of the Indian Contracts Act, 1872, all wagering contracts are ‘null and void’).

Generally, one rule to establish insurable interest is through ownership of the assets being insured. However, in special cases, such as mortgagees and mortgagors, agents, executors and trustees or bailees, partial ownership of assets insured is recognized as insurable interest. There are also certain classes of insurance that do not demand proving insurable interest, such as accident insurance and certain life insurance contracts. For example, in the case of insurance taken on the life of the spouse, the relationship itself is sufficient to prove existence of insurable interest.

- Utmost good faith: As mentioned earlier, insurance contracts are ‘uberrimae fidae’ contracts. Voluntary disclosure of all information pertinent to the contracts is expected of both the insurer and the insured. Any material fact not disclosed at the time of entering into the contract, which is relevant to the contract, can render the contract null and void. Since it may not be possible in practice to conduct a thorough due diligence on every person or entity wishing to enter into an insurance contract, the agreements contain express ‘warranties’ from the insured and ‘disclosures’ from the insurer.

- Indemnification: Under a contract of indemnity, the indemnifier provides assurance to save the counterparty from loss, caused by the action of indemnifier or a third party. Hence, every contract of insurance is a contract of indemnity. However, the party, whose loss is being compensated, should seek compensation for the loss alone and not attempt to make a profit on the compensation. It is noteworthy that the principles of insurable interest and indemnification are complementary, since the entity receiving insurance should prove that it will suffer a loss to the extent of the sum assured.

- Subrogation: This is a corollary to the indemnification feature. It is the right of the insurer to take the place of the insured, after settlement of a claim (by the insurer) to enforce the right of recovery from the source that caused the loss. This means that if the insured suffers a loss due to the action of a third party and the insurance company has settled the insured’s claim, the insurance company can step into the shoes of the insured to recover the loss from the third party that caused the loss. Subrogation therefore ensures that all rights in respect of the insured asset are transferred to the insurance company once the loss in indemnified. However, if after subrogation, the insurance company is able to recover from the third party more than the indemnified value, the excess amount will have to be paid back to the insured.

It is to be noted that both ‘indemnification’ and ‘subrogation’ are not applicable to life insurance contracts.

- Warranties: These are corollaries of ‘uberrimae fidae’, and are written as conditions in insurance contracts. These are explicit or express warranties. There are also ‘implicit’ or ‘implied’ warranties, such as ‘affirmative’ or ‘promissory’ warranties. For example, in marine insurance, an express warranty may be that the ship is seaworthy for a particular journey, or it would take a specified route to its destination. The implied warranties in this case would be that the ship is in perfect working condition, adequately equipped with machinery, supplies and skilled workers and is not overloaded. The insurance company will not be liable to compensate loss to the ship if the express or implied warranties are violated.

- Proximate cause: This important feature of an insurance contract looks at the ‘immediate cause’ of the event that caused the loss. For example, if a machine is insured against floods and damage is caused due to collapse of the factory building in which the machine was kept, the insurance company is not liable to compensate even if the building collapse was due to floods. The proximate cause of damage in this case was ‘building collapse’ and not ‘floods’ as specified in the contract. However, if building collapse was included as an insured peril, the insurance company would have to compensate the loss.

- Assignment and nomination: Both these aspects have been briefly discussed in the chapters on ‘Credit’. Both life and general insurance policies can be assigned as securities for loans granted to the insured. Nomination refers to the procedure by which the nominee (in whose favour the nomination is made) to receive the proceeds of the policy without cumbersome legal documents. However, if an assignment is made, the assignor (the insured) ceases to be the owner of the policy. Hence, once the purpose for which the policy has been assigned is achieved and the insured becomes the owner of the policy once again, he would have to carry out a fresh nomination procedure.

Benefits of Insurance

Insurance is an instrument of security, savings and peace of mind. By paying a small amount of premium to an insurance company, one can avail of several benefits as follows:

- Safeguard oneself and one’s family for future requirements

- Peace of mind in case of financial loss

- Encourage savings

- Get a tax rebate

- Protection from claims made by creditors

- Security against a personal loan, housing loan or other types of loan

- Provide a protection cover to industries, agriculture, women and children

Life insurance is universally acknowledged to be an institution which eliminates ‘risk’ and provides timely aid to the family in case of an unfortunate event like the death of the breadwinner. It is a contract for payment of a sum of money to the person assured (or the nominee) on the happening of the events insured against. The contract provides for the payment of premium periodically to the insurance company by the insured. The contract provides for the payment of an amount on the date of maturity or at specified dates at periodic intervals or at unfortunate death, if it occurs earlier. Some benefits of life insurance are as follows:

Protection Life insurance guarantees the full protection against risk of death of the assured. In case of death, the full sum assured is payable.

Long-Term Saving By paying a small premium in easy installments for a long period, a handsome saving can be achieved.

Liquidity A loan can be obtained against an assured policy whenever required.

Tax Relief Tax relief in income tax and wealth tax can be availed on the premium paid for life insurance.

Health insurance polices ensure guarding a holder’s health against any calamities that may cause long-term harm to his life hampering his earning ability for a lifetime. These health policies cover individuals and groups.

There are several types of health policies as given below.

- Mediclaim policy

- Personal accident–individual

- Personal accident–family n Group accident insurance

- Traffic accident policy

Types of Insurance Products

Broadly, insurance products can be classified as given in Figure 18.1.

FIGURE 18.1 BROAD CLASSES OF INSURANCE PRODUCTS

Life insurance: This is a contract between the insurance company and the insured person, whose terms specify that the insurer pay a specified amount of money at the end of the term of the policy, or in case of the death of the insured. The insured periodically pays a premium, the amount of which is determined based on the insured’s age and health. At the end of the term or on the death of the insured, whichever is earlier, the amount along with bonus is paid to the insured or his family.

As shown in Figure 18.1, there are two basic types of plans under life insurance—pure endowment and term assurance. These are considered the building blocks of life insurance, and the other plans, schemes and annuity plans of life insuring companies are variants of these basic plans. Under the pure endowment plan (and its variants), the sum assured is paid on survival of the life assured for the term of the policy. Under the term insurance plan, in contrast, the insurance sum is paid only on death of the insured during the term of the policy.

An illustrative list of general insurance products is as follows:

- Motor insurance: There are two types of motor insurance.

- Third party—which only insures the party/parties other than the owner in the case of an accident.

- Comprehensive—which insures the owner as well as the third party involved. The premium for motor vehicles is decided on the value of the vehicle and location where it is to be registered. The premium for a heavy commercial vehicle is decided on the value of the vehicle and gross laden weight.

- Property insurance: This insurance covers land, building and the contents of the building.

- Fire insurance: This is a comprehensive policy. This policy, besides covering loss on account of fire, also covers loss on account of earthquake, riots, strikes, malicious intent and floods.

- Burglary: This insurance covers all losses arising out of burglary committed in one’s premises.

- Health insurance: The holder can claim reimbursement of medical expenses.

SECTION II

INDIA’S INSURANCE SECTOR—AN OVERVIEW

The Insurance Sector

The economic growth and increase in population have made the countries, such as India and China as the most lucrative insurance markets in the world. Before 1999, Indian market was a monopoly with the state-run Life Insurance Corporation of India (LIC), the major player in life insurance sector and the General Insurance Corporation of India (GIC), with its four subsidiaries in the general sector. In the wake of the reform process and the passing of the Insurance Regulatory Development Act (IRDA) by the parliament in 1999, the Indian insurance sector was opened for private companies.

History The insurance industry has a long history. Life insurance, in its existing form, came to India from the UK in 1818. The Indian Life Insurance Companies Act of 1912, was the first measure to regulate the life insurance business. Later in 1928, the Insurance Companies Act was passed, which the government amended in 1950. On 1 September 1956, all the insurance companies were nationalized. The LIC of India was formed in September 1956, by the passing of the LIC Act by the Indian parliament in 1956.

The first general insurance company, Triton Insurance Company Ltd, was established in Calcutta in 1850. In 1957, the General Insurance Council, a wing of the Insurance Association of India, formed a code of conduct. In 1961, an insurance act was passed to form the GIC Ltd, which was amended in 1968. The general insurance business was nationalized with effect from 1 January 1973 by the General Insurance Business Act of 1972. 107 Indian and foreign insurance companies operating prior to 1973 were amalgamated and grouped into four operating companies under the GIC.

- National Insurance Company Limited

- New India Assurance Company Limited

- Oriental Insurance Company Limited

- United India Insurance Company Limited

All the above four subsidiaries of the GIC operate all over India. The GIC and its four subsidiary companies were government companies registered under the Companies Act.

The GIC as a holding company of the above four companies, super intends, controls and carries on the business of general insurance. The GIC undertakes mainly reassurance business and aviation insurance. The general insurance business of fire, marine, motor and miscellaneous is undertaken by the four subsidiaries. The general insurance industry has been growing at a rate of 17 per cent per annum.

Globalization and Liberalization The wave of globalization and liberalization is in full swing in the Indian markets. The insurance sector, being one of the most affected markets, has experienced a plethora of new relationships in the last couple of years. There are a few forces acting on the industry that have brought about significant changes in the behaviour of insurance policies.

India has become the second largest emerging market in the world. Emerging markets are characterized by low penetration and high growth.

Tables 18.1 and 18.2 provide basic information on the life and general insurance companies operating in India.

Though liberalization has led to an increase in the number of players, there is immense potential to increase insurance penetration in India. One study states that only about a quarter of India’s population has life insurance. ‘Insurance penetration’ is defined as the ratio of insurance premium to GDP, and is considered a key indicator of the spread of insurance coverage and insurance culture.

People purchase insurance for various reasons—old age security, risk coverage, tax rebate, money for child’s marriage and money for child’s education in that order with diminishing importance. In terms of insurability, the market penetration and coverage of human life value of policyholders are both less than 20 per cent. To harness the full force of Indian potential for contractual savings like insurance, the industry must learn a differential technique for rural business in areas like product development and pricing, marketing, development of sales channels, sales process, service to customers and financial management with a rural bias.

Some of the discernable trends for a healthy industry in India are a change of strategy from a technology focus to an integrated business focus, management style from a functional control to leadership based on teamwork, organization from a rigid hierarchical structure to a flexible team-based structure, performance measurement from a weak internal job orientation to a result-based business, funding from incremental induction to business value-based commitment and relationship with customer from ‘sell what can be sold’ to ‘retain the customer for life’.

Changing Scenario of the Life Insurance Sector

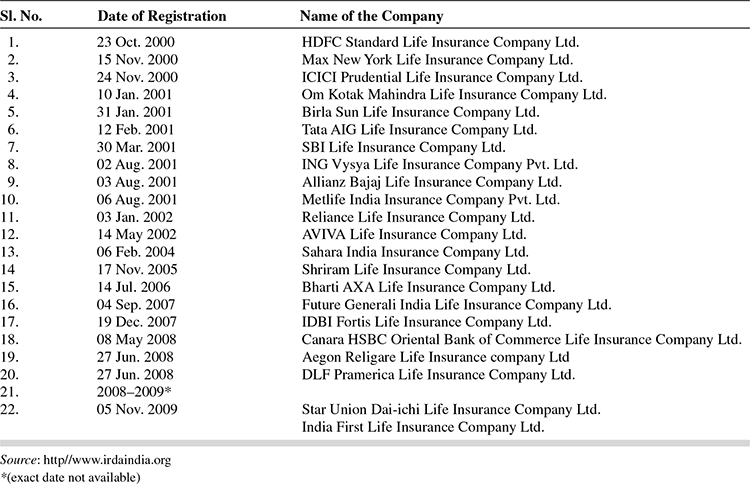

Consider the following facts. Only 22 per cent of the insurable population in India possesses life insurance. What’s more, in a country of over 1 billion people, life insurance premia forms only 1.8 per cent of the GDP, indicating the extent of underinsurance. Recognizing the huge potential in the market and the need to make insurance, particularly life insurance, available on a wider scale, the government opened the industry to private players in 1999 and was flooded with applications. Major international insurers—Prudential and Standard Life of UK, Sun Life of Canada and AIG, MetLife and New York Life of the US, to name a few, tied up with leading companies in India to reach out to this vast mass (see Table 18.3). Today, the Indian life insurance industry has many private players, each of which are making strides in raising awareness levels, introducing innovative products and increasing the penetration of life insurance in the vastly underinsured country. Several of the private insurers have introduced revamped products to meet the needs of their target customers in line with their business objectives. Some insurers, such as ICICI PruLife have fulfilled their mission to be a scale player in the mass market by introducing a slew of products to meet the need of each customer. Others have taken a more focused approach, introducing select products that they believe hold potential and fill market gaps. Whatever the case may be, each life insurer has approached the category with a fresh perspective. The success of the efforts is noteworthy—private players captured over 20 per cent of the premium income in less than 4 years since the beginning of operations, a figure that is growing each month.

Undoubtedly the biggest beneficiary of the competition amongst life insurers is the consumer. A wide range of products, customer-focused service and professional advice has become the mainstay of the industry, and the consumer forms the pivot of each company’s strategy. On the back of advertising campaigns, seminars and workshops, one can see a dramatic increase in customer awareness. Penetration of life insurance is beginning to cut across socio-economic classes and attract people who have never purchased insurance before.

Life insurance is no longer a poorly understood product that is pushed on to people. Nor is it a product that is only to be bought hurriedly at the time of filling taxes. It is now catching on as an important element of the overall financial basket; one that is purchased to fulfil specific rational and emotional needs and has clear benefits and advisors are being trained to sell insurance as a solution to meet these needs.

Life insurance is now also being regarded as a versatile financial planning tool. Research indicates that Indians have four basic financial needs during their life—asset accumulation (house, car), protecting their family, securing their children’s education and provision for their retirement. So, while there are three basic types of insurance, these have been structured with increased flexibility to meet focused requirements. Furthermore, these can be enhanced with riders to protect one against disability and provide monetary compensation at times of critical illness or surgeries. Apart from protection, life insurance policies are also ideal vehicles to save for retirement, because of their expertise in long-term fund management. By starting, say in one’s early thirties, and saving regularly through a pension plan for say, 25–30 years, a person can accumulate a large amount at the time of retirement. This can then be invested in an annuity to provide a regular income.

In addition to innovation, there are two trends that stand out on the products front. The days of high guaranteed return products, which were unsustainable, are over. Products are now priced flexibly, realistically and sustainably. What does this mean for the consumer? With greater awareness, they are in a better position to understand the benefits and are accepting new products.

Another area of vast improvement is in the service attitude and delivery. From a system that left policyholders running from pillar to post to get policy serviced, service levels are steadily rising to make the customer the focus of each initiative.

Multiple touch-points have emerged—contact centres, email, facsimile, web sites and of course snailmail—which enable the customer to get in touch with insurance companies quickly, easily and directly. In the process, response time has come down dramatically and information availability has become immediate.

As with privatization in any industry, the benefits are not restricted to the customer alone, but extend to society at large by generating employment for thousands. Over the past 2 years, insurance companies—both life and non-life—have collectively hired thousands of employees to staff their operations across the country. Most of them have been appointed as life insurance advisors who counsel and recommend products to insurance buyers. One of the most promising outcomes of this trend is that a job as an insurance advisor has become a practical career option for thousands of people who would otherwise not work—housewives, retirees, even those with just basic educational qualifications! Success levels are determined by the amount of effort one puts in, and the advantages are several—flexible hours, continuous learning and training, little or no investment, the pride of working with some of the most respected names in the financial services industry and an income stream that can continue for several years.

It is clear that the face of life insurance is changing. But with the changes, there come a host of challenges, and it is only the credible players with a long-term vision and a robust business strategy that will survive. Whatever be the developments, the future and the opportunities in the industry will surely be exciting.

Insurance Regulatory Development Authority (IRDA)

On the recommendation of the Malhotra Committee, the Insurance Regulatory Development Act (IRDA) was passed by the Indian Parliament in 1993. Its main aim was to activate an insurance regulatory apparatus essential for proper monitoring and controlling of the insurance industry. This Act helped several private companies to enter into the insurance market and some companies even joined hands with foreign partners. In this economic reform process, insurance companies could boost the socio-economic development process also. The huge amount of funds at the disposal of insurance companies could be directed towards desired avenues like housing, safe drinking water, electricity, primary education and infrastructure. The growth of the debt market also got a boost. Above all, the policyholders got better pricing of products from competitive insurance companies.

IRDA is responsible for the proper monitoring and controlling of the insurance industry. The IRDA is headed by a chairman, who is also the controller of insurance.2

IRDA, for the time being, prohibits 100 per cent foreign equity in insurance. It requires Indian promoters to invest either wholly in an insurance venture or establish a joint venture with a foreign partner. IRDA is the sole authority responsible for awarding of licenses.

IRDA Regulations

Due to the IRDA regulations, foreign players have to cultivate and develop long-term relations with potential Indian partners. The IRDA encourages domestic insurers to maintain maximum retentions commensurate with their financial strength and premium volume. Further, insurers must satisfy minimum obligations to serve specific rural and social sectors with phased operational targets. The IRDA also has tight controls and regulates rates, minimum capitalization and solvency, as well as advertisements, disclosure requirements, contract terms and conditions. Insurers must also satisfy minimum investment requirements in national government, state or approved securities (i.e., not less than 50 per cent of the total invested assets for life insurers and 30 per cent for non-life and reinsures). Minimum investment in infrastructure and social sector assets also apply (i.e., at least 15 per cent of life assets and 10 per cent for non-life and reinsures).4 The general intent is to keep as much business in the country as possible, a somewhat questionable action given the potentially substantial economic benefits of greater geographic diversifications.

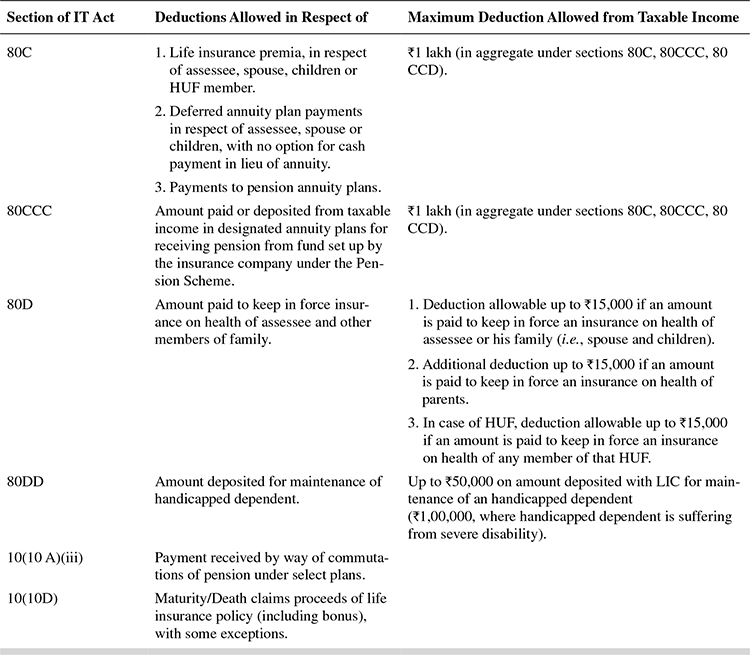

Tax Concession An investment in life insurance is not only a safety net, but also a great way to reduce tax burden. An illustrative list of income tax benefits available under various plans of life insurance is provided in Table 18.3.

TABLE 18.3 AN ILLUSTRATIVE LIST OF IT BENEFITS CURRENTLY APPLICABLE (2009–2010) IN RESPECT OF LIFE INSURANCE

Life Insurance Corporation of India

Life Insurance Corporation of India (LIC) was formed in September 1956 by the Government of India. Its main duty was to spread the message of life insurance in the country and mobilize people to save for nation-building activities.

Over time, LIC became very popular in India. The central office of LIC is in Mumbai and it has seven zonal offices located at Mumbai, Delhi, Kolkata, Chennai, Hyderabad, Kanpur and Bhopal. There are over 100 divisional offices and 3,000 plus branch offices. There are more than half a million active agents of LIC. It also has offices in different countries for business transactions. LIC has entered into joint ventures abroad with several companies in the field of insurance.

LIC has a variety of insurance plans which helps all categories of people and their diverse needs. The funds generated through the premium of policyholders are divested to a number of socio-economic projects in the country. The LIC insurance plan is categorized as individual insurance plan, group insurance schemes, pension plans and capital market linked plans.

LIC Plans for Individuals The important insurance plans offered by the LIC are as follows:

- Whole life schemes

- Endowment schemes

- Term assurance plan

- Periodic money back plans

- Plan for high-worth individuals and key men

- Medical benefits linked insurance

- Plans for the benefit of the handicapped

- Joint life plan

- Plans for children’s needs

- Investment plans

Export Credit Guarantee Corporation of India (ECGC)

The Export Credit Guarantee Corporation of India, the fifth largest credit insurer of the world was established in 1957 by the Government of India. Its main purpose is to cover the risk of companies on export credit. It is managed by a board of directors comprising representatives of the government, the Reserve Bank of India, the banking sector and insurance and exporting firms.

Major Functions The major functions of ECGC can be discussed as under.

- To provide a range of credit risk insurance, which covers exporters against loss in export of goods and services.

- To offer guarantees to banks and financial institutions to enable exporters obtain better facilities from them.

- ECGC also help exports by providing insurance protection to export-related activities, guidance in exportrelated activities, information on credit-worthiness of overseas buyers and information on about 180 countries with its own credit ratings, making it easy to obtain export finance from banks/financial institutions.

- Assisting exporters in recovering bad debts.

Policies issued by the ECGC can be divided into the following categories:

- Standard policy: Shipments (comprehensive risks) policy, which is commonly known as the standard policy, is the one ideally suited to cover risks in respect of goods exported on short-term credit, i.e., credit not exceeding 180 days. The policy covers both commercial and political risks from the date of shipment.

- Specific policies: Specific policies are designed to protect Indian firms against payment risks involved in exports on deferred terms of payment, including services rendered to foreign parties and construction works and turnkey projects undertaken abroad.

- Financial guarantees: Financial guarantees are issued to banks to protect them from risks of loss involved in their extending financial support at pre-shipment and post-shipment stages. These cover a host of non-fund based facilities that are extended to exporters.

- Some special schemes: Transfer guarantee is meant to protect banks that add confirmation of letters of credit opened by the foreign banks.

- Insurance cover for buyers’ credit

- Exchange fluctuation risk insurance

Overseas Investment Risk Insurance The ECGC has evolved a scheme to provide protection for Indian investments abroad. Any investments made by way of equity capital or untied loan for the purpose of setting up or expansion of overseas projects will be eligible for cover under investment insurance. The investments may be either in cash or in the form of export of Indian capital goods and services. The cover will be available for the original investment together with annual dividends or interest receivable.

SECTION III

BANKS AND INSURANCE SERVICES—BANCASSURANCE IN INDIA

Gradually all over the world, the separation of commercial banking activities from other financial services is blurring. In many countries, where such compartmentalization did exist, the barriers are being broken down through appropriate legislation and regulation. Financial liberalization and innovation have brought the worlds of banking and insurance closer.

Bancassurance refers to selling insurance products through banks’ established distribution channels. Given India’s size, its low insurance penetration, low insurance density and a very large bank branch network, it was only natural that banks entered the insurance business—since insurance is a financial product required by all banking customers.

The term ‘bancassurance’ stems from French origins (banc + assurance). In France, traditionally, a large part of insurance selling is being done by banks, and the term first appeared in 1980. Banks selling insurance products became common in other European countries too. Even in the United States, where there was a strict division between banking and non-banking activities, there is increased preference—post the Gramm-Leach-Blailey Act 1999—for banks dealing in non-banking financial products, especially insurance products. Several Asian countries too have adopted the ‘financial supermarket’ theme.

Following the Malhotra Committee recommendations,1 the Government of India specified in August 2000 that ‘Insurance’ is a permissible form of business that could be undertaken by banks under Section 6(1)(o) of the Banking Regulation Act, 1949. Subsequently, the RBI issued the guidelines on banks conducting insurance business.

How Does Bancassurance Help Banks?

Bancassurance helps banks in the following ways:

- Banks are experiencing narrowing ‘spreads’ or ‘net interest margins (NIM)’ due to increasing competition. Hence, banks are being forced to look for alternate sources of income in the nature of ‘fee based income’ (Also see the chapter ‘Sources of Bank funds’).

- Such fee-based income should be stable and free of default risk. Bancassurance promises enhancement in earnings without the problem of NPAs. (See chapter ‘Managing credit risk’ for more on NPAs).

- Bancassurance requires little or no investment in additional infrastructure.

- Banks can take advantage of the low insurance penetration and density (both terms were defined earlier in this chapter), as well as their very large branch network to generate substantial income.

- Banks have the advantage of customer interface even in the age of automation. This is an advantage to enable banks understand customers’ specific needs and design and market insurance and other financial products accordingly.

- Studies have revealed that adding life insurance activities to banking operations enabled banks not only to diversify their earnings but also increase assets under management substantially.

How Does Bancassurance Help Insurance Companies?

Bankassurance helps insurance companies in the following ways:

- Competition increased manifold with a number of foreign insurance companies in both life and non-life segments entering India through joint ventures. The huge market potential could be tapped only by increasing the distribution channels from the traditional ‘agency’ model.

- Insurers, especially those who were not subsidiaries to large commercial banks (e.g., SBI Life, HDFC Chubb or ICICI Prudential), and those in the private sector, benefitted through collaborative arrangements with specific banks to reach a huge client base.

- In a study, Swiss Re noted that Greenfield start up operations would be easier without the need to recruit and train a large number of insurance agents. At best, insurance companies need to train existing frontline bank staff. Insurer’s own agents could also act upon the client database obtained from banks. Thus, insurance companies can realize better earnings through cost effective operations and increased revenues.

- The proximity of bank staff to customers would help in understanding customer needs, which would lead to timely innovations or improvement in existing products to ensure better risk management.

- IRDA regulations require that a certain proportion of insurance revenues2 should flow from the rural and social sector. Banks, with their extensive rural reach, would help achieve this objective, cost effectively.

How Does Bancassurance Help Customers?

Bancassurance helps customers in the following ways:

- We have seen that insurance rests on the ‘uberrimae fidae’ pillar. For a long time, customers have built longterm trust and relationship with the public sector insurance companies, such as the LIC. With several new private sector insurance players, many of them with foreign collaborations entering the fray, the customer is confused about their trustworthiness. Bancassurance can bring in trust, since customers have long standing relationships with banks who are selling the insurance provided by the new players.

- Customers can now enjoy almost all types of financial services at a single window provided by the banks.

- The single window financial supermarket concept relieves customers from having to scout for good deals for various financial products.

- Even if they do get good deals, many customers may not have sufficient expertise to evaluate the deal or product. The financial supermarket concept lends comfort to customers since the bank recommends the product.

- The ‘one stop shop’ for the customer’s financial needs could also lead to cost effective products for customers; for example, a reduced premium rate due to economies of scope, as well as expert financial counselling.

- Banks take the role of financial advisors to the customer, since the relationship between the insurer and the insured is different from the relationship between the banker and the customer. Since customers trust banks due to their long standing relationship, the bankers’ advice could be a source of reassurance to the customers.

Let us look at the typical models of bancassurance.

- The referral model: This is the path of least risk for banks. They merely part with their client database for a commission. The client contact and deal closing is carried out by the insurance company or its agents.

- The corporate agency model: Here, the bank assumes the role of an ‘agent’. As a ‘corporate agency’, the bank trains its staff to assess customer needs for insurance and sell products. Understandably, the commission earned by the bank will be higher than for the referral model. However, the issues that could arise with this model can be easily foreseen—the bank may run a reputation risk if its staff does not provide appropriate advice,3 or specially trained staff would be required to handle the business, or the chosen employees may resist the change in their portfolio. However, many believe that this model can be made to work with proper training and incentives.

- The fully integrated financial service model: Recall the concept of the ‘operating subsidiary’ model from Chapter 1 (Managing Banking and Financial Services—Current Issues and Future Challenges), as one of the alternative models for a financial conglomerate. In this case, insurance business is just one more line of business for the bank. This includes banks having fully owned insurance subsidiaries, with or without private/ foreign participation. Indian banks, such as the SBI, ICICI Bank and HDFC Bank have already established and are successfully operating this model. For relatively large banks like these, this model could yield the benefits of synergy and economies of scope. International experience also finds that such fully integrated bancassurance performs better than other models.

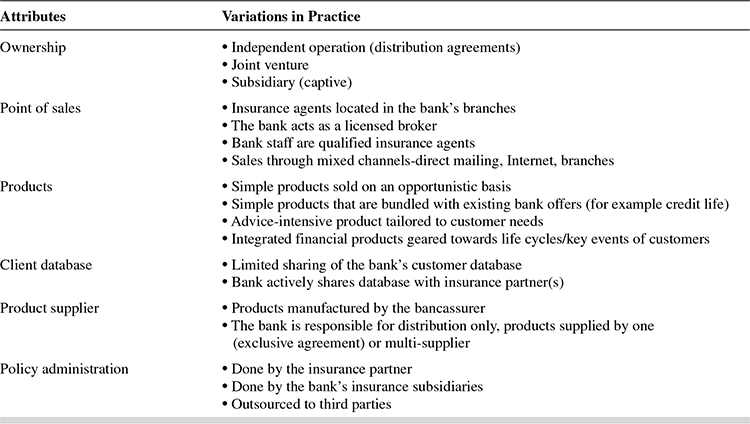

Both the referral and corporate agency models are in vogue in India. The current regulations stipulate that banks can opt to become either referral providers or corporate agents, but they are permitted to do so only for one life and one non-life insurance company in India. Variants of these practices can be found in various parts of the world, as shown in Table 18.4.

TABLE 18.4 ILLUSTRATIVE PRACTICES ADOPTED BY VARIOUS COUNTRIES FOR BANCASSURANCE

SECTION IV

GLOBAL INSURANCE INDUSTRY, OPPORTUNITIES AND CHALLENGES

The Industry After the financial Crisis4

The performance of the insurance sector since 2007 has been largely influenced by the sub-prime crisis that originated in the United States, and later engulfed most of the major world economies. However, except for a few major insurance companies, most insurance companies were not affected. Nevertheless, for the first time since 1980, insurance premiums declined in real terms. Life premiums appeared to be impacted more by a fall of about 3.5 per cent, while non-life premiums fell by 0.8 per cent. Profitability of insurance companies were further eroded due to losses on investments in volatile capital markets and higher cost of guarantees as well as lower revenues from management fees.

The United States of America accounts for 35 per cent of the global life and non-life insurance premiums. This reflects the concentration of wealth and high risk-awareness in that market. Japan has a global share of 21 per cent, mainly due to the public’s strong reliance on life insurance products as an investment vehicle. The UK contributes to about 10 per cent of the world’s total premium. Together, the three markets account for 66 per cent of world insurance premiums. It is worth noting that insurance industry too has its plate full of miseries. Non-life insurance companies suffered more than the life insurance ones. They were called upon to bear the loss due to the terrorist attacks; reinsurance companies had also doled out billions of dollars taking a severe hit in the process.

Challenges

There is tremendous potential for growth in the insurance industry because of the diversity and depth of the market. Amidst challenges of liberalization, intense competition and convergence of financial institutions, global insurers have called for greater cooperation among themselves and with the regulators. The life market is coping with challenges of new regulations, widened competition from banks and pressure to expand distribution channels. In recent years, insurers have expanded the frontier of insurability to include previous unfamiliar areas like political, gene and financial risk and would necessarily face greater challenges than before. In general, the key challenges are as follows:

Catastrophes Natural catastrophes include storms, floods and earthquakes. In recent years, the magnitude of catastrophic property—casualty disaster has become a major topic of debate. An approach based on traditional insurance according to the solidarity principle is better for all concerned and is feasible from an underwriting point of view.

Opportunities

Both life and non-life insurers see real challenges and opportunities in the market. Non-life insurers welcome the hardening cycle as a forcing factor to the industry to return to prudent underwriting basics, while life insurers feel there is greater scope for players with stress on financial planning, retirement planning, asset management and healthcare insurance. The key strength of the market is a strong consumer demand for insurance products, which is expected to continue for a long time.

Convergence

One conception of convergence is that the lines between banking, finance and insurance are increasingly blurred. For example, bancassurance, the provision of insurance products through banks, has developed into a major insurance distribution channel in Europe, where regulatory barriers are less restrictive than in other markets. Life products are more easily sold through banks than non-life products. The growth of bancassurance reflects several broad industry trends, including growing competition, a desire to expand existing distribution networks through cross-selling, a bank’s desire for diversification, financial deregulation and the pursuit of cost efficiencies.

The Growth of Insurance Demand

Globally, insurers are increasingly pressured by the demands of their clients. The development of the global insurance industry over the past few years was considerably influenced by the booming stock markets, which enabled considerable capital gains to be made in the non-life business. This strengthening of insurers’ equity capital increased underwriting capacity, while demand did not develop at the same pace, resulting in a dramatic fall in insurance prices. The stock market boom of the past few years led to a soaring demand for unit-linked insurance products in life business.

CHAPTER SUMMARY

The key areas for the IRDA for developing the emerging Indian insurance market are given below.

- In this world of continuous relationship marketing, the regulator has to strive to establish deep and direct linkages between the insurance companies and the policyholders in order to build a sustainable market.

- Achieving rapid sustainable growth requires that companies manage three horizons simultaneously, which are: growing current business, expanding into related businesses and seeding options for future growth.

- Delivering high-quality products, given the state of India’s fragmented retail trade and extreme weather conditions, is often viewed as a challenge. To ensure growth of the insurance business, the regulator has to develop innovative business systems.

- Insurance would assist businesses to operate with less volatility and risk of failure and provide for greater financial and societal stability.

- The government has arranged for disaster management funds. NGOs and public institutions assist with fund raising and relief assistance. Besides, government provides for social security programs. Insurance substantially steps in to provide these services. The effect would be to reduce the strain on the taxpayer and assist in efficient allocation of societal resources.

- Insurance firms facilitate trade, business and commerce by flexible adaptation to changing risk needs particularly of the burgeoning services sector.

- Like any other financial institution, insurance companies generate savings from the insurance sector within the economy and make available the same in well-directed areas of the economy deserving investments.

- It enables risk to be managed more efficiently through risk pricing and risk transfers and this is an area which provides unlimited opportunities in the Indian context for consulting and education in the post-privatization phase with newer employment opportunities.

- The insurance firm’s functions are based on the theory of ‘loss minimization’. The expertise in understanding losses would enable better loss control.

TEST YOUR UNDERSTANDING

- Which of the following is not a general insurance product?

- Motor insurance

- Life insurance

- Fire insurance

- Property insurance

- Health insurance

- Which organization/agency gives a license to new private players?

- GIC

- IRDA

- SEBI

- ECGC

- None of these

- Name three new players in the insurance sector in India.

- Name three firms offering services in the general insurance segment in India.

TOPICS FOR FURTHER DISCUSSION

- Why did the government privatize the insurance sector?

- Do you think that the new players would survive in the insurance industry?

- Do you agree with the idea of tax rebate for investment in insurance products?

SELECT REFERENCES

- Khan, M. Y. (1997). Financial Services, 2nd ed. Chapter New Delhi: Tata McGraw-Hill.

- Ray, Alok (2001). Pros and Cons of Insurance Liberalisation, in K. Seethapathi (ed.) ‘Financial Services: Emerging Trends, Chapter 22. Hyderabad: ICFAI Publication.

- Bhusnurmath, Mythili (2001). ‘Insurance Sector Reforms’, in K. Seethapathi (ed.), Financial Services, Chapter 23. Hyderabad: ICFAI Publication.

- Karunagaran, A.,(2006), “Bancassurance: A feasible strategy for banks in India”, Reserve Bank of India Occasional Papers, Vol. 27, No. 3, Winter 2006, accessed at http//www.rbi.org.in

- Report of the committee on IRDA distribution channels, (2008), accessed at http//www.irda.gov.in

ENDNOTES

- In 1993, the Government set up a committee under the chairmanship of R. N. Malhotra, former Governor of the RBI, to propose recommendations for reforms in the insurance sector. The objective was to complement the reforms initiated in the financial sector. The committee submitted its report in 1994 wherein, among other things, it recommended that the private sector be permitted to enter the insurance industry.

- IRDA notification dated 16.10.2002 and amendments can be accessed at http//www.irda.gov.in

- IRDA annual report 2008–2009 provides information on major types of grievances/complaints against insurance companies, and the most prevalent complaint relates to ‘wrong plan and term allotted’.(page 50, Table 53), accessed at http//www.irda.gov.in

- IRDA annual report, 2008–2009, accessed at http//www.irdaindia.org