CHAPTER EIGHT

Managing Credit Risk—An Overview

CHAPTER STRUCTURE

Section II Measuring Credit Risk—Introduction to Some Popular Credit Risk Models

Section III Credit Risk Transfers – Securitization, Loan Sales, Covered Bonds and Credit Derivatives

Section V Treatment of Credit Risk in India—Securitization and Credit Derivatives

Annexures I, II, III (Case Study)

KEY TAKEAWAYS FROM THE CHAPTER

- Understand the concept of credit risk.

- Know how credit risk arises.

- Learn about credit risk mitigation techniques, such as securitization, covered bonds and credit derivatives.

- Understand the Basel Committee’s role in credit risk management.

- Gain knowledge about the prudential norms for asset classification, income recognition and provisioning.

SECTION I

BASIC CONCEPTS

Banks grant credit to produce profits. In the process, they also assume and accept risks. In evaluating risk, banks should assess the likely downside scenarios and their possible impact on the borrowers and their debt servicing capacity.

Two types of losses are possible in respect of any borrower or borrower class—expected losses (EL) and unexpected losses (UL). EL can be budgeted for, and provisions held to offset their adverse effects on the bank’s balance sheet. EL could arise from the risks in the industry in which the borrower operates, the business risks associated with the borrower firm, its track record of payments and future potential to generate cash flows. UL, being unpredictable, have to be cushioned by holding adequate capital. In this chapter, we will concentrate on the process by which banks identify and provide for EL.1

Banks can utilize the structure of the borrowers’ transactions, collateral and guarantees to mitigate identified and inherent risks, but none of these can substitute for comprehensive assessment of borrowers’ repayment capacity or compensate for inadequate information or monitoring. Any action of credit enforcement (recalling the advances made or instituting foreclosure proceedings, including legal proceedings) may only serve to erode the already thin profit margins on the transactions.

Expected Versus Unexpected Loss

Although credit losses are typically dependent on time and economic conditions, it is theoretically possible to arrive at a statistically measured long run average loss level. Assume, for example, that based on historical performance, a bank expects around 1 per cent of its loans to default every year, with an average recovery rate of 50 per cent. In that case, the bank’s EL for a credit portfolio of ₹1,000 crores is ₹5 crores (i.e., ₹1,000 crores 3 1 per cent 3 50 per cent). EL is, therefore, seen to be based on three parameters:

- The likelihood that default will take place over a specified time horizon (probability of default or PD).2

- The amount owed by the counter party at the moment of default (exposure at default or EAD).

- The fraction of the exposure and net of any recoveries, which will be lost following a default event (loss given default or LGD).3

Since PD is normally specified on a 1 year basis, the product of these three factors is the 1 year EL.

EL can be aggregated at the level of individual loans or the entire credit portfolio. It is also both customer- and facility-specific, since two different loans to the same customer can have very different ELs due to differences in EAD and/or LGD.

It is important to note that EL (and credit quality) does not by itself constitute risk—if losses turned out as expected, they represent the anticipated ‘cost’ of being in business. In any case, their impact is being factored into loan pricing4 and provisions. Credit risk, in fact, emerges from adverse variations in the actual loss levels, which give rise to the so-called UL. As described in a later chapter, the need for bank capital arises from the need to cushion against UL or loss volatility. Statistically, UL is simply the standard deviation of EL as shown in Figure 8.1.5

FIGURE 8.1 EXPECTED AND UNEXPECTED LOSSES

Defining Credit Risk6

Credit risk is most simply defined as the probability that a bank borrower or counter party will fail to meet its obligations in accordance with agreed terms.

The effective management of credit risk is a critical component of a comprehensive approach to risk management and essential to the long-term success of any banking organization. The goal of credit risk management should be maximizing a bank’s risk-adjusted rate of return by maintaining credit risk exposure within acceptable parameters.

It follows that a bank needs to manage the following:

- The risk in individual credits or transactions (discussed extensively in the foregoing chapters).

- The credit risk inherent in the entire portfolio.

- The relationships between credit risk and other risks.

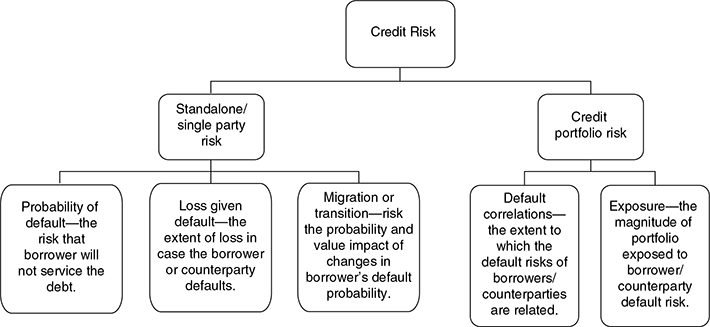

The elements of credit risk can, therefore, be grouped in the following manner7 (see Figure 8.2):

FIGURE 8.2 ELEMENTS OF CREDIT RISK7

We will discuss these aspects in the ensuing paragraphs and in the next chapter.

Credit Risk of the Portfolio From our earlier discussions, it would be evident that managing the credit portfolio of a bank involves a higher level of risk-reward decisions than managing a portfolio of market investments. This is due to the fact that there is limited upside risk and unlimited downside risk in bank lending (in contrast to market investments, which hold limited downside risk, but unlimited upside risk).

For example, when a bank makes a ‘good’ loan that is repaid in full on the due date, what the bank has received are only the interest payments and principal repayments due to it. The bank cannot demand a share of the substantial cash flows that the business has managed to generate with the help of bank funds. On the other hand, if the business fails, the bank’s earnings take a direct hit—the bank suffers along with the borrower. The bank could price ‘risky’ borrowers higher to compensate for the risk of failure.8 But market dynamics would limit the extent of the risk premium that the bank can charge.

Often, a bank develops expertise in financing a particular activity or industry and increases its credit exposure to this sector to leverage its capabilities. If this sector collapses, for some force majeure reason, it drags the bank’s fortunes down with it.

Thus, it is evident that a bank could be vulnerable to two factors—one, it may not be able to price its loan to compensate fully for the risk and two, its concentration in a specific industry or economic activity could render the bank susceptible to risks inherent in that industry.

It follows that the loan policy of a bank should be able to structure policies and procedures that ensure that credit exposures to various sectors and regions are adequately diversified to maximise the return on the loan portfolio of the bank. Such a task is too daunting for individual banks’ portfolio managers and requires the intervention of the central banks of the countries. In most countries, central banks propose optimal ‘exposure norms’ for various industries and activities from time to time. Such exposure norms not only pre-empt banks intending to invest excessively in similar firms, but also try to balance the risk-reward relationship for banks in the country.

The Relationship Between Credit and Other Risks While loans are the largest source of credit risk and exposure to credit risk continues to be a leading source of problems, there are other sources of credit risk throughout the activities of a bank, in the banking and trading books and on and off its balance sheet. For example, a bank could face credit (or counter party default) risk in various financial instruments other than loans, such as in: (a) acceptances, (b) inter-bank transactions, (c) trade financing, (d) foreign exchange transactions, (e) financial futures, swaps, bonds, equities, options, and (f) in the extension of commitments and guarantees and the settlement of transactions.9

International guidelines and standards for Credit Risk management – The Basel Committee on Banking Supervision (BCBS)

The BCBS and its key role in financial regulation have been described in detail in the chapter titled “Capital – Risk, Regulation and Adequacy”.

Annexure I presents a summary of the sound practices, standards and guidelines related to credit risk management published by the BCBS. Three such documents are noteworthy, which are:

- Principles for the Management of credit risk, published in September 2000, (http://www.bis.org/publ/bcbs75.pdf), establishes sound practices to specifically address key areas in credit risk management.

- Supervisory framework for measuring and controlling large exposures , published in April 2014, (http://www.bis.org/publ/bcbs283.pdf), sets standards to complement the risk based capital norms (which is described in detail in the chapter titled “Capital – Risk, Regulation and Adequacy”.

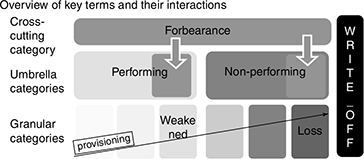

- The Guidelines for Prudential treatment of problem assets – definitions of non performing assets and forbearance, published in April 2017, (http://www.bis.org/bcbs/publ/d403.pdf) has developed guidelines for the definitions and operative features for two important terms – “non-performing exposures” and “forbearance”.

The above three documents are intended to contribute to increased stability of the financial system, especially after the experiences of the global financial crisis of 2007-08.

Classifying ‘Impaired’ Loans

International accounting practices set forth standards for estimating the impairment of a loan for general financial reporting purposes. Regulators are expected to follow these standards ‘to the letter’ for determining the provisions and allowances for loan losses. According to these standards, a loan is ‘impaired’ when, based on current information and events, it is probable that the creditor will be unable to collect all amounts (interest and principal) due in line with the terms of the loan agreement. Such assets are also called ‘criticized’ assets.

Typically, the impaired assets are categorized as follows:

- Special mentioned loans: These loans are assessed as ‘inherently weak’. The credit risks may be minor, but may involve ‘unwarranted risk’. Such credits contain weaknesses, such as an inadequate loan agreement or poor condition of or control over collateral or deficient loan documentation or evidence of imprudent lending practices. Adverse market conditions in future may unfavourably impact the operations or the financials of the borrower firm, but may not endanger liquidation of assets held as security. The special mentioned loans carry more than normal risks which, had they been present when the credit was appraised, would have led to rejection of the credit request.

- Sub-standard assets: These assets are seen to have well-defined weaknesses that may jeopardize liquidation of the debt, since they are not fully protected by the borrower’s financial condition or the collateral given as security. The bank is likely to sustain a loss if the defects are not corrected.

- Doubtful assets: These assets contain all the weaknesses of a sub-standard asset and, additionally, recovery of the debt in full is quite remote. Auditors may insist on a write down of the asset through a charge to loan loss reserves or a write off of a portion of the asset or they may call for additional capital allocation. Any portion of the balance outstanding in the loan, which is uncovered by the market value of the collateral, may be identified as uncollectible and written off.

- Loss assets: All identified losses have to be charged off. Uncollectible loans with such little value that their continuance as bankable assets is not warranted are generally charged off. Losses are expensed in the same period in which they are written off.

- Partially charged off loans: Though credit exposures contain weaknesses that render them uncollectible in full, some portion of the outstanding loan could be collected if the collateral is marketable and in good condition. Hence, the secured portion is not written off, while the unsecured portion of the loan is charged off.

- Income accrual on impaired loans is discontinued from the time they are classified.

Annexure I summarises the key guidelines from Basel Committee in defining non performing assets and forbearance. Select international practices in classifying impaired loans is shown in Table 8.1.

TABLE 8.1 CLASSIFYING IMPAIRED LOANS- PRACTICES IN SELECT COUNTRIES

Loan Workouts and Going to Court for Recovery

The workout function has been discussed in detail in the previous chapter. In the case of a restructured loan, the ability of the borrower to repay the loan on modified terms is focused upon. The loan will be classified under the ‘impaired’ category if, even after restructuring, there arise weaknesses that tend to jeopardize repayment on the modified terms.

In some developed countries like the US, regulatory rules do not require that banks restructuring a loan grant excessive concessions to the borrower during the period of restructuring.10

If all other forms of renegotiation between the bank and the borrower fail, the bank approaches the court to enforce recovery of dues. In some cases, ‘Debtor-in-Possession’ (DIP) financing is also done while the suit against the borrower is pending at the court. DIP financing is considered attractive by banks where such provision exists, since it is done only under the order of the court, which is empowered to give a priority position on the bankruptcy estate to the lender. Some alternatives for DIP financing include receivables backed credit, factoring and loans against equipment or inventory. The DIP loan is repaid from the following sources:

- cash flows from operations,

- liquidation of the collateral,

- the firm turns viable and the new lender refinances the DIP loan, and

- the DIP loan is taken over by a new DIP lender.

Credit Risk Models

Ever since Markowitz developed his pioneering Portfolio Analysis Model in 1950, quantitative models of portfolio management have been widely used in financial analysis, especially in analysis of equity portfolios. Over the last few decades, equity analysts have been successfully using portfolio management models to quantify default risks in a portfolio of assets. The objective of these methods is to maximize the portfolio’s returns while reining in risk within acceptable levels.11 This maximization involves balancing of risks and returns within a portfolio, asset by asset and group of assets by group of assets.12

However, similar models are not widely used for debt portfolios because of the greater analytical and empirical difficulties involved.

- Debt defaults can happen all of a sudden and once they happen, the risk can increase very quickly.

- We have seen the risk premium associated with the borrower or borrower class is inbuilt into the loan pricing. If the borrower risk has been misjudged, the loan would not be priced appropriately, implying further erosion in the bank’s already thin margins on lending.

- It is also pertinent to remember here that the lenders—the banks—themselves are highly leveraged entities. History is replete with instances where lenders have been destroyed by the combination of financial and default risks.

The truth is that ‘risk’ cannot be wished away, insured away, hedged away or structured away. Risk can merely be allocated or transferred, but ultimately the risk has to be borne by somebody. Hence, lenders try to diversify their credit risks, for they know that they cannot do business if they eliminate risks altogether. How can lenders diversify their risk? By avoiding ‘concentration’ of credit.

The Basel Committee13 has identified ‘credit concentrations’ as the single most important cause of major credit problems. Credit concentrations are viewed as any exposure where the potential losses are large relative to the bank’s capital, its total assets or where adequate measures exist and the bank’s overall risk level. Concentrations of credit and, hence, risk can occur when the bank’s portfolio contains a high level of direct or indirect credit to: (a) a single borrower, (b) a group of associated borrowers, (c) a specific industry or economic activity, (d) a geographic region, (e) a specific country or a group of inter-related countries, (f) a type of credit facility, or (g) a specific type of security. Sometimes, concentrations can also arise from credits with similar maturities or from inter-linkages within the portfolio. Annexure I gives a synopsis of Basel Committee’s standards in relation to credit concentration risk.

Relatively large losses14 may reflect not only large exposures, but also the potential for unusually high percentage losses given default.

Credit concentrations can further be grouped into two broad categories.15

- Conventional credit concentrations would include concentrations of credits to single borrowers or counter parties, a group of connected counter parties and sectors or industries, such as commercial real estate and oil and gas.

- Concentrations based on common or co-related risk factors reflect subtler or more situation-specific factors and often can only be uncovered through analysis, such as correlations between market and credit risks and their correlation with liquidity risk. Such interplay of risks can produce substantial losses.

Why do banks permit concentrations in their credit portfolios? The Basel Committee cites the following reasons:16 ‘First, in developing their business strategy, most banks face an inherent trade-off between choosing to specialize in a few key areas with the goal of achieving a market leadership position and diversifying their income streams, especially when they are engaged in some volatile market segments. This trade-off has been exacerbated by intensified competition among banks and non-banks alike for traditional banking activities, such as providing credit to investment grade corporations. Concentrations appear most frequently to arise because banks identify ‘hot’ and rapidly growing industries and use overly optimistic assumptions about an industry’s future prospects, especially asset appreciation and the potential to earn above-average fees and/or spreads. Banks seem most susceptible to overlooking the dangers in such situations when they are focused on asset growth or market share’.

Until recently, such ‘concentrations’ could be measured only after the credit exposures had been created. Of late, finance literature has produced a variety of models that attempt to measure default risk.

While most of the methodologies are seen to work adequately in practice, research indicates that some issues are still not tackled by the models in respect of bank lending such as predicting macro-economic cycles and industry shocks (systematic or exogenous default risk) and hedging strategies.

SECTION II

MEASURING CREDIT RISK—INTRODUCTION TO SOME POPULAR CREDIT RISK MODELS

A Basic Model

A simple method of estimating credit risk is to assess the impact of non-performing asset (NPA) write offs on the bank’s profits. This can be achieved through dividing the ‘profit before taxes’ (PBT) by the NPAs. Here, PBT is more relevant since losses written-off typically enjoy tax shields.

Another method of presenting this concept is to work from the net income of the bank and treat both the net income and the NPAs as a proportion of average total assets of the bank.

Accordingly, this simple measure of credit risk can be presented in the following forms:

- PBT/TA

------------

NPA/TA

or

- (PAT/[1 – t])/TA

--------------------

NPA/TA

or simply,

- PBT/NPA

Interpretation of the result

If the above measure yields a result of say, 0.7, it simply means that if 70 per cent of the NPAs turn into ‘loss assets’ and are written off, the bank’s PBT would be eroded completely. For this reason, the resultant proportion is also called the ‘margin of safety’.

TEASE THE CONCEPT

Which is safer for the bank—the above measure being lower or higher?

Modeling Credit Risk

Financial institutions have traditionally attempted to minimize the incidence of credit risk primarily through a loan-by-loan analysis. The foundations of a more analytical framework began in the early 1960s when the first ‘credit scoring’ models were built to assist credit decisions for consumer loans. The lending institutions initially classified debtors/counter parties on default potential based only on an ordinal ranking. By the mid-1980s, particularly with the introduction of RAROC as a performance measure, many financial institutions began calibrating each credit score to a particular PD17 to estimate expected losses (EL) and ultimately economic capital.

Techniques to calculate PD can be divided into two broad categories.

- Empirical: These models use historical default rates associated with each ‘score’ to identify the characteristics of defaulting counter parties. Traditionally, such models used discriminant analysis (such as Z scores), but more recently logit or probit regressions are being used to define the score ‘S’18

- Market-based (also known as structural or reduced-form) models: These models use counter party market data (e.g., bond or credit default swap (CDS) spreads and volatility of equity market value) to infer the likelihood of default.

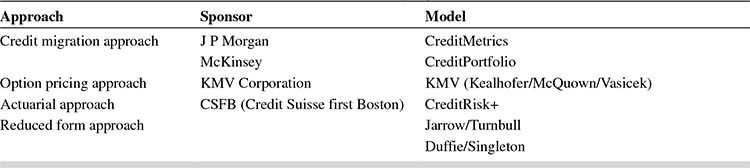

Several commercial credit value-at-risk models have been developed in the last 10–15 years (e.g., Credit Metrics, KMV and Credit Risk+) that use credit risk inputs (credit data, market data, obligor data and issue/facility data) to derive a loss distribution, by assuming that correlations across borrowers arise due to common dependence on a set of ‘systematic risk factors’ (typically, variables representing the state of the economy). Sophisticated banks generally use these models for active portfolio-level credit management (particularly, for large corporate loans) by identifying risk concentrations and opportunities for diversification through debt instruments and credit derivatives.

Table 8.2 classifies popular models according to the approach adopted by them.

TABLE 8.219 INDUSTRY-SPONSORED CREDIT VALUE-AT-RISK (VaR) MODELS

Table 8.3 compares these approaches on various parameters.

TABLE 8.320 COMPARIS ON OF CREDIT RISK MODELS ON VARIOUS PARAMETERS

In addition, several academic models have been developed, which can be categorized into two. The models in the first category adopt an exogenous default-trigger value of assets. In contrast, the models in the second category derive the decision to default endogenously, as part of the borrower’s internal problems and are, therefore, a function of borrower characteristics.21

A description of the approaches to credit risk measurement and the popular models can be found in the next chapter.

SECTION III

CREDIT RISK TRANSfERS—SECURITIZATION, LOAN SALES, COVERED BONDS AND CREDIT DERIVATIVES

Hedging reduces portfolio risk by offsetting one risk against another. Diversification reduces risk because risks are uncorrelated. How portfolio hedges are structured will vary according to the bank’s goals on hedging credit risk.

Till even about a decade ago, banks had to expand their loan portfolios for growing their business and keep these assets in their books till they were completely liquidated. In the present scenario, banks still grow their business by expanding loan assets, but these assets are sold off to other agencies or of floaded in the secondary loan market. In this manner, banks get risky loans off their books. Such loan sales provide liquidity to the selling banks and also represent a valuable portfolio management tool, which minimizes risk through diversification.

Some prominent forms of loan sales include the following.

- Syndication: We have seen this as a form of credit in Chapter 5. The manner in which syndication is conducted spreads the credit risk in the transaction among the banks in the syndicate. Let us assume a borrower wants a loan of ₹10,000 crores for a large project. If Bank X is nominated as the lead bank for the syndication, X will negotiate the documents with the borrower and solicit a group of banks to share the credit exposure. X will generally hold the maximum exposure, though this is not mandatory. Bank X claims a fee for its efforts in syndication.

- Novation: In the above example, Bank X assigns its rights to one or more buyer banks. These buyer banks then become original signatories to the loan agreement. Thus, the borrower would have contracted with Bank X for the ₹10,000 crores loan. Post novation, Bank X would hold, say, ₹2,000 crores of credit exposure to the borrower and the three buyer banks, say A, B and C, would hold the remaining ₹8,000 crores share among themselves in a mutually agreed proportion. Unlike syndication, A, B and C would enter into separate loan agreements with the borrower.

- Participation: In this case, Bank X transfers to other participating banks A, B and C the right to receive pro rata payments from the borrower. Typically, the seller of the participation—Bank X—will have to consult A, B and C before agreeing to changes in the terms of the loan (principal, interest, repayment terms, guarantees, collaterals, interest rate, fees and other covenants).

SECURITIZATION

This is one of the most popular and prominent forms of loan sale. The critical factor is finding a homogeneous pool of loan assets that generate a predictable stream of future cash flows.

Simply stated, securitization involves the transfer of assets and other credit exposures from the ‘originator’ (the bank) through pooling and re-packaging by a special purpose vehicle (SPV) into securities that can be sold to investors. It involves legally isolating the underlying exposures from the originating bank. A ‘true sale’ or ‘traditional securitization’ happens where the assets are actually transferred from the originator’s balance-sheet to the issuer of the securities. For instance, a bank makes auto loans and sells these loans to a SPE or SPV that structures these assets into a homogeneous asset pool. The SPE retains the loan as collateral, sells the pool to investors and pays the bank for the loans bought from it with the proceeds from the sale of securities.

At the end of the tenure of the securitization, the residual assets are passed on to the investors. If the asset quality deteriorates, the investors have to bear the loss. The investors receive variable coupon payments depending upon the risk they decide to bear. The investors who are ready to take the first loss get the maximum spread. The originator, in this fashion, has passed on the risk associated with the assets to the investor.

Figure 8.3 depicts a typical securitization process.

Securitization can be seen as the method of turning un-tradable and illiquid assets into various types of securities, which can then be sold to different investors with different risk appetites. These different types of securities with different inherent risks are known as the ‘tranches’. Technically, securitization is defined as a transaction involving one or more underlying credit exposures from which tranches that reflect different degrees of credit risk are created. Credit exposures may include loans, commitments and receivables. It may take the form of a security or of an unfunded credit derivative (to be explained later). The payments to investors depend upon the performance of specified underlying credit exposures. The salient features of securitization are outlined in Annexure II of this chapter.

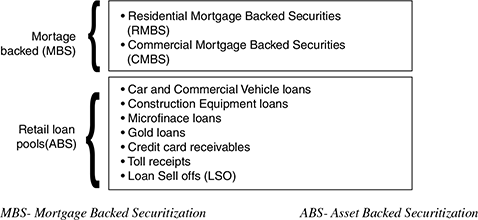

The securities sold to investors are called ‘asset-backed securities’ (ABS), since they are backed by the homogeneous pool of underlying assets. Originators of ABS usually want to sell loans ‘without recourse’.22 Hence, investors usually safeguard their interests through three mechanisms—(a) over collateralization, (b) senior/subordinated structures, and (3) credit enhancement.

- ‘Over collateralization’, as the nomenclature implies, involves structuring a collateral pool to ensure cash flow in excess of the amount required to pay the principal and interest on the securities.

FIGURE 8.3 A TYPICAL SECURITIZATION PROCESS

- In the ‘senior/subordinated structures’, the issuer of securities sells two categories of certificates—senior and junior—both secured by the same collateral pool. The senior certificates are usually taken by investors, while the originator itself may purchase the junior certificates. The cash flows from the collateral are first allocated to make payments to senior holders and the residual cash flows are allocated to junior holders. In other words, the actual losses should not exceed the promised payments to subordinated certificate holders. Therefore, the larger the component of junior holders, the greater the protection for senior investors.

- ‘Credit enhancements’, such as letters of credit are used to cover losses in the collateral. A bank other than the originating bank issues the letter of credit, generally covering a certain proportion of the loss on the pool (comparable to historical losses plus a margin) for a fee.

Thus, securitization is seen to benefit banks by providing liquidity to banks’ loan portfolios and mitigating credit risk by removing assets from banks’ books. Other spin offs include a possible lowering of interest rate risk and profitability enhancement through better asset turnover and fee-based income.

Box 8.1 provides an overview of collateralized debt obligations (CDOs) and compares them with securitization.

BOX 8.1 WHAT ARE CDOs/CBOs/CLOs?

These are the fastest growing segment of the securitization market. Banks resort to securitization with the following predominant motives-sourcing cheaper funds, attaining higher regulatory capital, better asset—liability management and reduced NPAs or under-performing assets.

Where the originating bank transfers a pool of loans, the bonds that emerge are called ‘collateralized loan obligations’ (CLOs). Where the bank transfers a portfolio of bonds and securitizes the same, the resulting securitized bonds are termed ‘collateralized bond obligations’ (CBOs). A generic name given to both these is ‘CDOs’. Some banks even securitize their equity investments—calling them ‘collateralized investment obligations’ (CIOs).

Difference between securitization and CDO structures

Though the essential nature of the structures are similar, securitization in its generic form and issuing CBO/CLO at the instance of banks, differ in respect of the following.

- For typical securitizations the primary objective is liquidity, while in the case of CBO/CLOs, the objectives could be capital relief, risk transfer, arbitraging profits or balance sheet optimization.

- While securitizations of, say, mortgage portfolios or auto loan portfolios could have thousands of obligors, CDO pools typically have only 100–200 loans.

- The loans/bonds are mostly heterogeneous in CDOs, whereas the securitized assets are typically homogeneous pools. The originator of CDOs might try to bunch together uncorrelated loans to provide the benefits of a diversified portfolio.

- Most CDO structures use a tranched and multi-layered structure with a substantial amount of residual interest retained by the originator.

- Generally, CDO issues will use a reinvestment period and an amortization period. Some tranches might have a ‘soft bullet’ repayment (a bullet repayment that is not guaranteed by any third party).

- Arbitraging is a common practice in the CDO market, where larger banks buy out loans from smaller ones and securitize them, earning arbitrage revenues in the process. There is a class of CDOs called arbitrage CDOs where the originating bank buys loans/bonds from the market and securitizes the same for gaining an advantage on the rates. Since the motive of such securitizations is arbitraging, such CDOs are called arbitrage CLOs/CBOs. To distinguish these from the ones where a bank securitizes its own receivables, the latter are sometimes referred to as ‘balance sheet CLOs/CBOs’.

Yet another upcoming variety of CLOs is ‘synthetic CLOs’. Here the originating bank merely securitizes the credit risk23 and retains the loans on its balance sheet. Synthetic CLOs repackage the underlying loans into cash flows that suit the needs of the investors and are not dependant on the repayment structure of the underlying loans.

To summarize, CDOs could fall into two basic categories: balance sheet CDOs and arbitrage CDOs. In the case of balance sheet CDOs, loans are actually transferred from the balance sheet of the originator and therefore impact the originating bank’s balance sheet. In the case of arbitrage CDOs, the originator merely ‘buys’ loans or bonds or asset-backed securities from the market, pools and securitizes them as a repackaged entity. The prime objective of balance sheet CDOs is to reduce risk and regulatory capital, while the purpose of arbitrage CDOs is to make profits from arbitrage.

Balance sheet CDOs could be further classified into cash flow CDOs and synthetic CDOs based on the nature of their assets.

In the case of ‘cash flow CDOs’, the assets are acquired for cash. The originating bank transfers a portfolio of loans into an SPV. ‘Master trust’ structures are commonly employed in CDOs to enable the bank to keep transferring loans into the pool on a regular basis without having to do complex documentation for every transfer. In view of the varied repayment structure of commercial loans, cash flow CDOs typically repay through bullet repayments and, hence, have a reinvestment period, during which the cash flows from repayments are reinvested.

However, a synthetic CDO primarily acquires ‘synthetic’ assets by selling ‘protection’24 rather than buying assets for cash. Hence, the funding requirement for a synthetic CDO is much lower than that for a cash flow CDO. The amount of cash raised is limited only to the extent of expected and unexpected losses (EL and UL) in the portfolio of synthetic assets, such that the highest of the cash liabilities can get an investment grade rating. Once the senior most cash liability obtains investment grade rating, the synthetic CDO does not raise more cash—it merely raises a synthetic ‘liability’ by buying protection from a super-senior swap provider. A typical structure in a synthetic CDO is illustrated in Figure 8.4. Clearly, the three different ‘tranches’ have different risk characteristics.

FIGURE 8.4 TYPICAL STRUCTURE OF A SYNTHETIC CDO

TEASE THE CONCEPT

Why would banks be tempted to sell only their best assets under the securitization process?

Let us now sum up the alternatives discussed so far in respect of a bank that has to deal with credit risk in its loan portfolio.

- It can continue to hold the loans, assess the EL periodically, take preventive or remedial measures to reduce the risk of loss or make a provision on the EL and allocate capital for UL.

- It can diversify its loan portfolio with several small loans to different counter parties, so that a few expected defaults may not lead to earnings volatility.

- It can negotiate a loan sale for the whole or part of the loan amount and incur the costs associated with the loan sale.

In resorting to the first alternative—(a) the bank runs the risk of earnings erosion if the provisions are substantial in value. It is not always easy to diversify the portfolio as in alternative; (b) since the bank’s operations, driven by its own internal skills and external competition, may not be able to balance the portfolio as optimally as it would like to. Further, a highly diversified portfolio is no complete hedge against borrower defaults and could lead to high transaction costs. Beyond diversification, banks look to sell off or securitize the loans as in the alternative; and (c) and this approach is seen to work well for standardized payment schedules and homogeneous credit risk characteristics. Commercial and industrial loans exhibit varied credit risk characteristics and can be sold or securitized through the CDO route as described above. In many cases, the banks themselves may not want the loans or more specifically, the ‘borrowers’ off their balance sheets and may merely want to hedge against the credit risk inherent in the loan transaction.

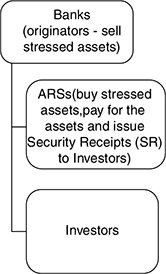

Asset Reconstruction Companies (ARC)

Asset Reconstruction Companies function as the Special Purpose Vehicles designed to hold the pools of securitized assets. Globally, countries have successfully implemented different models of ARCs to resolve the build up of non performing assets. Successful transfer of stressed assets to ARCs has resulted from creating a supportive regulatory environment. ARCs function like Asset Management companies transferring the acquired assets to one or more trusts (at the price at which the financial assets were acquired from the originator). Then, the trusts issue security receipts (SRs) to qualified institutional buyers (QIBs) and the ARCs receive management fees from the trusts. Any profit between the acquired price and the realized price is shared between the beneficiary of the trusts (banks/FIs) and ARCs.

The process is shown in Figure 8.5

FIGURE 8.5 ARC PROCESS

The trust acquires NPAs from banks/FIs by forming different trusts for the financial assets taken over. NPA are acquired from banks/FIs at fair value based on assessment of realisable amount and time to resolution. The maximum life of the trust may be prescribed by regulations. The trust is set up as a pass through entity (PTC) for Income tax purposes.

- Accordingly, the trusts issues securities (SR) to the investors which are usually QIBs or the seller bank itself. Therefore in case the seller bank is itself buying the SR in the Trusts, its status changes from lender of the loan to that of investor in the SR. SR represents undivided right, title and interest in the trust fund. After acquiring the NPA, the trust becomes the legal owner and the security holders its immediate beneficiaries. The Securitisation Act prescribes that an ARC has to make a minimum of 5% investment in the trust.

- The Trust redeems the investment to the SR holders out of the money realised from the borrowers. The ARC facilitates the whole working.

The NPAs acquired are held in an asset specific or portfolio trust scheme. In the portfolio approach, due to the small size of the aggregate debt the ARC makes a portfolio of the loan assets from different banks and FIs. Whereas when the size of the aggregate debt of a bank/FI is large, the trust takes an asset specific approach.

ARCs have several advantages. They help banks to focus on their core business by taking over the responsibility of resolving stressed assets. ARCs help in enabling industry to acquire expertise in loan-resolution arrangements and develop secondary markets for stressed assets. ARCs benefit the overall economy by trying to restore the operational efficiency of financially unviable assets after their acquisition by unlocking their true potential value or disposing them off, so that funds blocked in these assets could be released and invested in more productive sectors in the economy.

Covered Bonds

Covered bonds are not a new concept. They have been around for over 200 years, with a striking ‘zero’ default record! They have historically been associated with Germany—Pfandbriefe and Denmark–realkreditobligatione

Covered bonds are a hybrid between asset-backed securities/mortgage backed securities and normal secured corporate bonds, and serve as an instrument of refinancing, primarily used by mortgage lenders. Unlike secured corporate bonds which provide recourse against the issuer, covered bonds provide a bankruptcy-protected recourse against the assets of the issuer (Collateral Pool) too. Unlike mortgage backed securities which merely provide recourse against the Collateral Pool, covered bonds provide an additional recourse against the issuer too.

Covered bonds can therefore be defined as fixed income instruments that are unconditional obligations of the issuer, but containing an additional recourse against assets of a specified ‘cover pool’, the rights over which are protected, either by legislation or by using special legal devices, such that investors in the covered bonds have bankruptcy-protected claim against such cover pool.

Covered bonds are essentially used to raise liquidity through a bond issue, backed by a pool of assets. They combine the features of securitization and corporate bonds (debt instruments, more about which can be found in later chapters).

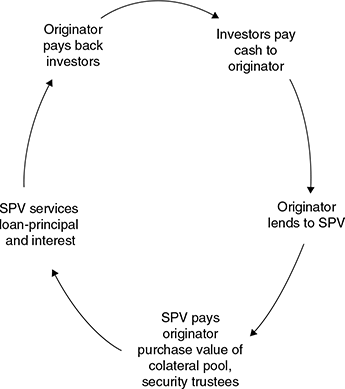

Typical covered bond issue process and cash payment structures are shown in Figures 8.5 and 8.6.

FIGURE 8.5 AT THE TIME OF ISSUING A COVERED BOND

FIGURE 8.6 FLOW OF CASH PAYMENTS IN A STRUCTURED COVERED BOND

It can be understood from the diagrammatic representations that the covered bond, like a securitized asset, is backed by a pool of identifiable assets usually with a level of over collateralization. But there are many points of difference that add up to making covered bonds a viable alternative to securitization.

Traditionally, covered bonds have been used in mortgage refinancing. However, unlike in traditional Mortgage backed securities (MBS), where the pool of underlying mortgages is static, the pool underlying covered bonds is a dynamic pool. Hence the generic structure of covered bonds resembles secured bonds.

Unlike securitization, which does not depend on the rating of the issuer, covered bonds do depend on ratings, but have additional advantage of ‘ring fenced’, high quality assets to back the pool. The quality of underlying asset pool in covered bonds is laid down by specific legislation or common law of the country.

Covered bonds are shown on the balance sheet of the originator, who is therefore subject to default risk and prepayment risk of bondholders. Contrast this with securitization, where the default risk of the assets (and the prepayment risk) is passed on to the investors, and the assets are taken off the originator’s balance sheet.

How do originators/issuers benefit from covered bonds?

- Originators are able to get higher leverage. The rationale for this is that mortgage lending, where covered bonds are the most prevalent, is low risk, low return business, where cash flows are recovered over a long period in time. Hence, for mortgage lenders to get a higher return on their equity, higher leverage is the preferred tool. This fact has been recognized by regulators too. Higher leverage also implies that originators have to constantly seek additional sources of funds. Covered bonds provide one such additional source of funds. The leverage that a covered bond issue can command is directly linked to the quality of underlying assets and the extent of over collateralization. Hence, originators will be able to raise funds only to the extent of the economic capital that the pool requires. (The concept of ‘economic capital’ is discussed in detail in the chapter ‘Capital—risk, regulation and adequacy’)

- Originators can get better ratings for the covered bond issue than their own ratings. This is due to the fact that the ‘cover pool’ of assets that will form the security for the covered bonds would be high quality assets, whose quality would either be stipulated by law or stated in specific legislations.

- Lower cost to originator as a direct result of better ratings.

- Originators can achieve better asset liability matches (asset liability matching is discussed in the chapter ‘Bank risk management’). In a covered bond program there may be asset liability mismatches. The underlying asset is a long term mortgage asset (with a maturity typically greater than 10 years), while covered bonds may be issued with short term or medium term maturities. This would mean that the normal asset amortization alone may be insufficient to pay the bonds on time. While evaluating the asset-liability mismatches, there are two risks that are taken into consideration: (a) asset risk; and (b) cash flow risk. These are dealt with while structuring of the transaction. Thereafter, reliance is placed on the debt service capacity of the issuer. Over and above these, the issuer may need liquidity facility provider to meet the covered bond maturities. The less the magnitude of the asset liability mismatch, the higher the rating for the bonds.

- Originators’ exposure to the capital market yields better reputation. Further the accountability to the capital market brings in better governance, discipline and best practices to the originator.

How do covered bonds benefit the borrowers/investors?

If covered bonds are able to bring down the cost of mortgage refinancing, the same would eventually translate into lower mortgage lending costs. In addition, covered bonds result into standardization of mortgage lending procedures and underwriting norms—all of which make pricing of mortgages far more transparent.

How do covered bonds benefit the economy?

Integration of capital markets with mortgage markets is an important step in the economic development of a country. Securitization is an extreme form of transforming illiquid assets into tradable securities in the capital market. However, post the 2007 crisis, the securitization model was seen as creating problems of moral hazard and adverse selection. As a device of capital market funding, covered bonds are mid-way between securitization and straight corporate bonds, since they combine the benefits of both.

One of the biggest advantages of covered bonds in future will be the liquidity requirements under Basel III (Please see chapter ‘Capital—risk, regulation and adequacy’). Basel III proposes to impose a Liquidity Coverage Ratio requirement for banks according to which banks are to maintain at least 30 days’ cash flows in ‘highly liquid assets’. Covered bonds of a certain rating would qualify as liquid assets for this requirement.

About 32 countries have already passed laws in respect of covered bonds. The National Housing bank (NHB) of India is actively considering introducing covered bonds in the country’s residential mortgage market. A working group submitted its report on the subject in October 2012. A draft National Housing Bank Covered Bonds Regulations, 2012, has also been proposed in the report.

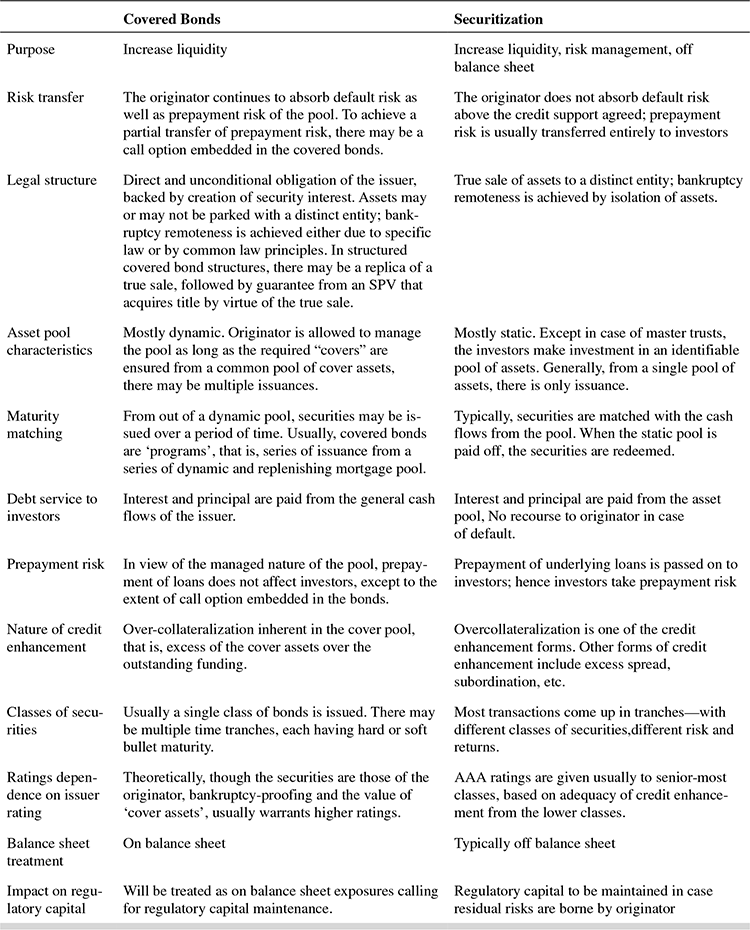

Comparing Securitization and Covered Bonds

Table 8.4 compares securitization and covered bonds on various parameters

TABLE 8.4 COVERED BONDS VS SECURITIZATION

Box 8.2 provides an overview of the legislation governing covered bonds in select countries.

BOX 8.2 LEGISLATION ON COVERED BONDS – SELECT COUNTRIES

Legislation on covered bonds—select countries

The USA

The Covered Bonds Bill, 2011 provides for different Covered Bonds Regulators for different categories of issuers that may be an insurer, a bank holding company, any NBFC, etc.

A wide range of assets including residential assets as well as commercial assets qualify as eligible assets. Also, the Cover Pool may be comprised of ancillary assets and substitute assets. A loan will not qualify as eligible asset if it is delinquent for more than 60 consecutive days. The Bill stipulates minimum over-collateralization requirements to be established.

Singapore

In Singapore, the Monetary Authority of Singapore came up with Proposed Consultation Paper on Covered Bonds Issuance by Banks incorporated in Singapore in March, 2012. According to the proposal, Covered Bond holders will have dual recourse against the issuing bank as well as the Cover pool. Further, the aggregate value of assets in the cover pool is to be capped at 2 per cent of the value of the total assets of the bank. Only residential mortgage loans and the derivatives held for the purpose of hedging risks arising from issuing covered bonds are proposed as eligible constituents of the Cover Pool. A minimum over-collateralization of 103 per cent and a LTV (Loan to Value Ratio) of 80 per cent have also been proposed.

The UK

The Regulated Covered Bonds Regulations 2008 (amended periodically) constitute the regulatory framework for Covered Bonds in the United Kingdom (UK). The Asset Pool should consist of eligible property (e.g., loans to registered social landlord, loans to a project company for specified projects, etc. or any interest in eligible assets specified in any one of the classes: public sector assets, residential mortgage assets and commercial mortgage assets) which shall be situated in particular areas only.

Europe

The European covered bond council (ECBC) has stipulated criteria that issuers will have to satisfy, and the ‘covered bond label convention’—as the legislation will be called—is likely to be passed.

Credit Derivatives

Due to the difficulties experienced by bankers with alternative methods of dealing with credit risk, another alternative has emerged: ‘credit derivatives’—a more specialized way to insure against credit-related losses.

Credit derivatives are an effective means of protecting against credit risk. They come in many shapes and sizes, but all serve the same purpose. Simply stated, a credit derivative is a security with a pay-off linked to a credit related event, such as borrower default, credit rating downgrades or a structural change in a security containing credit risk.

There are different types of credit derivatives, but we will take a brief look in this section at the commonly used derivatives. Some analysts classify credit derivatives into two categories in terms of how they are valued or priced, namely ‘replication’ products and ‘default’ products. Replication products, as the name suggests, replicate the money market transactions, such as credit spread options, while default products, such as credit default swaps (CDS) are priced on the basis of the PD of the asset whose risk is being transferred, the exposure at risk and the expected recovery rate. Another common classification is on the basis of performance—‘protection like’ products (e.g., credit default options and CDS) and ‘exchange like’ products (e.g., total return swaps).

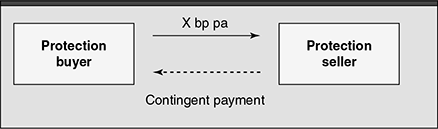

In credit derivatives, there is a party (or a bank) trying to transfer credit risk, called protection buyer and there is a counter party (another bank) trying to acquire credit risk, called protection seller. Over time, the credit derivatives market has become a trading market. Trades in credit derivatives are taken to be proxies for trades in actual loans or bonds of the reference entity and the borrower. For example, a bank willing to acquire exposure in a particular borrower would sell protection with reference to the borrower, while a bank wanting to hedge the risk of lending to the same borrower will buy protection.

Credit derivatives are typically unfunded—the protection seller is not required to put in any money upfront. The protection buyer generally pays a periodic premium. However, the credit derivative may be funded in some cases. For example, the protection buyer may require the protection seller to pre-pay the entire notional value of the contract upfront (as in the case of a ‘credit-linked note’ (CLN) discussed later in this section).

As is typical of derivatives, a credit derivative does not require either of the parties—the protection seller or protection buyer—to actually hold the reference asset (the credit that is being hedged). Thus, a bank may buy protection for an exposure it has taken or has not taken, irrespective of the amount or term of the actual exposure. It, therefore, follows that the amount of compensation claimed under a credit derivative may not be related to the actual losses suffered by the protection buyer.

When a credit event (as specified in the contract between the protection buyer and seller) takes place, there are two ways of settlement—cash and physical. In a cash settlement, the reference asset will be valued and the difference between its par and fair value will be paid by the protection seller. In the case of physical settlement, the protection seller would acquire the defaulted asset for its full par.

Box 8.3 provides an insight into the evolution of credit derivatives.

BOX 8.3 EVOLUTION OF CREDIT DERIVATIVES25

In March 1993, Global Finance carried a feature on J. P. Morgan, Merrill Lynch and Bankers Trust, which were already then marketing some form of credit derivatives. This article also prophesied, quite rightly, that credit derivatives could, within a few years, rival the USD 40 trillion market for interest rate swaps.

In November 1993, Investment Dealers Digest carried an article titled ‘Derivatives Pros Snubbed on Latest Exotic Product’ which claimed that a number of private credit derivative deals had been seen in the market but it was doubted if they were ever completed. The article also said that Standard and Poor’s had refused to rate credit derivative products and this refusal may put a permanent damper on the fledgling market. One commentator quoted in the article said: ‘It (credit derivatives) is like Russian roulette. It doesn’t make a difference if there’s only one bullet: If you get it you die’.

Almost 3 years later, Euromoney reported (March 1996 ‘Credit Derivatives Get Cracking’) that a lot of credit derivatives deals were already happening. The article was optimistic: ‘The potential of credit derivatives is immense. There are hundreds of possible applications: for commercial banks which want to change the risk profile of their loan books, for investment banks managing huge bond and derivatives portfolios, for manufacturing companies over-exposed to a single customer, for equity investors in project finance deals with unacceptable sovereign risk, for institutional investors that have unusual risk appetites (or just want to speculate) and even for employees worried about the safety of their deferred remuneration. The potential uses are so widespread that some market participants argue that credit derivatives could eventually outstrip all other derivative products in size and importance’.

Some significant milestones in the development of credit derivatives have been as follows:

- 1992: Credit derivatives emerge. ISDA26 first uses the term ‘credit derivatives’ to describe a new exotic type of over-the-counter contract.

- 1993: KMV introduces the first version of its Portfolio Manager model, the first credit portfolio model.

- 1994: Credit derivatives market begins to evolve. There are doubts expressed by some.

- September 1996: The first CLO of UK’s National Westminster Bank.

- April 1997: J P Morgan launches Credit Metrics.

- October 1997: Credit Suisse launches CreditRisk+

- December 1997: The first synthetic securitization, JP Morgan’s BISTRO deal.

- July 1999: Credit derivative definitions issued by ISDA.

Why Do Banks Use Credit Derivatives?

- They are an easy and cost-effective means to hedge portfolio risk.

- They permit substantial flexibility and hence increase the portfolio efficiency. For instance, the bank may have made a loan with 5-year maturity, but may be concerned with the risk over the next 2-year period only. The credit derivative permits the bank to allocate this risk to another party. The bank also effectively creates a 2-year security with many of the pricing characteristics of the 5-year loan. There are thus endless possibilities to create and structure flexible credit derivatives.

- They can be used to hedge against interest rate risks.

- Credit derivatives are often more efficient than loan sales since some investors who are unwilling to participate in the loan sales market are more willing to acquire credit derivatives.

- The bank transferring its credit risk may not want its actions to be visible to its borrowers and competitors and hence may want to use credit derivatives.

- Loan sales call for substantial information sharing among participants and the bank is likely to incur higher administrative costs and more obligations.

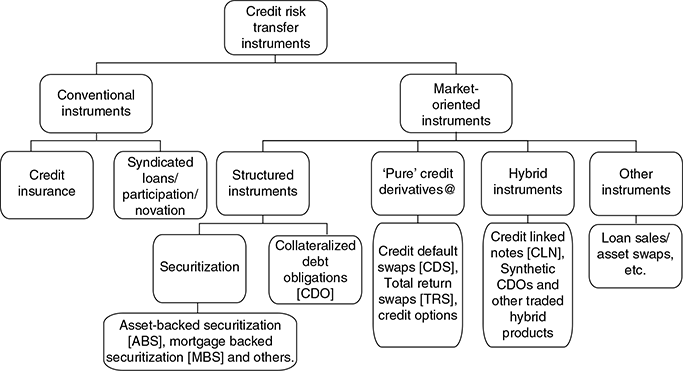

The popular credit risk transfer instruments can be summarized in Figure 8.7.

FIGURE 8.7 CATEGORIZATION OF CREDIT RISK TRANSFER INSTRUMENTS

Some Basic Credit Derivative Structures

There are many kinds of credit derivatives and to enumerate and describe them would be beyond the scope of this book. Further, most credit derivatives, like other derivatives, can be ‘structured’ to meet the specific requirements of the protection buyers and sellers.

However, we briefly describe some popular types of credit derivatives as follows:

- Loan portfolio swap27: Banks swap loan portfolios to diversify their credit exposures to a particular industry or activity. For instance, if Bank X has more real estate loans in its portfolio and Bank Y has more loans to technology firms, X and Y can agree to swap payments received on a basket of each bank’s loan exposures.

- Total return swap: This is one of the most popular credit derivative instruments. The steps involved in the swap are as follows:

- Bank A has made 5-year loan to firm XYZ. The bank would like to hedge its credit risk on the loan. Bank A is called the ‘beneficiary’ or the ‘protection buyer’.

- In terms of the swap agreement, Bank A agrees to pay Bank B, who is called the ‘guarantor’ or ‘protection seller’, the ‘total return’ on the ‘reference asset’, in this case, the loan to XYZ. The ‘total return’ comprises of all contractual payments on the loan, plus any appreciation in the market value of the reference asset.

- The swap arrangement is completed when Bank B agrees to pay a particular rate (which would include a ‘spread’ and an allowance for loan value depreciation) to Bank A. This rate is generally fixed based on a reference rate such as the London Inter Bank Offered Rate (LIBOR). Now, in effect, Bank B has a ‘synthetic’ ownership of the reference asset, since it has agreed to bear the risks and rewards of such ownership over the swap period. Bank B, therefore, assumes the credit risk and receives a ‘risk premium’ for doing so. The greater the credit risk, the higher the risk premium.

- On the date of a specified payment or when the derivative matures or on the happening of a specified event, such as default, the contract terminates. Any depreciation or appreciation in the amortized value of the reference asset (the loan to XYZ) is arrived at as the difference between the notional principal amount of the reference asset and the dealer price.

- If the dealer price is less than the notional principal amount on the date of contract termination, Bank B must pay the difference to Bank A, absorbing any loss due to the decline in credit quality of the reference asset.

To sum up, the protection buyer makes payments based on the total returns from the reference asset—the loan to XYZ—as seen in Figure 8.8.

FIGURE 8.8 TOTAL RETURN SWAP

The total returns include contractual payments on the loan plus appreciation of the loan value. In return, the protection seller makes regular contracted payments, fixed or floating, which include a spread over funding costs plus the depreciation value (the ‘protection’). Both parties make payments based on the same notional amount. The protection seller gets the advantage of returns without holding the asset on its balance sheet. The protection buyer can negotiate credit protection without having to liquidate the underlying asset. In floating rate contracts, not only is interest rate risk hedged, but also the risk of deterioration of credit quality (which can occur even where there is no default).

Some advantages of the TR swap are as follows:

- Since the asset is never transferred, the bank seeking protection can diversify its credit risk without the need to divulge confidential information on the borrower.

- The features of this type of credit protection are seen to have lower administration costs, as compared to loan liquidation.

- Banks with high funding levels can take advantage of other banks’ lower cost balance sheets through such TR swaps. This facilitates diversification of the user’s asset portfolio as well.

- The maturity of a TR Swap does not have to match the maturity of the underlying asset. Therefore, the protection seller in a swap with maturity less than that of the underlying asset may benefit from the ‘positive carry’ associated with being able to roll forward short-term synthetic financing of a longer-term investment. The protection buyer (TR payer) may benefit from being able to purchase protection for a limited period without having to liquidate the asset permanently. At the maturity of a TR Swap whose term is less than that of the reference asset, the protection seller has the option to reinvest in that asset (by continuing to own it) or to sell it at the market price.

- Other applications of TR Swaps include making new asset classes accessible to investors for whom administrative complexity or lending group restrictions imposed by borrowers have traditionally presented barriers to entry. Recently, insurance companies and levered fund managers have made use of TR Swaps to access bank loan markets.

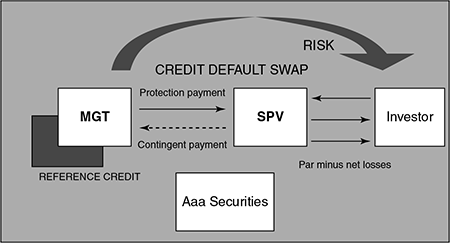

- Credit default swap (CDS): The CDS provides protection against specific credit-related events and, hence, bears more resemblance to a financial bank guarantee or a standby letter of credit, than to a ‘swap’. Under this agreement, the protection buyer (Bank A in our earlier example) pays the protection seller (Bank B) only a fixed periodic amount over the life of the agreement.

Figure 8.9 illustrates the mechanics of a CDS. The following chapter provides an overview of the mechanics of pricing and trading in the CDS.

The steps in which a basic CDS proceeds are as follows:

- Bank A agrees to pay a fee to Bank B for being guarantor or protection seller. The fee amounts to a specified number of basis points on the value of the reference asset (the loan made by Bank A).

- Bank B agrees to pay a pre-determined, market value based amount (usually a percentage of the value of the reference asset) in the event of credit default. The ‘event of default’ is rigorously defined in the contract—it could take the form of verifiable events such as bankruptcy, payment default or can amount to a specific amount of loss sustained by the protection seeker due to the credit (‘materiality threshold’). Bank B is not required to make any payment unless there is a default within the period of the swap.

- The amount to be paid by Bank B, post-default, will be defined in the contract. This amount usually represents the difference between the reference asset’s initial principal and the actual market value of the defaulted reference asset. The amount is settled through the ‘cash settlement’ mechanism.28

To lower the cost of protection in a credit swap, contingent credit swaps are employed. Contingent credit swaps are hybrid credit derivatives which, in addition to the occurrence of a credit event, require an additional trigger. Such a trigger could typically be tied to the occurrence of a credit event with respect to another reference asset or a material movement in equity prices, commodity prices or interest rates. The credit protection provided by a contingent credit swap, being weaker, is cheaper than that provided under a regular credit swap.

- Credit risk options: These options provide the protection buyer a valuable hedge against interest rate risk, primarily arising out of a downgrade in a borrower’s credit rating. Consider this example. When Bank A entered into a loan agreement with firm XYZ, the firm had an investment grade rating and the loan price was fixed accordingly on floating terms. However, in a year’s time, firm XYZ witnessed a slide in its credit rating, due to various factors. This implies that Bank A will have to raise the risk premium and run the risk of default by XYZ or retain the contracted rate and take on higher risk. The third option available to Bank A is to enter into a contract with Bank B, the protection seller. Bank B writes a simple European option with a fixed maturity, agreeing to compensate Bank A for the decline in credit quality due to the lower credit rating of XYZ.

Credit options can also be put or call options on the price of either a floating rate note bond or loan. In this case, the credit put (or call) option grants the option buyer the right, but not the obligation, to sell to (or buy from) the option seller a specified floating rate reference asset at a pre-specified price (the ‘strike price’). Settlement may be on a cash or physical basis.

The other settlement method is for the protection buyer to make physical delivery of a portfolio of specified deliverable obligations in return for payment of their face amount. Deliverable obligations may be the reference obligation or one of a broad class of obligations meeting certain specifications, such as any senior unsecured claim against the reference entity.

- Credit intermediation swap: In a credit intermediation swap, one creditworthy bank serves as an intermediary between two smaller banks to alleviate credit concerns in the swap transaction. For example, let us assume two small regional banks are keen on entering into a swap contract with each other. Both of them do not have much market presence or credibility and are not convinced of each other’s capability of honouring the respective commitments under the swap. The two small banks, therefore, invite a large prime bank with national/international presence to guarantee the swap. The two smaller banks can either pay to the large bank at floating rate and receive fixed rate in return or pay at fixed rate and receive floating rate. The difference between the rates received and paid forms the income for the large bank for accepting the credit risk of the two smaller banks.

- Dynamic credit swap: An important innovation in credit derivatives is the dynamic credit swap. The protection buyer pays a fixed fee, either up front or periodically, which once set does not vary with the size of the protection provided. The protection buyer will only incur default losses if the swap counter party and the protection seller fail. This dual credit effect means that the credit quality of the protection buyer’s position is at a level better than the quality of either of its individual counter parties. Also, assuming uncorrelated counter parties, the probability of a joint default is small.

Foreign currency denominated exposure may also be hedged using a dynamic credit swap where a creditor is owed an amount denominated in a foreign currency. This is analogous to the credit exposure in a cross-currency swap.

- Credit spread derivatives: Credit spread is the difference between the interest rates of risk-free government securities and risky debt29 in the market. Let us assume that interest rates move consistently with the market. That is, a one per cent change in government securities rate leads to a similar change in the debt market. If this is so, any difference between the two rates could be attributed to credit risk for the risky debt. Derivatives written on this spread are credit spread options/forwards/swaps.

For example, a ‘credit spread call’ is a call option on credit spreads. If the spread increases, the value of the call increases and pays off if the credit spread at maturity exceeds the strike price of the call option.

The ‘asset swap package’ consists of a credit-risky instrument (with any payment characteristics) and a corresponding derivative contract. The contract exchanges the cash flows of the credit-risky instrument for a floating rate cash flow stream.30 Credit options may be American, European or multi-European. Their structure may transfer default risk or credit spread risk or both.

Credit options have found favour with investors and banks for the following reasons:

- Institutional investors see credit options as a means of increasing yields, especially when credit spreads are thin and they find themselves underinvested. These investors prefer to bear the risk of owning (in a put option) or losing (in a call option) an asset at a predetermined price in future and collect current income commensurate with the risk taken.

- Banks, with their highly leveraged balance sheets, prefer credit options since they are off-balance sheet. Further, the credit options and credit swaps are structured to trigger payments upon the happening of a specific event, which help in mitigating credit exposure risk.

- Such options are also attractive for portfolios that are forced to sell deteriorating assets. Options are structured to reduce the risk of forced sales at distressed prices and consequently enable the portfolio manager to own assets of marginal credit quality at lower risk. Where the cost of such protection is less than the benefit in terms of increased yield from weaker credits, a distinct improvement in portfolio risk-adjusted returns can be achieved.

- Borrowers also find options useful for locking in future borrowing costs without impacting their balance sheets. Prior to the advent of credit derivatives, borrowers had to issue debt immediately, even if they had no requirement for the entire amount of debt all at once. The unutilized debt could be invested in other liquid assets, till the requirement for funds came up. This had the adverse effect of inflating the current balance sheet and exposing the issuer to reinvestment risk and often, negative carry.31 Today, issuers can enter into credit options on their own name and lock in future borrowing costs with certainty.

- Credit linked notes (CLN): This is a funded credit derivative where the protection buyer requires the protection seller to make upfront payments. In return, the protection buyer issues a note called ‘CLN’. The CLN is largely similar to any other bond or note. The simplest form of a CLN is represented by a standard note with an embedded CDS. These are typically issued by a trust or SPE. The steps in issuing CLNs are as follows:

- The bank seeking to issue CLNs (Bank A) sets up an SPE, in the form of a ‘trust’. The CLNs are intended to protect Bank A in the event the borrower firm XYZ is unable to repay its debt to the bank.

- Investors or other banks (say, Bank B) buy into these trusts and receive a CLN for a fixed period, say, 3 years.

- The trust offers a steady stream of fixed payments to Bank B over the 3-year period. These payments constitute interest plus a risk premium. The total return on the notes is linked to the market value of the underlying pool of debt securities.

- Bank A invests the funds received from Bank B in relatively risk-free securities, including highly rated corporate bonds.

- If, during the 3-year period of the CLN, firm XYZ keeps up regular payments to Bank A, it returns the investment made by Bank B.

- If firm XYZ defaults in payment, Bank A compensates its possible loss by liquidating the risk-free security investments. Bank B receives firm XYZ’s debt, which could have turned unsecured or worthless.

Issuers find CLNs attractive, because the ‘risk’ attached to a particular borrower is hedged and, therefore, the immediate need for more regulatory capital is avoided. The investing banks find CLNs attractive, because they are able to find a pool of leveraged securities, which could give them good income.

CLNs are used in several ways in practice. Four typical situations32 are presented as follows:

- Bank A has credit exposure to a firm S in a specific industry/sector. Institution C, an institutional investor, cannot, by policy or regulation, gain direct exposure to the industry that S is in, but is interested in reaping the benefits of such exposure. C therefore enters into a CLN contract with Bank A, by which A sells a note to C with underlying exposure equal to the face value of the reference asset S. In return, A receives from C, at the beginning of the contract, the face value of S in cash. In compensation, A pays to C a predetermined interest and some credit risk premium. In case of a credit event experienced by S during the contract period, A pays C the recovery proceeds of S. If the recovery value of S is less than what C paid for the asset, C suffers a loss. In case there is no credit event during the contract period, Bank A pays back to institution C the entire principal.

- The situation above is also applicable to any investor who wants to sell protection to Bank A through a CDS, but is unable to or does not want to access the credit derivatives market.

- Another common way to use a CLN is in buying protection. Bank A in the example above, the originator of the reference asset S, could buy protection from Bank B through a CLN, where A gets the value of the reference asset upfront (and pays interest and premium to the protection seller B). In a second case, Bank B could have sold protection through a CDS to A. Bank B now wants to guard itself against counter party risk, hence initiates a CLN contract with institution C or another Bank D. If the reference asset defaults, Bank A gets compensated as in example (a) above and Bank B makes the contingent payment on the default swap, which has already been compensated by the CLN. Thus, the CLN functions like insurance in both cases.

- Special purpose entities (SPEs) or trusts set up in the context of the CLN (as shown in Figure 8.10) are prevalently used in the case of synthetic CDOs (to be discussed in the next chapter).

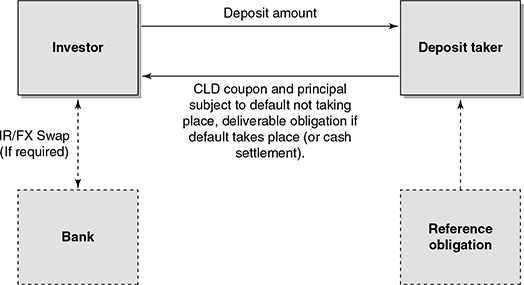

- Credit linked deposits/credit linked certificates of deposit: Credit linked deposits (CLDs) are structured deposits with embedded default swaps. Conceptually, they can be thought of as deposits along with a default swap that the investor sells to the deposit taker. The default contingency can be based on a variety of underlying assets, including a specific corporate loan or security, a portfolio of loans or securities or sovereign debt instruments or even a portfolio of contracts which give rise to credit exposure. If necessary, the structure can include an interest rate or foreign exchange swap to create cash flows required by investors. In effect, the depositor is selling protection on the reference obligation and earning a premium in the form of a yield spread over plain deposits. If a credit event occurs during the tenure of the CLD, the deposit is paid and the investor would get the deliverable obligation instead of the deposit amount. Figure 8.11 shows the structure of a simple CLD.

- Repackaged notes: Repackaging involves placing securities and derivatives in a SPV which then issues customized notes that are backed by the instruments placed. The difference between repackaged notes and CLDs is that while CLDs are default swaps embedded in deposits/notes, repackaged notes are issued against collateral—which typically would include cash collateral (bonds/loans/cash) and derivative contracts. Another feature of repackaged notes is that any issue by the SPV has recourse only to the collateral of that issue (Figure 8.12).

FIGURE 8.10 THE STRUCTURE OF A CLN

Source: The J.P. Morgan Guide to Credit Derivatives, 25.

Source: The J.P. Morgan Guide to Credit Derivatives, 25.FIGURE 8.11 STRUCTURE OF A CLD

Source: RBI, ‘Draft Guidelines for Introduction of Credit Derivatives in India’, Figure 4 (26 March 2003): 9.

Source: RBI, ‘Draft Guidelines for Introduction of Credit Derivatives in India’, Figure 4 (26 March 2003): 9.FIGURE 8.12 TRANSACTIONS UNDER A REPACKAGED NOTE

Source: RBI, ‘Draft Guidelines for Introduction of Credit Derivatives in India’, Figure 5 (26 March 2003): 10.

Source: RBI, ‘Draft Guidelines for Introduction of Credit Derivatives in India’, Figure 5 (26 March 2003): 10. - Basket default swap: A credit derivative may be with reference to a single reference asset or a portfolio of reference assets. Accordingly, it is termed a single credit derivative or a portfolio credit derivative. In a portfolio derivative, the protection seller is exposed to the risk of one or more components of the portfolio (to the extent of the notional value of the transaction).

A variant of a portfolio trade is a basket default swap. In this type of swap, there would be a bunch of assets, usually homogeneous. Let us assume that the swap is for the first to default in the basket. The protection seller sells protection on the whole basket, but once there is one default in the basket, the transaction is settled and closed. If the assets in the basket are uncorrelated, this allows the protection seller to leverage himself—his losses are limited to only one default but he actually takes exposure on all the names in the basket. And for the protection buyer, assuming the probability of the second default in a basket is quite low, he actually buys protection for the entire basket but paying a price which is much lower than the sum of individual prices in the basket.

Likewise, there might be a second-to-default or nth to default basket swaps. Box 8.4 sets out the operational requirements for credit derivatives as envisaged by the Basel Committee on Banking Supervision.33

BOX 8.4 OPERATIONAL REQUIREMENTS FOR CREDIT DERIVATIVES

In order for protection from a credit derivative to be recognized, the following conditions must be satisfied:

- The credit events specified by the contracting parties must at a minimum include:

- a failure to pay the amounts due according to reference asset specified in the contract,

- a reduction in the rate or amount of interest payable or the amount of scheduled interest accruals,

- a reduction in the amount of principal or premium payable at maturity or at scheduled redemption dates and

- a change in the ranking in the priority of payment of any obligation, causing the subordination of such obligation.

- Contracts allowing for cash settlement are recognized for capital purposes provided a robust valuation process is in place in order to estimate loss reliably. Further, there must be a clearly specified period for obtaining post-credit-event valuations of the reference asset, typically not more than 30 days.

- The credit protection must be legally enforceable in all relevant jurisdictions.

- Default events must be triggered by any material event, e.g., failure to make payment over a certain period or filing for bankruptcy or protection from creditors.

- The grace period in the credit derivative contract must not be longer than the grace period agreed upon under the loan agreement.