Clustering

Abstract

Clustering is an unsupervised data mining technique where the records in a data set are organized into different logical groupings. The groupings are in such a way that records inside the same group are more similar than records outside the group. Clustering has a wide variety of applications ranging from market segmentation to customer segmentation, electoral grouping, web analytics, and outlier detection. Clustering is also used as a data compression technique and data preprocessing technique for supervised data mining tasks. Many different data mining approaches are available to cluster the data and are developed based on proximity between the records, density in the data set, or novel application of neural networks. K-means clustering, density clustering, and self-organizing map techniques are reviewed in the chapter along with implementations using RapidMiner.

Keywords

Centriod; clustering; DBSCAN; density clustering; k-means clustering; Kohonen networks; Kohonen networks; self-organizing mapsClustering to Describe the Data

Clustering for Preprocessing

7.1. Types of Clustering Techniques

7.2. k-Means Clustering

7.2.1. How it Works: Concepts

Step 1: Initiate Centroids

Step 2: Assign Data Points

![]() (7.1)

(7.1)

Step 3: Calculate New Centroids

(7.2)

(7.2)

(7.3)

(7.3)Step 4: Repeat Assignment and Calculate New Centroids

Step 5: Termination

Special Cases

Evaluation of Clusters

7.2.2. How to Implement

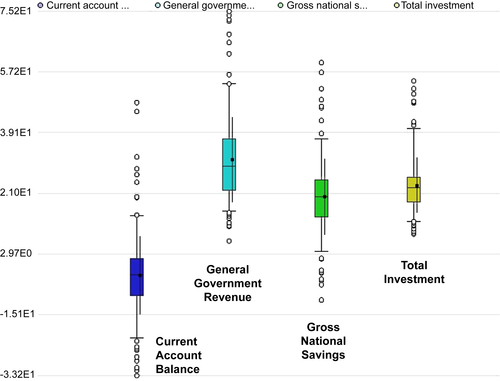

Step 1: Data Preparation

Step 2: Clustering Operator and Parameters

Step 3: Evaluation

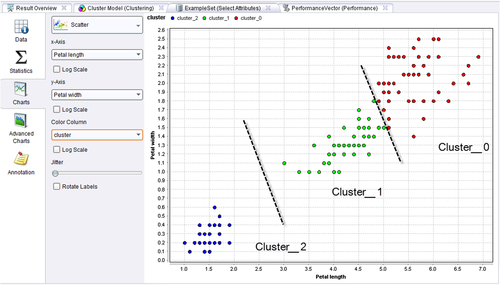

Step 4: Execution and Interpretation

7.3. DBSCAN Clustering

7.3.1. How it Works

Step 1: Defining Epsilon and MinPoints

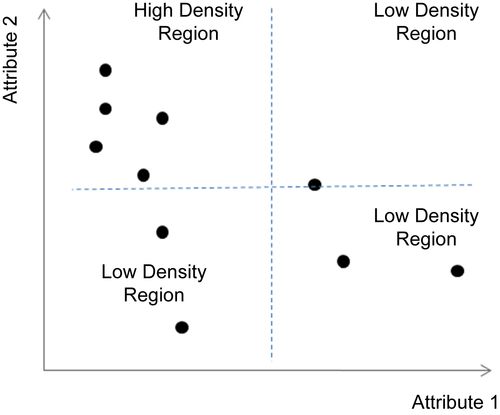

Step 2: Classification of Data Points

Step 3: Clustering

Optimizing Parameters

Special Cases: Varying Densities

7.3.2. How to Implement

Step 1: Data Preparation

Step 2: Clustering Operator and Parameters

Step 3: Evaluation (Optimal)

Step 4: Execution and Interpretation

7.3.3. Conclusion

7.4. Self-Organizing Maps

7.4.1. How it Works: Concepts

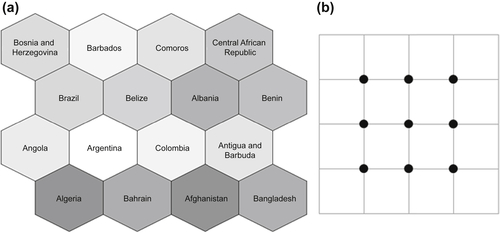

Step 1: Topology Specification

Step 2: Initialize Centroids

Step 3: Assignment of Data Objects

Step 4: Centroid Update

![]() (7.5)

(7.5)