5.1 DERIVATION OF A PDE FOR SHORT RATE MODELS

Assume the short rate rt (see Chapter 4) is modeled by an Itô process,

drt = μ(r, t)dt + σ>(r, t)dWt,

where we again use the notation r(T) = rt, Wt is a Brownian motion, and μ and σ> are functions to be defined later.

We are interested in the change dV of the value of an interest rate instrument V(rt, T) in an infinitesimally short time interval dt. Again, we utilize Itô’s Lemma and try to use the same kind of analysis that has been successful in deriving the Black-Scholes PDE (PS-PDE), where we got rid of the stochastic terms in the BS-PDE by Δ-hedging.

We set up a self-replicating portfolio π containing two interest rate instruments1 with different maturities T1 and T2 and corresponding values V1 and V2 (Hull, 2002). By applying the Itô Lemma for an infinitesimal change dπt = dV1 − ΔdV2, we obtain

Choosing![]() , the stochastic terms in the equation above can be eliminated. To avoid arbitrage, we have to use the risk-free rate,

, the stochastic terms in the equation above can be eliminated. To avoid arbitrage, we have to use the risk-free rate,

Rearranging equations (5.3)-(5.5) yields

This equality only holds when both sides of the equation solely depend on r and T and not on product specific quantities, thus

To model the individual properties of a particular instrument, specific terminal conditions, such as boundary conditions or interface conditions, have to be set. For instance, consider the simple case of a zero bond with a nominal of 1 and maturity T. To calculate the current price V0 under the assumption that r(0) = r0, one needs to solve the partial differential equation with the terminal condition

The partial differential equations obtained by using (one or more factor) short rate models can be interpreted as convection-diffusion-reaction equations (Anderson, Tannehill and Pletchter, 1997). This type of equation can, e.g., be found in heat transfer applications.2 The numerical solution using standard discretization methods entails severe problems, resulting in strong oscillations in the computed values. The drift term (first derivative) is chiefly responsible for these difficulties and forces us to use specifically developed methods with so-called upwind strategies (Quarteroni, Sacco and Saleri, 2002; LeVeque, 1992) in order to obtain a stable solution. Very roughly speaking, it is mandatory to “follow the direction of information flow”, and to use information only from those points where the information came from. In trinomial tree methods, the up-branching and down-branching takes into account the upwinding and leads to non-negative weights which correspond to stability.

5.2 UPWIND SCHEMES

Originating from the field of computational fluid dynamics, upwind schemes denote a class of numerical discretization methods for solving hyperbolic partial differential equations. In our case, they are used to cure the oscillations induced by using standard discretization techniques in convection dominated domains of combined diffusion-convection-reaction equations. Upwind schemes use an adaptive or solution-sensitive finite difference stencil to numerically simulate the direction of propagation of information in a flow field in a proper way.

Figure 5.1 Set of discrete points with indices {i - 1, i, i + 1}. The formulation of the first derivative by finite differences depends on the sign of a. Upwinding schemes consider the “flow”-direction of the information and only take the corresponding points (marked with dots) into account. The left hand figure shows the points used for a first order upwinding scheme for a> 0. The right hand figure shows the same for a < 0.

5.2.1 Model Equation

To illustrate the method, let us consider the hyperbolic linear advection equation

Discretizing the spatial computational domain yields a discrete set of grid points xi. The grid point with index i has only two neighboring points, xi-1 and xi+1. If a is positive, the left side is called upwind side and the right side is called downwind side3 (and vice versa if a is negative). Depending on the sign of a it is possible to construct finite difference schemes containing more points in the upwind direction. These schemes are therefore called upwind-biased or upwinding schemes.

First Order Upwind Scheme

A discretized version of (5.6) using a first order upwind scheme![]() and explicit time discretization is4

and explicit time discretization is4

The grid points of the space domain used for the formulation of the derivative with respect to the “flow”-direction of the information are displayed in Figure 5.1.

Severe numerical diffusion5 is introduced in the solution in spatial regions where large gradients exist. The scheme can be derived starting with the fact that the solution u of (5.6) is constant along characteristic curves,6 and therefore

Since in general xi − aΔT is not a grid point, the value of the solution at this point is approximated by a linear interpolation of the values at the neighboring grid points,

By inspection it is easy to see that the previous equation is equivalent to (5.7).

An Example

To illustrate the effect of upwinding schemes, we will solve (5.6) using the discretization in space and time given by (5.7). The computational domain (space X time) is given by

[0,3] × [0,1],

Let us specify the initial condition

![]()

the Dirichlet boundary condition

and the parameter a = 1.0. The number of discretization points for the spatial and the time dimensions are chosen to be nx = 301 and nt = 201. Therefore, as the Courant-Friedrichs-Lewy (CFL) condition

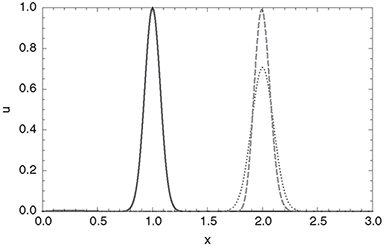

is satisfied, the explicit Euler time-stepping scheme yields stable results. Figure 5.2 shows u(x,t) for T = 0,0,25,0,5,0,75 and T = 1.0. The same problem calculated with the central difference quotient for approximating the first derivative (3.51) defined in Chapter 3 is shown in Figures 5.3 and 5.4. Using this discretization scheme, the solution blows up, and oscillations start to occur that destroy the solution. In the next subsection, we will show that using the central difference quotient in place of the upwinding scheme makes the propagation unconditionally unstable (Jacobson, 1999).

Some Theoretical Results

To examine the reason for the instability in the solution of (5.6) when using a central difference quotient, we start with

Figure 5.2 Solution of (5.6) for several points in time between T = 0 and T = 1.0. The analytical solution would be a peak with identical shape at T = 0, but rigidly shifted from 1.0 to 2.0 in x-direction. Obviously, an additional diffusive term leads to the dispersion of the solution.

Replacing ![]() ,

, ![]() and

and ![]() using the Taylor expansions,

using the Taylor expansions,

Figure 5.3 Solution of (5.6) for T = 0 to T = 0.5 using the second order central difference quotient (3.51) together with explicit time stepping.

Figure 5.4 Solution of (5.6) at T =1,0 using the second order central difference quotient defined in (3.51) together with explicit time stepping.

yields

Using7

we obtain

Numerical diffusion is introduced due to the discretization scheme used – the negative diffusion coefficient in the leading error term makes the scheme unconditionally unstable. Performing the same type of analysis for the upwinding scheme defined in (5.7) for a > 0, we end up with

Again using the identity (5.13) and defining

we obtain

Figure 5.5 Solution of (5.6) at T = 0.0 (solid) and T = 1.0 using the first order upwinding scheme (5.7) (dotted) and the Lax-Wendroff scheme (5.18) (dashed). Obviously, the diffusive behavior of the first order upwinding scheme is reduced by the anti-diffusion term introduced by the Lax-Wendroff scheme.

Therefore, the scheme is stable for C ≤ 1 and of order one.

Higher Order Upwinding Schemes

The Lax-Wendroff scheme (Quarteroni, Sacco and Saleri, 2002)8 can be derived using a Taylor expansion of ![]() (first equation in section 5.2.1). For the linear advection Equation (5.6), the Lax-Wendroff scheme yields

(first equation in section 5.2.1). For the linear advection Equation (5.6), the Lax-Wendroff scheme yields

The second term on the right-hand side can be interpreted as a diffusion term that stabilizes the method (remember that when using the central difference quotient for the discretization of the first derivative, we obtained an unconditionally unstable algorithm). Rewriting (5.21) for the case a > 0,

allows for a different interpretation. Now, the second term on the right hand side can be seen as an anti-diffusion term that reduces the diffusive behavior of the first order upwinding scheme described in (5.7). Figure 5.5 shows the effect of this anti-diffusion term.

Numerical experiments reveal an oscillatory behavior in the neighborhood of discontinuities, which can occur in finance due to discontinuous payoffs. This shows that in certain situations the anti-diffusive term of the Lax-Wendroff method is too high and therefore needs to be corrected. We will in the following derive such a correction using the total variation diminishing framework (TVD) (Harten, 1983).9, 10 We start with an attempt to control the anti-diffusive term by introducing suitable parameters Φi and Φi−1,

Setting

![]()

we obtain

with

The conditions (5.23) reduce to

A comparison of results obtained using the first order upwinding scheme, the Lax-Wendroff scheme and a TVD scheme is shown in Figure 5.6.

Figure 5.6 Solution of (5.6) at T = 0.0 (continuous black) and T =1.0 using the first order upwinding scheme (5.7) (dotted), the Lax-Wendroff scheme (5.18) (dashed) and the TVD scheme with the “superbee” limiter (continuous gray). The first order upwinding scheme is TVD but introduces severe numerical diffusion. The Lax-Wendroff scheme starts to develop oscillations when applied to non-smooth functions. The second order TVD scheme reduces the diffusion of the first order algorithm and does not show oscillations in the solution.

Condition (5.27) is satisfied for all C ∈ ]0; 1] if

Each setting of the form

leads to methods of order two.11 To obtain TVD methods, Φ(r) must lie between the “superbee” limiter by Roe (1986),

and the “min-mod” limiter

5.3 A PUTTABLE FIXED RATE BOND UNDER THE HULL-WHITE ONE FACTOR MODEL

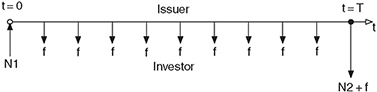

A fixed rate bond is a type of debt instrument bond with a fixed coupon rate. The coupon rate is payable at specified dates before bond maturity. A bond is puttable (also called retractable) if the holder of the bond has the right, but not the obligation, to demand early repayment of the principal at specified date(s) before the bond reaches the date of maturity. A bond is callable (also called redeemable) if the issuer of the bond is allowed to redeem the bond at specified date(s) before the bond reaches the date of maturity. In other words, on the call date(s), the issuer has the right, but not the obligation, to buy back the bond from the bond holders at a defined call price. Figure 5.7 shows the main properties of such an instrument.

Figure 5.7 The figure shows the time line plus the cashflows of a fixed rate bond. The time line is marked using an open arrow. All cashflows are marked using filled arrows. At time t = 0, the bond investor pays the face value of the bond to the bond issuer (open circle). Each coupon period, the issuer of the bond pays the coupon f to the investor. At the end of the contract period (t = T, marked with a filled black circle) the issuer of the bond pays the last coupon plus the face value to the bond investor. Possible call/put dates are fixed by the term sheet. Typically they coincide with the coupon dates, but this need not to be the case.

5.3.1 Bond Details

For the remainder of this section, we consider a bond with the following details as an example:

- Contract period of bond: T = 10y

- Coupon frequency: Annually

- Coupon rate: 5% fixed.

- Put dates: Annually starting one year after the issuing of the bond until one year before maturity.

5.3.2 Model Details

We valuate the bond under a one-factor Hull-White model (4.19). Model parameters are assumed to be piecewise constant functions of time (see Figure 5.8).

- We assume today’s spot rate r(0) = 0.03,

- The mean reversion speed parameter b(T) remains constant within [0, T] and b(T) = 0.1,

Figure 5.8 The figure shows model parameters as a function of time (in days). All time-dependent model parameters are assumed to be piecewise constant, changing their values only on model term dates.

- The long-term drift level Θ(t) is set to 0.05 in [0,T/2] and to 0.045 in [T/2; T] and therefore we have a(T) = Θ(T)b(T),12

- The volatility σ(T) = 0.005 is constant.

5.3.3 Numerical Method

Below, we summarize details of the algorithms used for the valuation of the bond:

- The theoretical domain for the spatial dimension r ∈] −∞; ∞[ is restricted to r ∈ [a, b], and Neumann boundary conditions of the form

are applied. The question of how to find appropriate cut off values a and b remains. Defining σmax = max(σ(t)),t ∈ [0, T] we choose

for the cut-off points. From experience we know that K ≈ 7 is a sufficiently good choice leading to cut off values a = −0.09 and b = 0.15 (for a detailed discussion of boundary conditions, see Chapter 6). The number of equidistantly spaced grid points is N, yielding a set of points {r0, r1 ... rN−1}.

- A finite difference discretization in the spatial dimension using second order finite difference formulae for the diffusion part and the simple upwinding scheme for the discretization of the convection term is used. Rewriting (5.4) in the form

and specifying the discrete operator L(j), where the index j denotes the time point at which the operator is evaluated, yields

- A second order semi-implicit time discretization using the Crank-Nicholson scheme is used. The time interval [0,10] (in years) is split into M − 1 time intervals (M points in time resulting in a set of time points TP that are measured in days starting from T = 013). Starting to derive an equation similar to (3.70),14

we obtain for Θ = 1/2

With the definition of the following matrices,

we obtain

and

The boundary conditions (5.32) can be incorporated by updating the first and the last row vector a0 and aN-1 of the coefficient matrix AHW as well as by setting the first and the last element of the right hand side vector BHWvj to 0. Using first order finite differences for the discretization of (5.32) yields

For convenience, we assume the time discretization to be consistent with the time line of the instrument (all relevant instrument dates, such as coupon dates and put dates as well as model term dates, are contained in the set of time points).

- Starting at T = T (V(T) is known by the payoff function at maturity), in each time step a system of linear equations,

must be solved15 by utilizing algorithms for tridiagonal matrices.

- If a coupon date is reached, the value on the grid point ri is updated according to

where f is the coupon rate of the fixed rate bond.

- If a put date is reached, the value on the grid point ri is updated according to

where p is the put rate. In order to calculate the value of the puttable as well as the non-puttable instrument, in each time step the system of equations is solved for two different right hand sides.

- If T = 0 is reached after M − 1 steps, the product value v is obtained by interpolation from v0.

5.3.4 An Algorithm in Pseudocode

V(i, T) ← FV+f ∀i ∈ {0, N −1}

for j = M − 2 → 0 do

Δt ← TP(j+1) − TP(j)

SOLVE (5.41)

if j == putdate then

v(i) ← MAX(v(i),p) ∀i ∈ {0, N −1}

end if

if j==coupondate then

v(i) ← v(i)+f ∀i ∈ {0, N − 1}

end if

if J==modeltermdate then

UPDATE AHW and BHW

end if

j ← j −1

end for

v ← INTERPOLATE(v0)

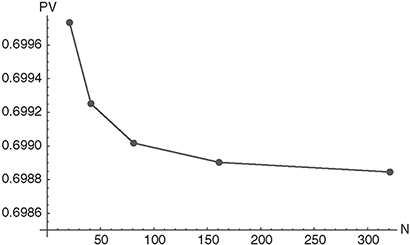

Figure 5.9 The figure shows the present value of a non-puttable zero bond with a maturity of 10 years and a nominal value of 1 as a function of discretization points N in the spatial dimension. For time discretization Δt =1 is used.

Figure 5.10 The figure shows the present value of a puttable (put rate p = 1.0) and a non-puttable fixed rate bond with a maturity of 10 years and a nominal value of 1 as a function of the coupon rate f.

5.3.5 Results

The number of days (equal to the number of intervals) until maturity is assumed to be 3650 with Δt = 1 (interval length). As a first step, the number of grid points needed for the spatial dimension is determined by calculating the value for a non-puttable zero bond (f = 0) with identical maturity using the model and numerical methods described above. From Figure 5.9, we see that N = 161 grid points are sufficient (the difference in the present value of the zero bond for N = 321 and N = 161 is smaller than one basis point).

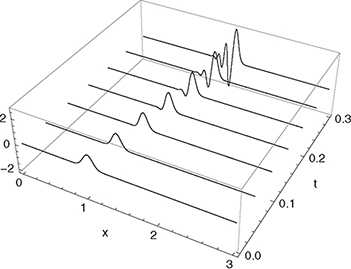

Figure 5.11 The figure shows the present value of a non-puttable fixed rate bond with f = 0.025 as a function of t and r.

Figure 5.12 The figure shows the present value of a puttable fixed rate bond with f = 0.025 and p = 1.0 as a function of t and r.

Next, we examine the present value of the puttable and the non-puttable bond as a function of the coupon rate f for a fixed put rate p = 1.0. As expected, in the limit of high coupon rates the present values for the puttable and the non-puttable product are equal, since no puts will take place, a fact that can also be seen in Figure 5.10. The bond value as a function of r and t for fixed f = 0.025 can be seen in Figures 5.11 (non-puttable) and 5.12 (puttable with p =1.0).

1In contrast to the Black-Scholes self-replicating portfolio, where the option and the underlying are tradable quantities, the interest rate (short rate) is a non-tradable quantity. To circumvent this problem, two different maturities are used to set up the portfolio.

2Transport phenomena such as heat transfer can be described by a generic scalar transport equation which in its general form reads

![]()

Here, f denotes the flux and g the source. Different physical processes like conduction (diffusion), convection and reaction can occur in heat transfer problems.

3 Think of a river and its flow direction – the water comes from the upwind side.

4 This scheme is also called Courant-Isaacson-Rees method.

5 When discretizing the continuous equations of motion by dividing time and space into a grid, the resulting discrete finite difference equations are in general more diffusive than the original differential equations. Therefore, the simulated system behaves differently from the system described by the continuous equation.

6 Characteristics are a key concept in the analysis of partial differential equations. In an equation such as (5.6), the characteristics describe the propagation direction of the wave.

7Assuming everything is smooth enough we change the order of differentiation and obtain

![]()

8The Lax-Wendroff method consists of two steps – a step for calculating auxiliary points for half step size in the spatial and in the time dimension, and a second step performing the time integration using a Leapfrog-like method. All spatial derivatives are performed using second order finite differences, therefore the scheme is second order in space and time.

9If it exists, the total variation of a function u mapping from [a, b] → r is given by

and a method is called total variation diminishing if

It can be shown, that a method of the form

where the coefficients An and Bn may depend on the approximate solutions

![]()

is TVD if the following criteria are fulfilled

10Intuitively, a system is said to be monotonicity preserving if no new local extrema can be created within the solution’s spatial domain as a function of time and if the value of a local minimum is non-decreasing, and the value of a local maximum is non-increasing as a function of time. Harten proved that a monotone scheme is TVD and on the other hand a TVD scheme is monotonicity preserving. Godunov’s theorem proves that only first order linear schemes preserve monotonicity and are therefore TVD. Higher order linear schemes, although more accurate for smooth solutions, are not TVD and tend to introduce spurious oscillations (wiggles) where discontinuities or shocks arise. To overcome these drawbacks, various high-resolution, nonlinear techniques have been developed, often using flux/slope limiters.

11To obtain second order methods, ![]() must be Lipschitz continuous.

must be Lipschitz continuous.

12 There is another commonly used notation for the general Hull-White model:

drt = b(t)(Θ(t) − rt)dt + σ(t)dWt.

In this notation, Θ(t) is the long-term drift level.

13Without loss of generality, we assume the starting point in time to be 0. Usually, a reference date is chosen and all relevant dates in a system are calculated relative to this reference date.

14In contrast to the classical heat equation, we are going backwards in time and are therefore using a backward finite difference quotient for the discretization of the time derivative.

15 Note that vj is the vector of instrument values of length N indexed by 0,1,... ,N −1 on the grid points. At a certain point in time j the instrument values at time point j −1 are unknown. These unknown values are the solution of the system of linear equations (5.41).