CHAPTER TWENTY

Cash Management and Demand Forecasting in ATMs1

CHAPTER STRUCTURE

Section II The Case of Bharath Bank

Section III The Case of Global Bank

Section IV Cash Demand Forecasting

KEY TAKEAWAYS FROM THE CHAPTER

- Learn how to determine the cash flow from banks and ATMs.

- Analyze forecasting methods to decide optimum cash in ATMs to avoid a stock-out situation.

- Analyze data from the ATMs of two banks in Mumbai city.

SECTION I

INTRODUCTION

All retail banks including leaders are competing for a larger share of customers’ financial transactions. Their efforts are directed toward attracting and retaining customers by offering them a basket of tailormade schemes supported by a state-of-the-art distribution system (the ATMs). The whole exercise is helping the banks to serve their customers fast and avoid human intervention totally. And for the customers, ATMs offer hassle-free cash withdrawal. There are no more fighting with the bank’s teller for change and fresh notes. The ATM has become a medium for non-cash transactions, such as payment of bills, insurance payments, printing of statements or even accessing the Internet.

Cash management service (CMS) is a new product off the block, which facilitates the banks to source cheaper funds and serve its clients (having widespread networks across the country) more efficiently. The analysis is based on the cases of two banks, namely Bharath Bank and Global Bank2 and the data from their ATMs in Mumbai city.

The product in this chain is cash. The objective of this chapter is to primarily study the information flow and the fund flow in the supply chain of the retail banks in the country.3 The supply chain in retail banks needs to be more responsive to the needs of the customers in comparison to the traditional FMCG industry. All the intermediaries in the supply chain play an important role in making the supply chain more efficient. The various aspects involved are the logistics involved in ATM operations, role of forecasting in retail outlets and ATMs and the parameters that are taken into consideration, scope of network sharing and issue of having the right mix of currency denomination to be able to satisfy the demand. The chronic problem faced in such a scenario is cash stock-outs and banks are increasingly trying to synergize their supply chain with that of the external agents (ATM vendors, outsourcing agents and VISA network) involved in this process.

The players in a retail bank’s supply chain are the RBI, the corporate branch of the bank in the city, the retail branches, the delivery channel coordinators, outsourced agents who take care of physical cash movement, ATMs and ATM vendors.

The key elements in the supply chain are cash flow, information flow and IT infrastructure, lead time of cash replenishment, payments and receipts, different denominations of currencies and geographical locations and status of accounts (corporate accounts and salary accounts).

In case of financial services and banks, it is presumed that the demand drivers for cash are those factors which increase the propensity of cash withdrawal (retail as well as ATMs) and cash deposits. Certain demand drivers having a substantial effect on the final level of demand are the following:

- Location of the branch/ATM

- Number of current accounts

- Resident accounts and their age profile (for example, some banks have a captive audience of pension holders)

- Number of salary accounts

- Seasonal factors including weekends and festivities

In order to understand this concept, two banks were selected—Bharath Bank and Global Bank. Their cases will be discussed in detail in the following sections.

SECTION II

THE CASE OF BHARATH BANK

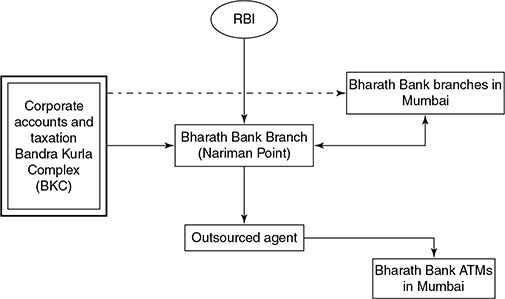

Let us assume that Bharath Bank has 22 branches and 120 ATMs in Mumbai. Like any bank in the country, it does maintain an account with the RBI for cash reserve rates (CRR) requirements. In addition to this, the RBI also offers a ‘currency chest’ facility to the banks. Under this facility, the banks can operate their accounts for their daily requirements of cash ensuring that the CRR is maintained at the end of the day. However, Bharath Bank has not subscribed to this facility. It uses its Nariman Point branch as the central point for all cash issuance to the branches and ATMs in Mumbai. Figure 20.1 describes the flow of funds in the entire retail banking segment of the bank.

In the case of Bharath Bank, the corporate accounts and taxation department at Bandra Kurla Complex (BKC) has worked out a certain retention limit for all the branches as well as the ATMs. The factors on which such a limit is calculated by the department are as follows:

- Total deposits of the branches

- Total advances (amount lent to the customers)

- Branch location

- Number of salary account holdings

- Corporate accounts, if any

- Total receipts/payments of the branch in the last three months

This figure of retention limit is shared across all the branches in Mumbai including the Nariman Point branch. Based on the retention limits as set by the bank’s BKC office, the cash management centre is responsible for distributing the funds to various branches (retail outlets) and the outsourced agents for ATMs. It needs to be mentioned here that all correspondence with the RBI regarding any kind of shortfall is carried out by the Nariman Point branch. However, Bharath Bank does not have any currency chest account with the RBI as it requires immense procedural hassles and formalities. Thus, at the end of the day, all branches are notified to return the excess cash above the retention limit to the Nariman Point branch, which remains in Bharath Bank’s custody.

Outsourced Agents for ATMs

Bharath Bank has only one outsourced agent—M/s Brinks Arya, for depositing cash in their 120 ATMs across Mumbai. Unlike in Global Bank, Brinks Arya does not maintain any vault cash account, i.e., it does not maintain certain cash balance/overdraft account with Bharath Bank. The outsourcing agent’s account gets debited when it collects cash from the bank and it gets adjusted when the money is transferred to the ATMs.

Bharath Bank ATMs The ATM operation is coordinated by a delivery channel coordinator and it is similar to the functioning of Global Bank. The ATM switch is located at BKC and all forecasting is carried out in BKC. Bharath Bank deploys only one outsourced agent for the 120 ATMs.

Bharath Bank Retail Branches Each of the 22 retails outlets are aware of the retention limits set upon them by BKC and are also notified by the main branch at Nariman Point that any excess cash above the retention limit should be returned to the main branch.

The Reserve Bank of India The RBI is known as the banker’s bank in India. This is so because the banks fulfill all their excess cash requirements by borrowing from the RBI. Most of the banks have a currency chest option wherein they are able to put in cash and withdraw it as and when required as part of its maintenance of its CRR. The RBI has already outsourced its coinage division to a player so that they can cut costs in this process.

SECTION III

THE CASE OF GLOBAL BANK

For Global Bank, to cater to its needs and demand of 33 ATMs and branches in Mumbai, cash is centrally distributed from its Bandra office. For the ATMs, there are three vendors which have been outsourced to replenish cash at the ATMs in Mumbai. These are: Brinks Arya (which looks after 22 ATMs), CMS Securities (which looks after 6 ATMs) and Writer’s Safeguard (which looks after 5 ATMs).

The maximum limit that Global Bank normally keeps in an ATM is `20 lakh, since each ATM is insured for an equivalent amount. This amount varies with each bank.

Brinks Arya has a vault whereby they maintain a certain cash balance, whereas, the other two vendors have accounts with Global Bank and they are allowed to go in for an overdraft (OD). This amount is settled by the end of the day by a reverse entry. The OD account is essential as banks cannot allow cash to lie idle with the outsourced agents. Vault cash account necessitates the replenishment of the cash from the outsourced agents to the ATMs in case of some major shortfall in cash. The intention of the entire ATM management is to ensure that there is no cash out situation at any point of time.

Information Flow in the Supply Chain—Role of IT Infrastructure

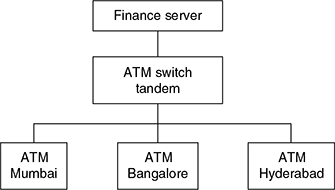

Global Bank has 33 ATMs in Mumbai city. They have changed over to switch technology from star technology. The server is located at Hyderabad and can handle 1000 ATMs at one go. All the ATMs are directly connected to the server (Base-24 systems, also called Tandom) and all the transactions across all the ATMs in the country are recorded out there. Every two hours, a report is generated to analyze the amount of cash withdrawal and idle cash lying in each of the ATMs.

Global Bank has a wide number of ATM networks across the country. The back office operation is maintained by the Finacle server which is the main database of all the customers of the bank. The ATM switch controls the functioning of all the ATMs and validates the operations of the customers by linking up with the financial server.

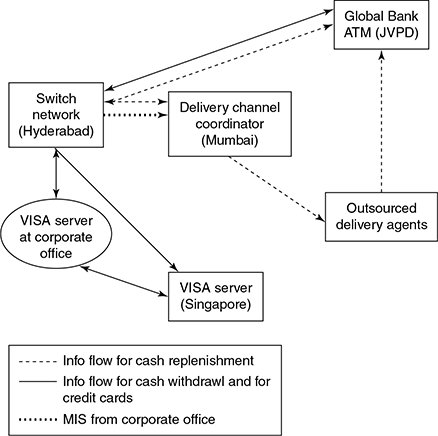

If there is a break in connectivity between the Finacle server and the ATM server, there is a cash memory that takes control of the operations of the ATMs. All transactions taking place at that point of time are recorded in the cash memory in a file called the positive balance file. Once the Finacle server is up-linked, the transactions are debited from the respective accounts of the customers.

Card Operation Centre There is a VISA server at the Global Bank corporate office at Hyderabad. This server is connected to the main VISA server at Singapore. Once a VISA card holder logs into any Global Bank ATM, the Global Bank server at Hyderabad passes on the link to the VISA server at the corporate office which transfers the information to the main server for validation of the transaction. Here, Global Bank has no direct role in controlling the operations and is just a part of the supply chain of information. This is a classic case of how two independent information hubs can collaborate to deliver better customer service to its customers.

FIGURE 20.2 ATM IT CHAIN OF GLOBAL BANK IN INDIA

For efficient functioning of the supply chain, the following factors have to be kept in mind in order to ensure minimum lead time and minimum breakdown time:

- The way vendors are integrated in the supply chain of the banks for maintenance management.

- Actual time required by the vendor to physically go to the branch/ATM to replenish the stock.

- Physical replenishment of items like rolls and stationary.

TEASE THE CONCEPT

How does the information flow place between ATMs and the VISA network?

The time lag between a breakdown of the ATM machine either due to a cash out situation or a technical snag and the information getting passed onto the delivery channel coordinator is about 20 minutes. Any problem with the ATMs gets captured first by the switch at Hyderabad and the information is then passed over to the respective individual in the city looking after the distribution system. The message is acted upon by informing the outsourced agency looking after that particular ATM to go and replenish the cash. This process takes another one hour. Hence, on an average, the lead time for cash replenishment or ATM machine maintenance takes about one and a half hours. Stationary/rolls are sent by the corporate office at Hyderabad to the head office at Mumbai and are then distributed to the respective ATMs through the outsourced agents like Brink’s Arya.

Payments and Receipts The inflow of cash to a bank takes place either through deposits of the customers, borrowings from the RBI or other commercial banks. The banks only go to the RBI when their expected outflows in a particular day exceed the available cash-on-hand on that day. The difficulty out here is that if the demand and supply for cash is not synchronized, it leads to a dead weight loss since there is an opportunity cost of holding back idle cash. Banks often face the situation whereby a customer wanting to withdraw a hefty amount does not turn up on that particular day leading to the bank holding more cash than what is permitted by the retention limit. Hence, the issue is to decide to what extent should the supply chain of a retail bank be efficient or should it be more responsive even if the total costs are not minimized.

FIGURE 20.3 INFORMATION FLOW FOR CASH REPLENISHMENT AND WITHDRAWAL IN GLOBAL BANK

Geographical Locations The geographical location of the branches and the ATMs are of vital importance in order to ensure either responsiveness of efficiency of the supply chain. While analyzing the ‘cash dispensed figures’ for the various ATM locations for Global Bank, certain locations show a significant amount of variability in the amount of cash dispensed. Depending on the high volume of transaction or high value of transaction, this could be attributed to the change in withdrawal pattern of the customers in the catchment area. The ATMs around shopping complex and malls have enormously large withdrawals in weekends and festival times.

Status of Accounts The asymmetry in the nature of accounts is one main factor that leads to wide fluctuations in the demand for/or supply of cash. The catchment area can necessarily have resident individuals, shopping malls or a large chunk of salaried people (in a typical downtown location). In such a scenario, the withdrawal of cash recurs on a fixed slot every month. Naturally, banks should take cognizance of this fact and accordingly plan the replenishment at these counters so as to avoid any excess cash holding situation.

SECTION IV

CASH DEMAND FORECASTING

There are four steps in any market forecast undertaken by an organization:

- Defining the market for the product/basket of products

- Dividing total industry demand into its main components

- Forecasting the drivers of demand in each segment and projecting how they are likely to change

- Conducting sensitivity analysis to understand the most critical assumptions and to gauge risks to the baseline forecast

The selection of a forecasting method depends on the following factors:

- The context of the forecast

- Relevance and availability of historical data

- Time period to be forecasted

- Degree of accuracy desirable

- Cost benefit or value of the forecast to the bank

- Time available for making the analysis

The following are the factors that are kept in mind while forecasting tools for demand management of cash for the branches as well as the ATMs.

- There is no stock-out situation in any of the branches as well as the ATMs.

- There is not much of idle cash lying since the opportunity cost of holding cash is quite high.

FIGURE 20.4 LINK BETWEEN THE CENTRAL SERVER, ATM AND VENDORS

- The cost of delivering cash to the branches and ATMs through the outsourced agents is minimized.

- The lead time to deliver cash is minimized.

- The architecture of the supply chain also becomes an endogenous variable since it has a direct relationship with the efficiency/responsiveness of the supply chain. The nature of information flows, the lead times in every step of the chain, the relationship with the outsourced agents and the geographical location of the branches and the ATMs all play an important factor in zeroing in on the most appropriate demand forecasting tool.

Both time series data as well as judgmental forecasting is used by all the retail banks to predict the demand for cash. Based on the demand forecasting tools, used by Global Bank and Bharath Bank, it was observed that location-wise daily data were captured to forecast demand for the next month.

Time Series Analysis of Cash Withdrawals from ATMs

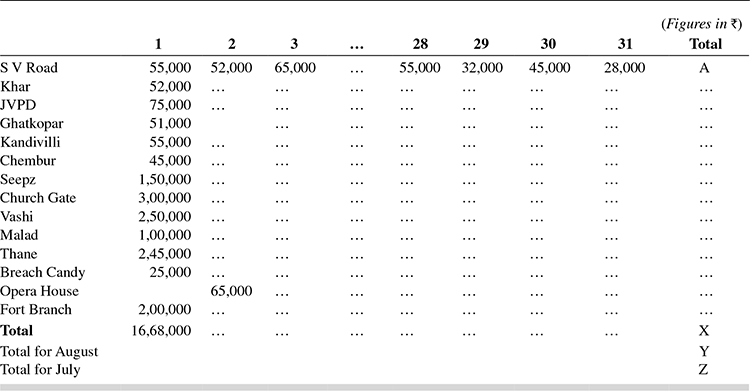

In most banks, demand is forecasted for a period of one month at a time. Therefore, the demand for the month of October gets forecasted on 30 September. Table 20.1 is a representative table highlighting the methodology of data calculations.

The data from Global Bank (for the period of July–August 2003) on the basis of the monthly cash dispensed from each of the ATMs aggregated over a month were collected.

TABLE 20.1 CASH WITHDRAWALS FROM ATMs OF GLOBAL BANK IN SEPETEMBER

The figure X shows the total withdrawal of cash that has taken place in the month of September. Similarly, such tables are constructed for the last three months. Y and Z show the corresponding totals for the months of July and August. Therefore, the demand planner will have the cash withdrawal data for the last three months before him and will be able to find out what has been the growth in the total cash outflow in this period of time. Using linear growth trends, one can initially predict that the total cash outflow for the month of October also grew at a similar rate and a total figure is arrived at. But this figure in itself is erroneous since only the trend is taken into consideration without paying heed to seasonality and judgmental factors. This growth which was calculated was the overall growth expected for the month of October. One can also take the site specific data and analyze the monthly growth based on the ATMs or the branches. The overall trend can be increasing, decreasing or stagnant.

Corrected: The present trend for month is with last year’s data to analyze the difference in the growth rates. This difference is then added into the forecasted trend. Once the trend is achieved, the list of festivities for the forecasted month is looked into. The dates are identified and then over and above the normal trend, the seasonality is factored in. (For example, 15 per cent to 18 per cent growth in outflow was factored in all major ATMs of Global Bank during Ganesh Puja).

Sales Trends and Other Factors

There are many salary accounts that banks have in their fold. These are those accounts where the salaries of the employees directly get credited to their respective accounts. From the day of the salary payment, within next four to five days, it has been observed that normally 50 per cent to 70 per cent of the money is withdrawn by the account holders. Therefore, if the salary accounts get credited by the bank on the first of every month, then for the next five days there has to be more cash that needs to be provided at the ATMs as well as the branches. To predict the outflow, a simple iteration is carried out whereby the number of salary accounts holders (say 500) is multiplied by the average salary that is deposited in their respective accounts (say `15,000). This would help the planner to arrive at a figure representing the expected demand for cash in the next few days exclusively because of the salary issue.

Judgmental factors in demand forecasting of cash by banks are stated as follows:

- Safety margin—Banks take into consideration the lead time that they will take to reach cash to the branches as well as the ATMs. The time to procure that cash from the RBI or from other branches is also factored in while deciding the amount of cash that needs to be sent out. Also, in those ATMs which are situated far off, cash is disbursed there sufficiently in order to cater to the demand for the next two days. These calculations are reached at after undertaking cost-benefit analysis at each ATM and branch. Even in case of weekends (Saturday and Sunday), many of the banks are closed and hence the money which is disbursed on Friday takes into account the expected demand in the weekends too. This type of system is primarily followed by smaller banks and in those ATMs where the volume of transactions is at a low level.

- Cash inflows that are expected to take place—Inflows from the RBI from their own branches, cash position maintenance as well as exogenous factors that effect the final decision of cash disbursal.

- ATMs are categorized by some of the banks depending on the volume of transaction that takes place from the outlets. Table 20.2 shows the method of categorization used by Global Bank to grade its ATMs.

TABLE 20.2 CATEGORY OF ATMs

Once the ATMs are categorized, a maximum cash retention limit is set on the basis of the following calculation shown in Table 20.3.

TABLE 20.3 SETTING LIMITS FOR EACH CATEGORY OF ATMs

The average volume of transaction is taken into consideration in each of the categories. This value is multiplied by a factor of 3. This factor 3 has been derived after taking the data of the maximum withdrawals that has taken place from each of the ATMs in the last three months and measuring the deviations, and then applying judgment to the factor in any unexpected swings in demand and other external variables.

CHAPTER SUMMARY

The findings and the observations based on the discussion in this chapter can be summarized below:

- In the following areas in Mumbai, significant variability in the average cash dispensed over a month was observed (Table 20.4) in the case of Global Bank.

It is worth noting that in the ATM counters where variability is high, it can lead to either a cash-out situation or an idle cash situation. If such wide variability is observed over a considerable period of time, then such changes in the demand pattern has to be immediately incorporated in the forecasting system.

- Maximum value withdrawn in the weekend is 1.5 to 2 times the normal withdrawal.

- If there is an increase in the number of transactions, it implies greater volume of transactions. On the contrary, an increase in the cash transactions implies a higher value of transaction. The cause of variability is either rooted in a higher volume of transactions or a higher value. The forecasting strategy of the bank can take this vital information into account to put in their judgmental part in the forecast If, for example, there is a higher volume of transaction noticed for a significant period in any ATM, it could be necessarily inferred that there has been an upsurge in the number of customers operating the ATM. This phenomenon is further analyzed by looking into the account numbers of the transactions from the Finacle server. The local addresses and the office addresses of the account holders can be looked into to verify whether the upsurge in demand is because of any significant change in the catchment area (which can be taken to be the area around, say, five kms. in the vicinity of the ATM). The chances should be noted as an endogenous variable in the regression model and has to be carried out in future so that such changes, once noticed can be factored into the model to avoid cash-out situations.

- On the other hand, if there is a high value of transaction noticed where the volume is not commensurately high, it can be inferred that the account holders are withdrawing more cash than they used to in the recent past. If this trend is witnessed for say three consecutive months, then there is surely a change in the withdrawal pattern of the customers. This needs to be further introspected to see if the base composition of the accounts operating the ATM is the same or has there been some change out there. If the composition happens to be the same, then the total volume of money that those specific accounts are having needs to be looked into. Finally, the amount of withdrawal as a percentage of the total holdings of the accounts can give the planner a better insight into the customer’s withdrawal pattern. If this change becomes a constant factor over a few periods, then the trend is considered to be a part of adaptive forecasting where level, trend and seasonality are updated after each demand observation.

From Table 20.4 it is evident that in Kandivali, the percentage change in number of transaction is significantly less than the percentage change in cash dispensed. This clearly indicates the high volume of transactions that have taken place from this ATM outlet. Similar inferences can be drawn for Sion and Malad. However, the Versova ATM shows that there is an increase in the number of transactions but a decrease in the value. If this trend persists, then it could be attributed to a change in withdrawal patterns at Versova ATMs. It is to be mentioned here that ATMs in Global Bank have currency denominations of `100 and `500 only. So for low value and high number of transactions, we could also study the flow of each of this currency from the ATMs. In scenarios such as this, the movement of the 100-rupee denomination might be significantly more than the 500-rupee currency so as to support a low value of transaction.

- Banks are highly overenthusiastic in setting retention limits of each of the counters, and so while setting up limits they have used a factor of 3, which arises due to an element of judgement. The intention is always to avoid any cash-out situation, but at times, it may lead to idle cash in the counters. No sophisticated forecasting tools are being used in any of the ATMs and retail branches; rather, banks take atleast two or three months to arrive at a figure for retention limits.

- The forecast horizon that is considered by a few banks is for a period of one month. This can be further subdivided into weekly forecasts so that better tracing of fluctuations is done leading to sound forecasting.

- The bankable consumer population in India is 300 million and the number of ATMs required for this population is supposedly more than two lakh. An ATM will have to be installed for every 1,489 cards issued. This seems to be an uphill task for private banks considering the expansion spree of the retails banks.

- On an average, an ATM costs around ₹8–14 lakh, while the annual maintenance varies between ₹12 and 20 lakh. An ATM is profitable if 50 – 100 transactions are carried per day on it. If the number of transaction are 260 – 270, the bank recovers its investment within a year. Bharath Bank claims that its ATMs execute over 300 transactions per day, hence justifying its expansion spree. But the moot point lies in the fact that the urban market is getting saturated in the days to come. In a crowded location in any of the metros, it would be prudent on the part of the bank to have a shared network, and given the number of transaction and the prevailing IT infrastructure they have, it is quite feasible.

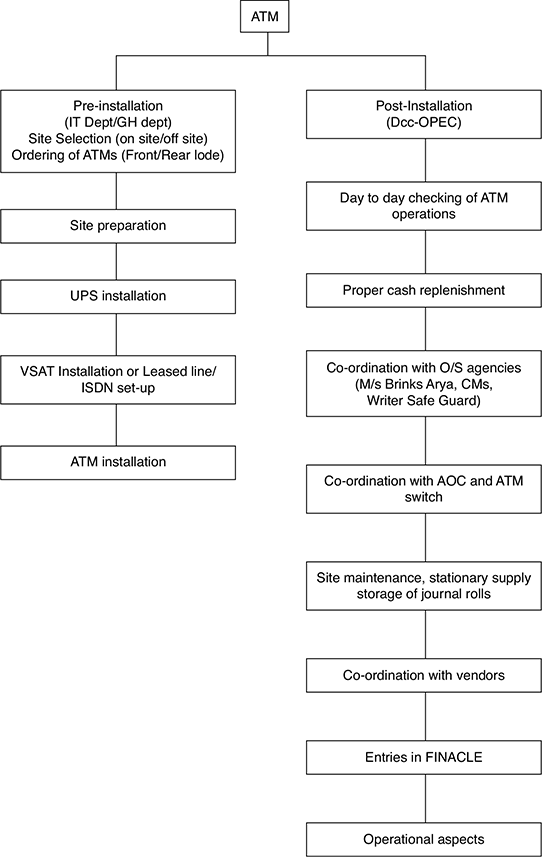

FIGURE 20.5 ATM—POST-AND PRE-INSTALLATION ACTIVITIES

- The flip side of this would be that a particular bank would loose out on its marketing edge when its network is shared, but on the other hand, it will gain free income from other banks for the use of its ATMs and hence recover its costs. Many banks have already entered into this kind of collaborative networking sharing as it gives them immediate access to a widespread market with minimal cost involved in infrastructure.

- The biggest problem that banks are facing today is deciding the optimal mix of denominations that they must keep in order to ensure that there is maximum customer satisfaction. All those banks which have harped strongly on CRM look forward to satisfying customers by supplying them with the denominations they look for. But in this process, at times, demand gets skewed for a particular denomination leading to short supply. This can still be managed by demanding the specific denominations from the RBI or from other commercial banks. However, the reverse case is the banker’s worst nightmare. For example, Bharath Bank once faced a situation whereby they are left with ₹2 crore in ₹10 denominations. Their predicament was such that they could not push this cash through the ATMs since the machines accepted only ₹500, ₹100 and ₹50 denominations. Another example is of HLL which holds an account with Bharath Bank. HLL gives only a day’s notice to the bank regarding the exact denominations it needs for paying off its members in its supply chain. At times, it so happens that the RBI also runs short of such denominations and hence has to look forward to get the specified denominations from its other branches. Therefore, it is not only forecasting what would be the level of demand but also the nature of demand that is important to understand.

TEST YOUR UNDERSTANDING

- How would you forecast the demand for cash in ATMs?

- What are the judgmental factors, you would take into account, while forecasting demand for cash in ATMs?

- Do you think that the complications would be more with the new system of shared ATM networks of banks like cash net and cash tree?

TOPICS FOR FURTHER DISCUSSION

- How does Bharath Bank manage the daily requirement in ATMs in Mumbai?

- Discuss the factors on which the retention limit for cash is set in branches and ATM of Bharath Bank.

- Analyse the case of cash management in ATMs based on the Global Bank case.

ANNEXURE 1

ATM—POST- AND PRE-INSTALLATION ACTIvITIES

Operational Aspects

- Daily end of day (EOD) reports from outsourced agencies

- Collection and processing of ATM deposit envelopes everyday at 6 p.m. at OPEC

- Disposing captured cards

- Checking and proper storing of journal rolls

- MIS to corporate office

- Electronic data capture (EDC) storing

- Informing respective agency at any time if there is any problem with the ATM

ATM Departments in Global Bank

AOC (ATM Operation Centre)

- Taking care of all the ATMs in India 24 hours

- Coordination of respective delivery channel coordinator

- Checking of ATM transactions and reconciliation

- MIS to Q and OPS department

CMC (Card Management Centre) Preparing ATM cards as per the application from the respective branches (FATM).

PMC (Pin Management Centre) Preparing PIN (Personal Identification Number) for all the ATM cards prepared by CMC.

COC (Card Operation Centre)

- Taking care of all the VISA transaction all over India in Global Bank ATMs

- Coordination with VISA—Bangalore and Singapore

- Maintenance and proper care of VISA server at corporate office

SElECT REFERENCES

- Patnaik, Santosh (2004). ‘Shared ATMs—The Way Foreward’, IBA Bulletin, December, pp. 24–27.

- Geetha, D (2005). “A Study on the Performance of ATM Services in Malaysia and Coimbatore City” in Justin Paul and S. Ganesan, Management: Strategies and Policies. Allied Publishers, New Delhi.

- Indian Institute of Banking and Finance (2005). General Bank Management. Delhi: MacMillan.

- Indian Banks Association (2004). ‘Technology as Competitive Edge’, IBA bulletin, March, special issue.

ENDNOTES

- This chapter has been co-authored by Dr Justin Paul, IIM Indore with Anirban Mukherjee, Arindya Roy and Dr Rakesh Singh.

- The names of the banks have been changed based on the request from the respective organizations.

- Author Dr Justin Paul is thankful to Anirban Mukherjee for collecting data and drafting the article that provided the preliminary source for this chapter.