7. Implications for Sourcing/Procurement: Natural Resource Scarcity

At the beginning of 2012, government officials in Regina, Saskatchewan, were already looking forward to the year’s end, when construction on an important bridge spanning the Saskatchewan River would be finished. Their hopes were dashed shortly thereafter when, in late January, they announced the project would have to be delayed because of unexpected shortages in steel needed to craft the bridge’s girders. In North America, where the raw materials were to be procured, only certain mills could supply the specific type of steel needed to make the girders. Thus, the company charged with buying the steel to make the girders was unable to purchase the necessary quantities of raw materials from its North American suppliers, pushing back the estimated completion date to late 2013.1

This Canadian bridge will eventually become the final piece of an important project designed to address increasingly heavy traffic. This traffic includes important product distribution vehicles whose routes run from the province’s southern parts to its northern ones. On the surface, Saskatchewan needs the bridge for public safety reasons: Its predecessor was old, unsafe, and heavily traveled. However, from a broader economic perspective, its construction is part of the greatest infrastructure investment in the province’s history, enacted in response to the region’s significantly increasing population and economy. Unfortunately for Saskatchewan, scarcity of raw materials will put the bridge and its larger infrastructure implications on hold.

Understanding Resource Scarcity Today and Tomorrow

Around the world, the macrotrends we’ve described have already begun driving up the demand for natural resources and commodities needed to build infrastructure or produce more consumer and business products. In instances similar to the Saskatchewan bridge example, companies often can’t find the right quantities of raw materials needed to supply their manufacturing operations. We can cite many other worldwide steel and iron ore shortages similar to the ones in Canada. These include reports from South Africa and India, where several industries’ production has slowed because companies cannot meet local demand for critical steel supplies.2 Japan’s most notable shortages came in 2004, when an important Nissan Motor Co., Ltd., steel supplier surprised the automaker with its inability to meet purchase requests. This shortage came as a result of increased Chinese demand and actually triggered two shutdowns at three different Nissan manufacturing plants.3 One step upward in the steel supply chain, India’s largest steelmaker, JSW Steel, almost had to halt its manufacturing processes in late 2011 because it did not have the iron ore quantities needed to run blast furnaces.4 A shutdown would have had a significant effect on Indian steel prices. Yet steel isn’t the only critical metal facing shortage risks. In early 2012, Barclays Capital forecasted that aluminum would be in short supply by 2014,5 and a number of other important metals are forecasted to deplete in the coming decades. As with the issue of demand uncertainty, we tie future natural resource scarcity issues back to the global macrotrends. More consumers in more places having more buying power create more demand and subsequent shortages for metals such as steel and aluminum, as well as many other commodities required in companies’ production processes. Our examples of material shortages foreshadow that firms’ current assumptions about available resource quantities may not always hold true.

In other instances, quantities might be sufficient to meet demand, but available materials could and will fail to meet the quality standards that certain industrial processes require. For example, many grades of coal exist in various geological deposits around the world. One grade, commonly known as “coking” coal, is used primarily to manufacture steel. This grade of coal is in high demand due to the need for steel in the emerging Chinese and Indian economies. As a result, during recent years several foreign companies have sought to purchase mining companies in Australia that mine coking coal to stockpile the valuable deposits that will enable them to meet future global demand.6 However, the geopolitical risks of allowing sizable purchases of high-quality resources have led the Australian government to reconsider allowing foreign acquisitions of rare commodities for fear of compromising the national interests and forsaking future resource needs.

Resource quantity and quality issues are inextricably tied to geography. Lacking resource quantity or quality at a given location has, in many instances, forced companies to procure materials from remote locations and then transport them great distances to manufacturing sites. Business and economic history have seen many examples of common raw-materials transportation. Whether sourcing diamonds from Africa or salmon from Alaska, the global economy depends on unique combinations of supply chain tasks that link the successful acquisition and efficient transporting of raw materials from one location to another. Differences in resource availability, quality, and price have helped establish a thriving global trade network composed of multiple overlapping supply chains for natural resources and commodities. However, as critical commodities become more scarce, these problems will expand in scope, going from being more “local” to more “global” problems in the next 20 years. As fundamental as effective transportation and logistics methods may be, they will simply not be enough to overcome the constraints on procurement and sourcing that resource scarcity will enact on global supply chains in all instances.

In many cases, eternal hope springs from a resource’s renewability. Natural resources that are renewable can be regenerated over (relatively) short time periods. Of course, these issues are also tied to a critical macrotrend—environmental deterioration. Agricultural crops and timber are examples of renewable resources that can be re-created to meet future demand, but they are not immune to the effects of population growth, demand increases, and progressively polluted environments. The renewable resources that businesses need depend on clean air, soil, and water in the environment. If population, demand, and pollution continue to strain the environment, renewable resources will become less renewable. By losing the ability to regenerate, renewable resources that economies depend on are also in jeopardy of becoming scarce.

Resource scarcity also stems from geopolitical risks in the form of increases in raw-materials prices. Consequently, this increases companies’ economic risks. Price impacts on industrial supply chains are immediately evident if you examine the rare-earth metals market. Rare-earth metals are a group of 17 precious metals used to produce a variety of high-tech products. Two rare-earth metals currently affected by price pressures are europium and dysprosium, which are used today in solar cells, lasers, lighting, and magnets. From the early 2000s to 2011, these commodities’ prices shot up by over 300% thanks to export restrictions enacted by China.7 Emerging nations’ growing populations and economies are further exacerbating these metals’ scarcity and their corresponding prices. However, the price pressure is not confined to nonrenewable metals. Other renewable resources, such as beef, are under permanently exacerbating price and quantity constraints because people in emerging economies are consuming more meat. More common materials have also seen price increases. For example, from 2004 to 2008, aluminum and copper prices rose by nearly 100%, natural gas and industrial electricity prices tripled, and oil prices quadrupled. Increases in demand can have a ripple effect on resource scarcity levels and the corresponding worldwide prices of resources.8

It is important for sourcing and procurement professionals of the future to understand that a resource’s scarcity level changes continuously over time due to macrotrend-generated economic forces—in both positive and negative directions. Constant resource discoveries and technological advancements play a big role, as do changes in population, environment, geopolitics, and economic balance. For example, as described in Chapter 2, “Global Population Growth and Migration,” the shale oil and natural gas booms in North Dakota and other Western U.S. states were largely unexpected. Many of those deposits of oil are now expected to bring in amounts that are many times more than the initial projected quantities, which could depress prices for a decade or more. Changing competition and resource substitutions in product designs, stemming from human consumption in new or growing world markets, also have an enormous impact on demand levels and resource scarcity. These are the crux of supply uncertainty. Therefore, supply chain managers must learn to continuously reassess how natural resource scarcity levels are changing to fully understand the potential for sparse availability and how to deal with it.

Natural resource scarcity is a complex issue. Several resource attributes and forces determine the current scarcity level of a particular resource. Therefore, we need to take a more theoretical look at what’s driving this scarcity and how it affects supply chains. Why is scarcity a major issue for some resources and more easily overcome for others? Depending on your industry and your products’ (and services’) designs, companies and supply managers might find that their supply chains depend on multiple resources across a broad scarcity portfolio. This probably already impacts your company’s purchasing practices and logistics functions. However, increased scarcity could also create expensive product redesigns or increase the need for recycling in your own supply chain in the decades ahead. How can we explain what causes natural resource scarcities in the supply chain? And what can future sourcing, procurement, and supply managers do about it? The remainder of this chapter will try to answer these questions.

Natural Resource Attributes and Their Future Implications

Three primary attributes and a set of related forces that act on them can be used to describe a natural resource’s current status.9 We will focus on the three primary resource attributes: heterogeneity, renewability, and scarcity. Understanding a resource’s current state and how external dynamic forces are working to change it are critical for knowing how to manage resources in a changing world. First, we will take a look at heterogeneity.

Firms can gain competitive advantage by exploiting their resources. However, the exact quality and quantity of these resources determines the advantages that can be gained. Heterogeneity is the distinctness between apparently similar resources—the traits they possess that allow us to distinguish them from one another in terms of their exact physical and chemical properties. For example, it is easy to say that a farmer has 100 bushels of apples to sell. However, there are over 7,500 types of apples in the world, with different characteristics. So even if a supplier has 100 bushels of perfectly consumable apples, they may not be the type, color, size, or weight required to meet the demands of a specific customer, such as Kroger or Walmart. Apples vary by species, color, size, and origin, among other aspects. Dividing these 100 bushels into more “heterogeneous” and distinct types of apples directly and inversely reduces the quantity of each type and size available to sell. Hence, if a customer demands 50 bushels of the Golden Delicious variety, only 10 bushels may be of the proper variation. Even though the farmer has 100 bushels to sell, the maximum he can sell is 10, and the remaining 90 bushels may have to be sold elsewhere at a different price.

Consider a different, industrial example: Not all grades of diamonds are fit for use in making fine jewelry. Diamonds used to make wedding rings possess different qualities than those used in manufacturing cutting tools, despite their hardness and clarity similarities. Even if a company possesses “diamonds,” they may not be of the right quality to make the aforementioned products. Consider this: diamonds typically are classified based on specific criteria, including cut, color, clarity, and carat weight. Each category has a scale associated with it. For a diamond to receive a grade (such as industrial-versus jewelry-quality), it must score appropriately on these scales. Diamonds that do not pass the “Four C’s” test are more numerous, but they cannot be sold as jewelry. However, such quality diamonds are far from useless. Since diamonds are composed of some of the hardest substances on earth, they make excellent cutting tools in the manufacturing world. Disfigured or discolored diamonds often make their way to this industry after scoring poorly on the Four C’s test. The rarest jewelry-grade diamonds can cost $60,000 and more.10 Prices typically are lower for industrial-grade diamonds. A glance at commodity purchasing website Alibaba.com11 showed “saw grade diamonds” for sale in 200g bulk at $.70 to $1.30 per gram when we logged in during late 2011.

Therefore, heterogeneity as a commodity attribute describes the degree of distinctly different natural resource types that are possible. From the supply manager’s perspective, it contributes greatly to commodity scarcity. High levels of heterogeneity for a resource such as apples or diamonds also indicate that many different types of the resources are possible and currently available to be utilized. Since consumer and industrial products generally require a wide variety of heterogeneous resources with different attributes, worldwide demand depends on a sufficient supply of heterogeneous resources. Unfortunately, consumption over time has sometimes used up the highest-quality and most available nonrenewable resources. In fact, consumption has often created instances where some resource grades are no longer available, so levels of heterogeneity are lower. Additionally, pollution and resource degradation have caused many plant and animal species to go extinct. They also have led to lower levels of heterogeneity of renewable natural-resource supplies needed to meet the wide array of ever-increasing demands.

Understanding the exact specifications of the natural resources needed in products and their available supply quantities is critical to supply managers’ understanding and management of heterogeneity in the future. More and more resources are becoming scarce and/or exhausted. Assuming that apparently plentiful resources exist within broad homogeneous groups (diamonds, apples, coal) that are globally available is a dangerous way for a supply manager to speculate. Such thinking can cause a firm to be blindsided by growing scarcity of a distinct heterogeneous resource type. Instead, supply managers need to understand a resource’s level of heterogeneity and how it corresponds to specific resource demands.

Renewability is the second primary attribute affecting a resource’s current status. This attribute describes a resource’s ability to regenerate new quantities in the future. Some “renewable” resources can be regenerated over relatively short periods of time. Crops that supply the world’s food chains are regenerated and harvested once or more in a single year. In the case of forests, it may take several years or decades for a resource to be restored and ready for a new cycle of consumption. For fisheries and other living systems, renewability may depend on the resource’s reproduction versus harvest rates, as well as the underlying environment’s health. As such, these renewable resources depend on the continued availability of accessibly clean amenities such as water, air, soil, and even ecological systems. For example, fruit crops depend on honeybees for pollination, and fisheries depend on plankton for food. Therefore, just as an isolated supply chain disruption such as a hurricane can affect a company’s product supply chain, so can an environmental or ecosystem disturbance disrupt the supply chain for a renewable natural resource. Additionally, economists and ecologists have established that as population, consumption, and pollution increase, renewable resources can become less renewable. By losing the ability to regenerate, renewable resources that economies depend on are in jeopardy of becoming scarce.

Other natural resources are, for all practical purposes, “nonrenewable,” such as the metals, minerals, and petroleum currently used in large quantities in industry around the world. These nonrenewable resources have very long natural creation periods. As humans consume more and more of them, they will steadily and increasingly become more rare. Although better technology helps us discover new deposits of nonrenewable resources, the planet contains a finite quantity of many resources to exploit. Although many of us may never live to see the complete “exhaustion” of a natural resource, economic activity continually decreases resource supplies and forces us to use quantities of lower-quality resources. This usage is more costly, requires improvements in technology, and can create more pollution, which then harms the environment and other natural resources.

The third attribute is scarcity—the primary focus of this chapter. Scarcity of a resource is the balance of physical supply and demand of the resource in a given location. Following scarcity research in several academic fields, natural resources can be described as scarce or available in a particular location depending on whether demand exceeds supply (scarcity) or supply exceeds demand (availability). Therefore, in a geographic context, scarcity can be either a global or local phenomenon. For example, metals such as gallium, indium, lead, platinum, and silver are becoming more globally scarce—they are predicted to be in short worldwide supply in the future. This fact has the potential to impact product designs for capacitors, solar cells, lasers, magnets, and the high-tech consumer products they help comprise.

Other resources may simply be locally scarce. Even though Australia is an extremely resource-abundant nation, it does not possess enough nickel deposits to meet all of its local demand. Consequently, it imports large quantities of nickel from the nearby island of New Caledonia (Fr.). Local scarcity is also prevalent with renewable resources like beef, salmon, and timber. These are not necessarily globally hard to find, but they are locally scarce. They must be transported long distances to meet local demand in places they cannot be found. Location is a key aspect of resource scarcity. Managers must determine the local and global aspects of scarcity for resources they possess and figure out how changes in scarcity might impact future operations. Additionally, it is important for managers to understand that the related attributes of renewability and heterogeneity also affect the measurement of scarcity (demand-versus-supply balance) for a resource and help determine an overall resource status.

Scarcity of resources like rare-earth metals, oil, and natural gas can bloat costs and prices for businesses in the coming decades. Although such increases show the power that scarcity can have over business, supply managers must not overreact to short-term changes that could be due to simple market fluctuations. Instead, we need to understand the long-term forces that constantly affect a natural resource’s availability and price. By analyzing the three attributes of a resource now, managers can assess how that resource’s current status might change and can take action to ensure that their organization is not crippled by future scarcity.

The Seven Forces Driving Resource Scarcity

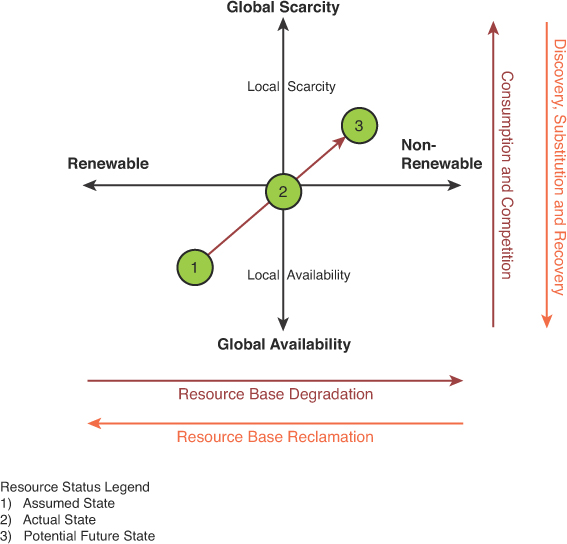

Researchers across several sciences have identified seven macro-level forces that change a specific heterogeneous resource’s scarcity level: discovery, substitution, recovery, resource base reclamation, consumption, resource base degradation, and competition.

As shown in Figure 7.1, four of these forces make resources more abundant, and the other three deplete them. Balancing these forces helps us ensure a specific resource’s global availability and keeps it from losing economic value due to exceedingly high prices. However, this balance may not always be possible. As has happened so often in the past, supply managers may make false assumptions about a resource’s homogeneity and availability, thereby failing to understand how scarce a particular resource really is. That is why we, as business managers, must understand how the seven forces act upon the world’s natural resources.

Figure 7.1. Resource scarcity dynamics12

Discovery of new resources has always been paramount to countering resource scarcity. As resource prices increase, so do the incentives to explore the Earth and create new technologies to find either additional volumes or new, less-scarce replacements. In 2011, over 300 activities were related to exploring the planet for rare-earth metals. This includes major efforts in California to reopen the United States’ only rare-earth mine, which at the time was owned by Molycorp Inc.13

A major part of new-resource discovery is the related technological improvements developed to extract nonrenewable materials or harvest renewable ones. Recent efforts by major oil companies to find new resources depend on cutting-edge technologies to exploit shale gas and oil sand deposits. These deposits were previously believed to be far too expensive to extract. But with horizontal drilling and hydraulic fracturing technologies (fracking, described in Chapter 2), the northern and western areas of the United States, as well as significant portions of Australia and Canada, are at the forefront of a new natural gas and oil boom. Critics argue that the increased impact of these discoveries comes at a much higher ecological price and that the companies using these new technologies may not have fully considered the long-term environmental and social costs. But even as the debate over fracking rages, its use is becoming more widespread.

When a resource’s availability erodes and price increases, the economic force known as substitution may take over. Business history offers many classic substitution examples. When whalers made their prey an endangered animal in the 1850s, whale oil prices soared. With whale oil no longer an economic possibility, kerosene soon became the standard for lantern fuel. Similarly, the lack of timber and wood for industrial purposes has often resulted in companies using substitute materials such as iron, steel, glass, or plastics to build their products. When engineers design new products, they search for substitute materials with similar physical characteristics that are not quite as expensive.14

Substitution has its limits, though. For example, the “tin whiskers” anomaly has made it difficult to replace lead solders with tin in electronics. The tin functions as a solder, eliminating the need for lead, but it creates electrical malfunctions as microscopic “whiskers” disrupt the robust way in which microelectronic designs operate. Few periodic table elements might serve as viable substitutes. Even if scientists could find a suitable replacement, each element comes with its own unique problems and benefits. As in a game of chess, design engineers find themselves strategically moving from one element to another to avoid resource scarcity and achieve desired product characteristics, but they can make only so many substitutions. Therefore, like discovery, substitution often depends on improved technology, where potential risks and limitations almost always come with the territory.

Next, recovering, or recycling, natural resources can increase their supply and hence lessen their scarcity at local or even global levels. In the United States, a large portion of aluminum (30%), lead (63%), and titanium (50%) needed by their respective industries are supplied by recycled sources each year.15 Products often are recycled for purposes other than just countering scarcity. For example, environmentally conscious policies in states like California and Oregon have compelled citizens to recycle. Some companies have started recycling efforts that focus on packaging materials (containers, cans, boxes) that can easily be reused. Others help consumers dispose of products that are obsolete or at the end of their life cycle so that they can be reused or recycled.

In some instances, these efforts are not always successful. In 2011 some cities fell far short of California’s recycling goals, and some major companies were reported as not fully utilizing their recycling facilities. Given the increasing pressures of macrotrends on both the world and its supply chains, we expect this to change in the future. Scarcity, pollution concerns, and increased discovery/technology costs will make recycling natural resources more of a necessity than a marketing function. Managers must be on the lookout for ways to build closed loop supply chains to both recover value from obsolete products and design new ones so that they are easily recycled. When scarcity starts to take its toll, recovering reusable materials will be extremely important.

Similar to resource recovery, reclaiming the environment’s air, water, and soil can mitigate, and possibly even reverse, the way in which resources are losing their renewability. Mining companies like Rio Tinto PLC have worked to reclaim and clean their mining locations by returning soil and groundwater to its original state, where it can be used for agricultural purposes. Much to the horror of many activists, governments, and a growing number of the world’s population, pollution continues to spread in some regions of the world. Business still has a long way to go in terms of harnessing resource reclamation without also polluting the environment. This is probably due to the short-term inability to build profitable justification for such environmentally friendly activities, which do not always please shareholders.

As resource scarcity intensifies, supply managers should try to find ways to work with industry groups and government to reclaim damaged air, soil, and water to regain the renewability of resources. This concept should be obvious for companies like Georgia Pacific and ConAgra, which depend on timber and crops. They cannot afford to pollute the soil and water and expect their renewable resource supplies to remain sustainable. All industries should start to look into resource reclamation as a means to reduce the scarcity sure to strike them in the future.

The forces just described counter scarcity, but other forces amplify it. Increased consumption (as driven by our focal macrotrends) is a major worldwide concern and one of the most stressful forces acting upon natural resources. In economic and industrial activity, humans typically extract the highest-quality and most abundant resources first. Therefore, over time the highest-quality and easiest-to-access resources have disappeared due to past consumption. This helps explain why discovering new resources gets more difficult and more expensive and why products using those resources see continuous price increases. Some economists and environmental scientists are beginning to argue that we will probably never truly exhaust all of the world’s oil. This is because global societies would be unable to afford the environmental impact or technological cost necessary to do so. Some economists believe that because the earth’s environmental sinks are starting to fill up with air, water, and soil pollution, that trying to extract quantities of a resource (such as oil) to the point of exhaustion will create levels of pollution that the planet cannot bear.16

As we pointed out earlier, the planet’s population will probably stabilize, and may even begin to contract, between the years 2030 and 2050. Until then, many of Earth’s new citizens will seek more and more industrial and commercial products that will consume our natural resources. Consumption has the potential to change and disrupt the balance of resource scarcity, as shown in Figure 7.1, in a truly daunting way. Without long-term approaches and strategies to counter consumption’s growing effects, many companies will face a serious scarcity of resources that today are assumed to be globally available.

The degradation of underlying resource “bases” is making some renewable resources nonrenewable and some common ones more scarce. Economists and ecologists have observed this trend for many years. It is highly correlated with greater levels of consumption. For instance, environmental damage is threatening resource renewability around the globe. In China, some major rivers have become so polluted that even livestock cannot drink from them.17 Similarly, overfishing and pollution threaten seafood sources, and overharvesting and ground pollution increase the scarcity levels of agricultural resources. Even though people and companies have started reclamation efforts, degradation rates are far exceeding reclamation rates. Degradation is hundreds of years in the making, and much of the damage has already been done thanks to previous industrial and commercial activity.

Although competition among firms is generally best for the consumer because it reduces prices in the short term, it also augments scarcity, which exacerbates prices in the longer term. With limited materials to go around, there is no guarantee that your firm will have access to them. If a direct competitor or a firm in another industry needs a natural resource and has secured large quantities of it for future use, it may be more difficult for your firm to gain access to it. Firms from countries all around the world are already “buying up,” or hedging, numerous scarce resources because of anticipated future shortages. These hedging expenditures have been estimated at over $1 billion per day. Some companies are also hedging by vertical integration: They are buying up mining companies. Speculators are acquiring waste-collection companies to gain access to waste streams that will someday become reclamation sources.

Companies and managers need to understand that long-term availability of natural resources may be limited because firms and individuals are competitively buying up resources. Business competition is generally viewed as a downstream, market-side phenomenon in commercial supply chains. However, growing competition among major firms upstream in the supply chain is expected to increase as firms seek to secure scarce resources needed to meet future demand. We are entering a business phase in which Demand-Supply Integration (DSI) will be not only important to world-class companies, but also a trait needed for any business’s long-term corporate survival.

Resource scarcity has three primary attributes and seven primary forces that change its level over time. It is evident that prevailing economic macrotrends, such as population growth and economic leveling in emerging parts of the world (Asia and Africa), will tip the DSI balance for many resources toward higher levels of local, and even global, scarcity. This translates into much higher costs and may even mean an insufficient supply of natural resources to meet rapidly growing, industrial product demand.

Scarcity Strategies for the Future Procurement/Supply Manager

As supply managers start to make strategic choices about how to match demand with supply in the coming decades, they need to be careful not to make incorrect assumptions about a resource’s scarcity status. Companies may make an assumption about the status of a resource that doesn’t match its actual state (see states 1 and 2 in Figure 7.1). For example, a person may assume that the demand for a resource such as coal is very homogeneous and can be met with any type of supply. However, he may later find that only a specific grade of coal can be used and that the actual state of scarcity is much worse than he thought. Additionally, supply managers who do not analyze how forces are changing the actual state may not realize that they are headed toward a potential scarcity situation in the future (see state 3 in Figure 7.1). As you read in the preface, Coca-Cola may have made bad assumptions about freshwater availability for its bottling plant in India.

Similarly, designing a product such that a scarce natural resource is needed in its production, and then later finding out that there isn’t enough of it to go around, could dramatically impact the product’s (or company’s) viability. Throwing money at the problem is not always the solution. A company may stockpile a resource in anticipation of growing scarcity and then have its investment undercut by the future discovery of a new major deposit. It is important to understand that it is possible to move in any direction shown in Figure 7.1, depending on how the seven forces are attempting to counteract and balance each other. Therefore, to prevent mistakes like this and to mitigate scarcity risks, firms need to collect better information on potential scarcity for their resources and build better processes for strategic decisions concerning resource scarcity.

Improved technology, resource discovery, and resource substitution may have the potential to temporarily mitigate short-term price fluctuations caused by scarcity. However, economists and energy scientists alike admit that there may be environmental, geological, and technological limits on alleviating scarcity in the long run. Many firms are already starting to feel the growing problem of scarcity and are bracing for tougher times ahead. Consulting firm Pricewaterhouse-Coopers surveyed over 60 industrial firms in December 2011. It found that over 50% of companies are struggling with scarcity of their key metal sources and that 75% of them anticipate the problems will get worse in just the next five years.18 Additionally, many design engineers are beginning to document the difficulties associated with designing and manufacturing new products with scarce availability of important metals. Some metals are projected to have a 10-to-20-year global supply at current consumption rates. But this supply could be cut to fewer than 10 years if the rest of the world increases its consumption to even half of what the United States is consuming. With an insufficient supply of metals, how will we continue making the batteries, magnets, lasers, solar cells, and other components needed in future products? Or, more importantly, how much will these important subcomponents cost your company—and the world as a whole?

Sourcing and Procurement Responses to Resource Scarcity Through 2030

This chapter has described the general problem of resource scarcity, mapped the playing field (by articulating resource attributes and forces), and described some of the growing risks anticipated in the next 25 years. Now we offer three general recommendations for managing future supply in a world of resource scarcity:

• Supply managers need to understand what resources (in terms of quality and quantity) are used in their key products’ designs and how scarce those resources are. We suggest that managers must map these products’ supply chains all the way back to the raw-material level to uncover hidden supply risks. Resource scarcity can affect the key GSCF supply chain processes of product development, supplier relationship management, and manufacturing flow management. Therefore, companies should work with supply chain partners in these processes to collect information and uncover hidden risks.

• Because scarcity is a dynamic issue, the sourcing functions of current and future businesses should consider investing in research activities to monitor scarcity changes caused by the seven forces. This includes monitoring changes and forecasts for consumption and competition for key resource supply. Global awareness and anticipating changing resource statuses will help supply managers identify demand and supply threats and also help them create opportunities for their companies. Instead of being caught off-guard by unanticipated scarcity crises, supply chain managers in proactive companies can differentiate themselves and create competitive advantage by getting ahead of scarcity trends.

• As soon as supply managers fully understand the resource scarcity dynamics that affect their firms, they should capitalize on opportunities by building comprehensive supply strategies that capture and leverage the described forces to get ahead of the competition. Firms should work with their supply chain partners to build long-term strategies for responding to growing scarcity levels by designing products and basing their technology changes on resources that will be available. Additionally, managers should leverage supply chain designs and build logistics approaches to ensure that products remain sustainable throughout their life cycle.

These three ideas are not new to world-class companies like GE, Unilever, and Kimberly-Clark. They have already faced challenges created by resource scarcity and have taken significant steps to do something about it. They have joined global groups, such as the World Business Council for Sustainable Development, to monitor issues like water scarcity and learn how these can affect their products. They are building long-term and multifaceted strategies to mitigate resource scarcity in the future. They understand what’s coming, and they’re doing something about it.

Let’s look at GE’s method for identifying scarcity risks as an example. In the production of its major aircraft engines, GE has recognized that many important metals are becoming scarce. This scarcity has affected GE’s costs and is having a significant impact on how the company designs future engines. To make the best decisions about using scarce metals and to mitigate the impacts of scarcity on current engine product lines, GE has developed a multifaceted risk management approach.19 GE uses approximately 70 of the first 82 elements in the periodic table in its manufacturing operations. However, since detailed analysis of all 70 of these elements seemed infeasible, the company ranked the annual purchase value of the elements from highest to lowest in a Pareto ranking. Doing so helped GE identify where the biggest scarcity impacts could occur. Using this approach, GE narrowed the list to 24 elements with a large-enough footprint in the company to have a significant impact on operations if supply became restricted. Next, it narrowed this field to 11 metals that were subject to recent price variability and instability. Then it conducted detailed research on the 11 elements and ranked them in a criticality matrix. On one axis of this matrix, elements were ranked from very high risk to very low risk based on the potential impact to the company. This impact was measured with four subfactors: the ability to substitute the element, the percentage of world supply used by the company, the revenue that would be lost if the element became unavailable, and the ability to pass on price increases to final customers. On the second axis of the matrix, GE ranked the 11 elements from very high risk to very low risk based on the potential supply and price risks. Subcategories in this category included abundance of the element in the Earth’s crust, political risk, demand increase risk, whether the element is a by-product of another element, price volatility, and the ability to substitute. Overall risk scores for each of the two axes were determined by summing the risk rankings in each subcategory, and then the final position of each element was plotted on an x,y matrix. The results helped identify which elements were at greatest risk of being impacted by scarcity, and also how that would translate into an impact on GE. Overall, GE identified that the metal rhenium, used in its aircraft engines, was not suffering from scarcity but had the potential to have a major impact on the company. This allowed the company to take detailed actions, which we will describe in Chapter 11, “Mitigating Demand-Driven Imbalance.” Unlike our opening example of the steel shortage in Canada, GE has built a formal and proactive process for identifying natural resource scarcity risks in its products and for doing something about it before it impacts the company. Managers should consider whether they have similar processes in place, or whether they will find out about the impacts of scarcity after it is too late and major disruptions affect their operations.

So what’s the bottom line? Growing resource scarcity will play a major role in business over the next 25 years. In response, supply managers will have to avoid short-term thinking and invest more time and money in more proactive and long-term risk management strategies to avoid the scarcity pitfalls.