Chapter 6: Getting Paid for Your Mobile Marketing Efforts

In This Chapter

![]() Making money through the mobile channel

Making money through the mobile channel

![]() Distinguishing among mobile payment models

Distinguishing among mobile payment models

![]() Cashing in on carrier billing relationships

Cashing in on carrier billing relationships

![]() Building out your own commercial presence

Building out your own commercial presence

The mobile channel is unique. It is a personal, location- and time- independent, interactive marketing medium that can be used to enable commerce. You can use it to process transactions and as a storefront, as well as a tool to interact with and turn your once-inert print, television, radio, outdoor, advertising, and related marketing media into immediate retail engagement mediums. In 2012, eBay estimates that between its auction site and PayPal, it will process over $8 billion in transactions through mobile. Worldwide, mobile commerce transactions are expected to exceed $1 trillion by 2015, up from $24 billion in 2011.

This chapter reviews the many ways you can leverage mobile as a medium of commerce. It explains how you can commercialize physical and virtual goods through and with mobile, including music, movies, tickets, parking, televisions, and clothes for your virtual avatar within a game. And most importantly, it explains the different ways to consider mobile commerce and the various payment methods you can use to make money with mobile.

Methods of Monetizing the Mobile Channel

When considering mobile commerce, it is important to recognize that the term mobile commerce, or mCommerce, can be confusing. It’s like trying to measure sunlight; depending on the tool used for measurement, it will either be perceived as a particle or a waveform. Depending on how you look at mobile commerce, you’ll either perceive it one of two ways:

• Receiving payment via mobile is the activity of processing a transaction through the mobile device, that is, exchanging money or stored value (such as a rebate or prepaid card) via one of the mobile paths, including SMS, applications, mobile web, and voice. See Chapter 1 of this minibook for more details on all the mobile paths.

• Mobile-influenced transaction is the use of the mobile device to engage people and influence their awareness, interest, and relationship with your business to eventually encourage them to make a purchase, whether through your brick-and-mortar store or your website. For example, people may use the mobile phone to search for a local store, check for discounts, or compare products but complete their transaction at your store’s traditionally manned or self-service checkout counter. They may even just go home and buy the product from your website and have it shipped.

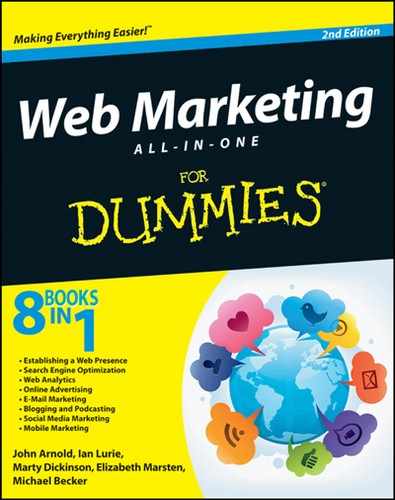

Figure 6-1 illustrates this idea, putting mobile commerce as a unique process/event within the context of mobile marketing.

Figure 6-1: Mobile commerce within the context of mobile marketing.

Understanding mobile payments

When thinking about taking a payment for a transaction through mobile, it is important to consider what kind of goods and services you’re looking to sell and to understand the flow of money between the consumer and you.

In the mobile world, people tend to consider two billing models:

• Direct carrier: In this model, the charges for items being bought are billed directly to the consumer’s mobile carrier bill, and the consumer pays for the services each month when he pays his phone bill.

Two methods exist for direct-to-carrier billing:

• Premium SMS: The practice of using text messaging as a billing method. See the section “Making Money through Premium Text Messaging,” later in this chapter.

• Internet-based carrier-billing models: Billing solution providers supply the developer of your mobile Internet or applications with software to include in your mobile websites and applications (see Chapter 5 of this minibook) to support carrier billing.

Leading carrier-billing solution providers include Zong (www. zong.com), BilltoMobile (www.billtomobile.com), BOKU (www.boku.com), Payfone (www.payfone.com), and OpenMarket (www.openmarket.com).

• Internet-based: In this model, you manage the billing in the cloud (online servers) and through your mobile payment solutions providers with the charge going directly to the carrier bill as opposed to your credit card. See the section “Selling Your Content and Services via Mobile,” later in this chapter.

Offering Your Content through a Carrier’s Portal

With the growth of smartphones and the ability to engage a consumer directly, it may come as a surprise that the mobile carrier itself is still an incredibly valuable channel to reach your audience. Every mobile carrier offers a branded portal on the mobile phone. This portal features content and services created by the carrier and its partners. You too can offer content through a carrier portal. To offer your content and services for sale through a carrier’s portal and ensure that you ultimately get paid, you must follow one or more of the paths described in the following sections.

Mobile carriers today typically are not enabling the physical goods and services through their portals. It is one thing to take on the sale of a ringtone, image, or movie. It is a completely different thing to take on the liability of physical goods.

Mobile carriers today typically are not enabling the physical goods and services through their portals. It is one thing to take on the sale of a ringtone, image, or movie. It is a completely different thing to take on the liability of physical goods.

Developing a direct relationship

Many companies establish a direct relationship with each individual carrier for the purposes of promoting content and services directly on the carrier’s portal. The deals that you can strike can vary greatly, but here are some common ways to develop revenue opportunities with a carrier:

• The carrier gives you a lump-sum payment for access to your content for a certain period.

• The carrier provides you minimum sales guarantees.

• You and the carrier enter into a revenue-sharing relationship in which you share the revenue (often not equally).

Direct carrier relationships take time to develop and negotiate — often 12 to 18 months or more — and this time frame assumes that you already have a head start and generally know who to talk to.

Direct carrier relationships take time to develop and negotiate — often 12 to 18 months or more — and this time frame assumes that you already have a head start and generally know who to talk to.

Entering into a channel relationship

Many carriers offer developer and content-channel relationship portals that you can sign up for on the Internet. The channel relationship business model differs from the direct carrier relationship discussed in the preceding section in that you’re not negotiating a direct deal. Instead, with a channel relationship, you get access to the carrier portal, business terms that are easy to adopt and employ, royalty payments for the sale of your content, access to the carrier’s marketing education materials, and more. Table 6-1 lists various carrier content and developer programs.

Table 6-1 Carrier Developer Programs

|

Name of Carrier |

Contact Information |

|

Sprint |

|

|

Verizon |

|

|

T-Mobile |

|

|

AT&T Wireless |

Here’s how to get started with channel relationships:

1. Go to the carrier’s website, and sign up for a standard third-party service program.

2. Have your content or service certified.

This step is important, because you must be certified before the carrier puts your content on its portal. Every carrier’s certification process is different, based on the type of content or service you’re offering. You’ll need to review the details of the process on the carrier’s website.

3. Accept the terms and conditions of the program.

The terms include how much and when you get paid for your services. In very rare situations, you may be able to obtain minor adjustments in the standard program terms.

Contracting with an intermediate company

Some intermediary companies have direct relationships with mobile carriers that have been forged over many years. The intermediary firms sublicense your content to get it on a mobile carrier’s portal. Some of the leading players include BilltoMobile (www.billtomobile.com), Zong (www.zong.com), Mocapay (www.mocapay.com), PayOne (http://payone.com) and others.

Intermediaries are great channels because they enjoy economies of scale and greater reach than you can get on your own by going to each carrier individually.

Making Money through Premium Text Messaging

Premium text messaging, or PSMS (P for premium and SMS for Short Message Service, or text messaging — yes, all the jargon can be confusing), is an extremely common, fast, and versatile way to monetize a mobile marketing campaign by charging mobile subscribers for content you sell via the mobile channel. When you use PSMS, the price you charge for access to your content — 99¢, $1.99, $9.99, and so on — is billed to the consumer’s mobile phone bill, and after carrier collection of payments and deduction of carrier fees, you get a check.

PSMS can be used only for content and services that can be consumed (read, viewed, played, and so on) on a mobile phone or tablet, such as a text message, wallpaper, or ringtone. You can’t charge for physical goods or nonmobile services by using PSMS.

PSMS charges are billed in the mobile subscriber’s local currency. In the United States, for example, numerous fixed-price points between 10¢ and $29 are available for charging mobile subscribers via PSMS. A price point means that you can’t make up a price; you have to choose among the various price tiers that are available for you to use. Contact your application provider or messaging aggregator for a list of all the PSMS price points that you can use in each country.

You might consider using PSMS to charge your subscribers for the following:

• Entering a sweepstakes

• Voting in a poll, quiz, or survey

• Purchasing your content, such as text (news, horoscopes, sports alerts, and so on), wallpapers, screen savers, ringtones, applications, and games

See Figure 6-2 for how a PSMS charge appears on a mobile phone bill.

Figure 6-2: PSMS charge on a Verizon Wireless bill.

![]()

PSMS can be used for one-time purchases and donations as well as for recurring (weekly or monthly) billing. The versatility of this method comes from the fact that you can initiate the PSMS billing process from any marketing channel, including the following:

• Mobile-originated (MO) text messaging — that is, a message originated by consumers and sent from their mobile phones. MO messaging is used in all programs in which you’re mobile-enhancing traditional media and retail with a text-messaging call to action (see Chapter 2 of this minibook).

• A website or mobile Internet site.

• A widget, such as a plug-in for use on a social networking site.

• An interactive voice response (IVR) session. (See Chapter 2 of this minibook for more details on IVR.)

Putting PSMS to work: An example campaign

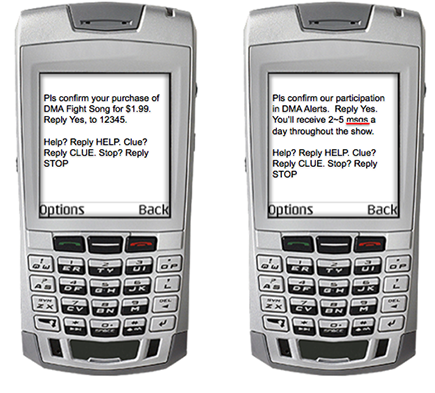

Suppose that you’re trying to sell a ringtone called BestSong and want to let everyone know about it. If you use PSMS, the process works as follows:

1. You promote the ringtone in various media:

• Traditional media: In flyers, on billboards, in store displays, and so on, you place a call to action like this one: “Text tone to 12345 to buy BestSong for $1.99. Standard messaging and other data rates apply.”

• Digital media: On a web or mobile website, in a widget, or in other digital media, you place a message like this one: “Enter your mobile number in the field below and click Submit to buy BestSong for $1.99. You’ll receive a text message asking you to confirm your purchase. Standard messaging and other data rates apply.”

• IVR: In an IVR session, the singer records a sultry prompt such as this one: “Preview and get the latest track I’ve laid down, BestSong, for $1.99. Say or press 1. You’ll get to hear the preview and then receive a text to confirm your purchase. Standard messaging and other data rates apply.”

2. The consumer responds to your call to action.

3. You send a text message to the consumer’s phone, asking him to confirm his purchase request. Your message may say something like this: “Please confirm your purchase of BestSong for $1.99 by replying yes. Standard messaging and other data rates apply. Reply help and/or stop.”

4. The consumer responds to your purchase request.

5. You send a text message with a download link to the consumer’s phone. Your message may say something like this: “Thanks. To download BestSong, click http://c4d.com/1212fas.”

6. The consumer downloads the ringtone.

7. You send the consumer a final text message to initiate billing (see Figure 6-3).

Figure 6-3: Initiating billing via PSMS.

The actual billing event happens after the content or service has been delivered — not before. Make sure that your application provider is handling this step properly.

Setting up a premium messaging program

Setting up a PSMS program is similar to setting up an SMS program (which is covered in Chapter 3 of this minibook), but you need to complete a few extra steps. To set up and run a PSMS program, you need the following elements:

• A Common Short Code (CSC) approved to run your premium program: This code must be certified for each price point you want to use it for. (For details on CSCs, flip to Chapter 2 of this minibook, and for more information about price points, refer to the section “Making Money through Premium Text Messaging,” earlier in this chapter.)

• A mobile marketing messaging application solution: You need a solution that’s compliant with carrier and messaging aggregator requirements in each country in which you plan to run the PSMS program.

If you want to bill through PSMS, make sure that you work with an experienced mobile services application provider. You must meet many rules, regulations, and technical requirements before mobile carriers allow you to bill via their networks using PSMS.

If you want to bill through PSMS, make sure that you work with an experienced mobile services application provider. You must meet many rules, regulations, and technical requirements before mobile carriers allow you to bill via their networks using PSMS.

• Campaign approval: The carrier has to review and approve your program and all its user flows, including ensuring that you receive text-message purchase confirmation from the consumer — known as a double opt-in. The carrier also must determine that your program meets all other requirements, such as opt-out, help, and privacy. (For more details on best practices and guidelines, refer to Chapter 1 of this minibook.)

If your program isn’t preapproved, the carriers won’t turn on billing support. If you have an active Short Code, your unapproved program may run, but one of two things will happen: (1) You won’t get paid, or (2) Your CSCs will be shut off, and you’ll be blacklisted.

Don’t skip the approval process, which takes 8 to 15 weeks. Ask your application or messaging aggregator provider (see Chapter 4 of this minibook for details on providers) to help you get certification.

Determining how much you’ll get paid and when

When you have your program up and running, you can start getting paid for your content and services. Typically, PSMS revenue is split among the following parties:

• Carrier and aggregator: Messaging aggregators and carriers retain a percentage of the gross receipts from PSMS billing events — combined, typically 40 to 60 percent. The percentage depends on the price points of the transactions, the total volume of transactions, and the carriers that the mobile subscribers are using. Payouts typically are made 12 to 15 weeks after the sale.

• Application and billing providers: Some application and billing providers will negotiate with you to share in a percentage of the revenue in lieu of or in addition to software licensing fees, download fees, or messaging transaction fees.

• Content rights holder: If you’ve licensed content from a third party, or if you’re using content licensed by your application provider, the content rights holder must be paid from the proceeds of the sale.

Be sure to get a rate card from the content rights holder before selling the content. You need to determine how much you can expect to earn — which may be less than you think. Suppose that you’re selling — in moderate volume — a ringtone for $1.99. The mobile carrier and aggregator retain 50 percent of the sale price, leaving 99.5¢. If you have a 20 percent revenue share with the application provider, and the cost of the ringtone from the content rights owner is 50¢, you’ll receive a payout of 29.6¢ per sale. And if you’re reselling leading-artist ringtones (referred to as master tones), you’ll receive 1 to 3 percent of the gross receipts after all the fees are deducted. Furthermore, carriers reserve the right to provide credit to customers who complain about a premium charge. Any such credits will be deducted from your receivables before they are paid.

Selling Your Content and Services via Mobile

The mobile phone is an incredible payment platform, because mobile subscribers almost always have their phones with them. In fact, most of us are never more than a few feet away from our phones.

Entire industries are looking to use the mobile phone for payment — not just for mobile-consumable goods and services, as discussed in the preceding sections — but in the last 18 months, the opportunity to sell physical goods and services with Internet-based billing methods has emerged. The following sections discuss the most common alternative billing methods you can use to get paid via the mobile phone.

Using mobile Internet link billing

One alternative method of promoting and selling mobile-consumable content and services is the mobile Internet. In industry jargon, this practice is often referred to as Wireless Application Protocol (WAP) billing, a legacy term for the mobile Internet. To continue the example from the section “Putting PSMS to work: An example campaign,” earlier in this chapter, you can promote your Hot New Ringtone track with a Purchase link on a mobile Internet page. But instead of using the PSMS channel, which uses text messaging to capture consumers’ consent to the charge, you can use mobile Internet link billing.

In mobile Internet link billing, mobile subscribers click a link on a mobile Internet page to initiate and then confirm their purchase of the content or service.

Billing via mobile Internet links is not something anyone can do; it requires special relationships with wireless carriers. If you want to use this method of billing on your mobile Internet site, you need to make sure that you’re working with a mobile application service provider that has mobile Internet link billing relationships with the connection aggregators, such as Ericsson IPX (www.ericsson.com/solutions/ipx) or OpenMarket (www.open market.com), or with mobile billing firms such as Bango (www.bango.com) or Buck (www.gobuck.com).

Internet-based billing solutions

Internet-based billing solutions leverage the Internet infrastructure to process payments. You have to rely on your payment-processing partners to help you pull all the pieces together. Payment-processing partners are companies that help you take in and process payments and then distribute the money with you after taking off a prearranged processing fee (typically 2.5 to 5 percent plus a per-transaction fee).

You can find numerous solution providers to assist you with integrating billing into your messaging, voice, mobile websites, and applications, including any number of e-commerce solution providers for the web and then mobile commerce specialists such as Visa (www.visa.com), MasterCard (www. mastercard.com), Google (www.google.com/Wallet), Buck (www.gobuck. com), PayPal (www.paypal.com), and Mocapay (www.mocapay.com).

You’ll also find all kinds of other types of mobile payments, specifically mobile banding and commercial and personal money transfers. These types of mobile payments are highly regulated by the government.

Using a mobile wallet

Money does not simply appear. Many people think that with mobile commerce, cash, checks, or credit cards are not needed. It may be true from a customer experience prospective, but you still need to have the customer get the money to you. Anytime someone stores money or links accounts, it’s a mobile wallet. The generally understood concept of the mobile wallet is that it is used to easily associate the consumer’s Internet-based billing account to her online credit, banking, or stored-value accounts. Here are a few options you can offer customers:

• Prepaid cards: The customer puts money on a card and then uses the card to purchase products with it. A prepaid card is similar to a debit card.

• Through an app: A customer can link an account (which has money in it) to a store with an app. He can then pay for purchases and add more money to his account through the app. (See the Starbucks example in the “Using mobile as a point-of-sale solution” sidebar.)

• A loyalty program: Customers can sign up for a loyalty program, giving a bank account or debit or credit card information to automatically pay for purchases through the program. (See the PayPal example in the “Using mobile as a point-of-sale solution” sidebar.)

Alternatively, if the consumer is not using a prepaid card, he often has the option of linking his bank account or debit or credit cards to the mobile payment service.

Using mobile as a point-of-sale solution

For many businesses, both large and small, mobile devices are increasingly used as a payment and redemption tool at the point of sale. Here are a few:

![]() Inmar, the industry-leading processor of paper coupons (to name just one of its many services), has a mobile solution that is integrated with many grocery stores. Users can scan coupons and associate their loyalty accounts with the Inmar system, and when they check out at the register, they simply need to scan their phone and/or enter their mobile phone number at the checkout keypad for the system to access their stored coupons, previous purchase history, rewards, and so on. All this information is then considered and applied to the consumer’s current transaction and added to his history.

Inmar, the industry-leading processor of paper coupons (to name just one of its many services), has a mobile solution that is integrated with many grocery stores. Users can scan coupons and associate their loyalty accounts with the Inmar system, and when they check out at the register, they simply need to scan their phone and/or enter their mobile phone number at the checkout keypad for the system to access their stored coupons, previous purchase history, rewards, and so on. All this information is then considered and applied to the consumer’s current transaction and added to his history.

![]() K&G Brands has also integrated its mobile programs, specifically its text-messaging-powered coupon program, with its point-of-sale system. Consumers simply need to text in to the text program, which is prompted in-store, to receive a coupon. They then can show the store associate their phone at the store to redeem the coupon.

K&G Brands has also integrated its mobile programs, specifically its text-messaging-powered coupon program, with its point-of-sale system. Consumers simply need to text in to the text program, which is prompted in-store, to receive a coupon. They then can show the store associate their phone at the store to redeem the coupon.

![]() Starbucks offers an app that allows customers to scan a phone at the register to pay for items with money stored in a Starbucks account. The customer can also use the app to reload the account with more money.

Starbucks offers an app that allows customers to scan a phone at the register to pay for items with money stored in a Starbucks account. The customer can also use the app to reload the account with more money.

![]() PayPal gives customers the choice to link one or more bank, debit, or credit card accounts to their PayPal account. Therefore, when they use PayPal to buy something, they don’t need their bank or credit card information.

PayPal gives customers the choice to link one or more bank, debit, or credit card accounts to their PayPal account. Therefore, when they use PayPal to buy something, they don’t need their bank or credit card information.

No universal mobile wallet exists. Today’s implementations require that a consumer have her account information duplicated across every Internet-based billing solution she chooses to work with. This information may include not just the consumer’s desired payment methods, but can also include — just like her physical wallet — coupons, receipts, and loyalty and reward cards.

If you are not ready to integrate your mobile programs into your stores’ point-of-sale system yet, not to worry; you can always leverage stand-alone mobile point-of-sale solutions:

• You can scan a phone screen and charge the consumer’s registered account. Check out LevelUp (www.thelevelup.com).

• Attach a small device to your phone, and it will act as a credit card scanner. The leading solution for this is Square (www.squareup.com). However, Intuit and PayPal are also coming out with their own offerings.

Mobile commerce solutions are innovating every day. Just keep looking around. For example, shopkick (www.shopkick.com) is an in-store loyalty engagement solution. People receive loyalty points for checking in at the store and scanning products. foursquare, the leading check-in social media solution, has partnered with American Express. If you check in via foursquare to a participating establishment, you can receive a discount, and if you pay with your American Express card, you’ll automatically receive the discount on your next credit card bill. Also, keep an eye out for contactless payment solutions like Near Field Communication (NFC), RFID, and SIM RFID. Future phones will be embedded with chips using these local-frequency technologies, which will link to the consumer’s mobile wallet. All a consumer will need to do is wave his phone over a scanner that can detect the NFC, RFID, or SIM RFID signal and a transaction is complete. No need for any messy credit cards, wallets, or keypads.