Chapter 12

Risk-Neutral Pricing in the (B, S) Economy: One Underlying Stock

At this point we have the necessary tools in stochastic analysis for developing the theory of derivative pricing and hedging in continuous time in an economy where risky assets are modelled as Itô processes. In this chapter we consider an economy with two securities: a single tradable risky asset, namely, a stock, and a money market (bank) account or a bond. We refer to this as a (B, S) economy with only two tradable assets: B stands for the bank account or bond and S stands for the stock. More specifically, this chapter is devoted to presenting the theoretical framework solely within the classical case of an economy where the interest rate is fixed and the stock price is modelled as a standard geometric Brownian motion (GBM) with constant growth rate and constant volatility. The case in which the stock pays a dividend yield is also included later. The only source of randomness driving the stock price is a single Brownian motion. This is also referred to as the standard Black–Scholes framework. This can be thought of as the continuous-time analogue of the standard binomial tree model which was formally discussed in great detail in Chapter 7. The analogues of the up and down market moves in discrete time are now random movements of the underlying (driving) Brownian motion. The same important underlying concepts of self-financing, replication, hedging, arbitrage, and no-arbitrage pricing of derivative contracts in discrete time now carry over into the continuous-time setting.

All appropriately discounted tradable assets are martingales under an equivalent martingale (risk-neutral) measure. In particular, by using a self-financing replication strategy, we will arrive at the risk-neutral pricing formula that expresses the current price of any attainable European-style derivative, including contracts with path-dependent payoffs, as a conditional expectation (under the risk-neutral or equivalent martingale measure) of the discounted payoff. The class of derivative securities that are attainable is quite general. This chapter also includes a discussion of this and its relation to hedging and pricing. When pricing a non-path-dependent European-style derivative, the inherent Markov property reduces the risk-neutral pricing formula to a conditional expectation where the (discounted) Feynman-Kac formula allows us to arrive at the infamous Black–Scholes–Merton PDE for the current price of the derivative (option) contract. Recall that in Chapter 11 we made the important connection between the SDE of an Itô process, the (discounted) conditional expectation of a (payoff) function of the terminal value of the process, and the corresponding terminal (or initial) value PDE problem. This is the essence of the Feynman–Kac representation. Our discussion on the theoretical framework of the (B, S) economy culminates in the risk-neutral pricing formulation. We then apply this formulation to derivative pricing problems, where we explicitly derive pricing and hedging formulae for various European contracts, such as standard calls and puts, as well as more complex options such as compound options. We finally also apply the risk-neutral pricing formulation to path-dependent derivatives such as barrier options and lookback options.

12.1 Replication (Hedging) and Derivative Pricing in the Simplest Black–Scholes Economy

Following Section 11.8 of Chapter 11, we fix a filtered probability space (Ω, ℱ, ℙ, ), where is a filtration for standard Brownian motion, i.e., {W(t)}t≥0 is a standard (ℙ, )-BM where ℙ is the physical (real-world) measure. The first base security, B, in this market is the bank account whose price process is denoted by {B(t)}0≤t≤T. In this section we assume a constant interest rate r where B(t) = ert, i.e., B(0) = 1 and B(t) is one unit (dollar) of investment compounded continuously with fixed rate r over time [0, t]. The second base security is the stock whose price process is assumed to be a standard GBM satisfying the SDE

with constant drift µ and constant volatility σ > 0. We recall Example 11.15 in Section 11.8 of Chapter 11. There we showed, by a simple application of Girsanov’s Theorem, that there is a unique risk-neutral measure , defined by (11.96), where is a standard -BM. The discounted stock price process is a -martingale. For convenience, we repeat some of the important equations here. In particular, the stock satisfies the SDE

with solution

The discounted stock price process, with discount factor D(t) := 1/B(t) = e−rt, is a -martingale:

Note also that dB(t) = rB(t)dt has an identically zero coefficient in and that is trivially a (constant) martingale under any measure. Hence, is an equivalent martingale measure (EMM) with the bank account as a numéraire asset.

As in the discrete-time models, we assume no arbitrage in the market and will, below, set up a self-financing replicating portfolio strategy in the two base securities such that the value of the portfolio replicates the value of the financial derivative at some future (maturity) time T. In the absence of arbitrage, the time-t value of the self-financing replicating portfolio must therefore equal the no-arbitrage price of the derivative. Let {Vt}0≤t≤T denote the price process of the derivative security where Vt is the price of the derivative at time t ≤ T. At maturity T, the derivative price is given by the payoff value VT, which is an ℱT-measurable random variable. In the present model, VT is generally some functional of the Brownian motion (BM) up to time T or equivalently some functional of the underlying stock price process {S(t)}0≤t≤T. This functional can be quite complex for a general path-dependent payoff, although for a non-path-dependent derivative (as, for example, a standard call or put) the payoff is only a function of the terminal stock value S(T).

In this (B, S) economy any portfolio (trading) strategy is a continuous sequence of portfolios in the two base assets: (βt, Δt), 0 ≤ t ≤ T, with each process {βt}0≤t≤T and {Δt}0≤t≤T assumed to be adapted to the filtration . As in the binomial model, βt represents the time-t position in the bank account where βt < 0 corresponds to a loan and βt > 0 is an investment. The hedge position Δt is the number of shares held in the stock at time t where Δt < 0 corresponds to shorting the stock and Δt > 0 is a long position. Since we are in continuous time, trading (i.e., portfolio re-balancing) is allowed at any moment in time. The investor begins with a given initial wealth Π0, which completely finances the initial portfolio with positions (β0, Δ0) and subsequently trades at every time t ∊ [0, T] while holding Δt shares in the stock and βt units in the bank account, i.e., this is represented by the portfolio value process for t ∊ [0, T]:

In what follows, we will only consider self-financing portfolio strategies. In analogy with the binomial model, a self-financing portfolio strategy is one in which the differential change in portfolio value is due only to differential changes in the prices of the base assets. Essentially this means that the investor holds the positions (βt, Δt) during the infinitesimal time window [t, t + dt). At time t + dt the BM will have changed by a differential amount dW(t), the stock will have changed its share price by a differential amount dS(t), and the investment in the bank account will have either accrued interest (if βt > 0) or will have decreased in value if βt < 0. Formally, a self-financing portfolio strategy is then a portfolio strategy (βt, Δt), 0 ≤ t ≤ T, such that the cumulative gain in portfolio value is given by

with probability one (a.s.). It is more convenient to work with the differential form of (12.5),

From (12.4) we can express the bank account investment (or loan) as βtB(t) = Πt − ΔtS(t) and substituting this into the above differential, where βt dB(t) = rβtB(t)dt, gives

We can recognize this as the differential form of the continuous-time analogue of the wealth equation we encountered in the binomial model.

As in the binomial model, the discounted self-financing portfolio value process, defined by , is a -martingale. This is readily shown by applying the Itô product rule to the process e−rtΠt ≡ D(t)Πt, where dD(t) dΠt = −rD(t)dt dΠt ≡ 0, and using (12.6):

In the last equation line we made use of (12.3). This therefore shows that is a -martingale and that changes in this discounted self-financing portfolio are due only to changes in the discounted stock price. In integral form we have

Note: we are assuming that the above Itô integral is square integrable. This guarantees that the process defined by (12.8) is a -martingale. This technical detail can be verified later once the option price, and hence the delta position, is obtained.

As in the binomial model, we wish to price derivative contracts that can be replicated by a self-financing portfolio strategy. Let us therefore give a definition of this for the above continuous-time model.

A self-financing strategy (βt, Δt), 0 ≤ t ≤ T, is said to replicate the ℱT-measurable payoff VT at maturity T if ΠT = VT (a.s.), i.e., ℙ(ΠT = VT) = 1. We also say that the payoff VT is attainable.

Let us suppose that a self-financing portfolio strategy that replicates the derivative payoff VT exists. Later we give some discussion on this existence. Then, the cost at any time t ≤ T to set up such a strategy, i.e., the portfolio value Πt, must equal the time-t price of the derivative Vt in order for the investor to hedge (at time t) the short position in the derivative security that has the given attainable payoff VT at future time T, and hence avoid arbitrage. Therefore, we set Vt = Πt for all 0 ≤ t ≤ T for any attainable payoff VT.

The key step now is to make use of the -martingale property in (12.8). In particular, we have

and, since Vt = Πt, then . The discounted derivative price process, {D(t)Vt ≡ e−rtVt}0 ≤ t ≤ T , is therefore a -martingale. We can combine the discount factors, where D(T)/D(t) = B(t)/B(T) = e−r(T −t), giving

This is the risk-neutral pricing formula for the above (B, S) model with a constant interest rate. It is the continuous-time analogue of (7.23) for the binomial model in Chapter 7. We remark that (12.9) was derived for the simplest case where the stock is a standard GBM, but in Chapter 13 we will arrive at the same formula for more general continuous-time stock price processes as long as the payoff is attainable and there exists a risk-neutral measure where the discounted stock (base asset) price process is a -martingale. In Chapter 13 we shall also define an arbitrage strategy in the multi-asset continuous-time framework where it is shown that the existence of a risk-neutral measure implies that no arbitrage strategies are possible within the market model.

The formula in (12.9) may seem very simple; however, its practical use rests upon our ability to calculate the expectation of the payoff conditional on the filtration at time t. The payoff is an ℱT-measurable random variable and it can, in some cases, be quite complex, as it may have a complicated dependence on the path of the stock price process. Hence, the conditional expectation can be quite challenging to compute for complex path-dependent payoffs. The main idea is to simplify the ℱt-conditional expectation to an expectation that can be readily computed. In most practical situations the derivative has a payoff structure that is not too complex. In the binomial model, we have already used the risk-neutral pricing framework to value derivatives having commonly encountered payoffs, such as the standard European call and put options as well as path-dependent options such as lookback and Asian options. Our main tools for analytically pricing such options were the Markov property and the Independence Proposition 6.7 or 6.8. For continuous-time models these tools will also be used within the risk-neutral framework. Moreover, we shall also have other tools at our disposal, such as the PDE approach that is a result of the Feyman–Kac theorems.

Let’s now consider the case of a standard (non-path-dependent) European option with payoff VT = Λ(S(T)) as a ℱT-measurable random variable that is a function of only the terminal (maturity time T) value of the stock price. The important simplification that now follows is due to the Markov property where the conditioning on ℱt is replaced with a conditioning on S(t). We remind the reader of our discussions in Section 11.7 on conditional expectations and the Markov property. In particular, recall that a solution to an SDE is a Markov process and hence (11.42) in Theorem 11.5 applies. The time-t derivative value (expressed as a σ(S(t))-measurable random variable) then takes the form

The derivative pricing function, V(t, S), is a function of calendar (actual) time t and the spot1 (ordinary variable) S > 0 and is given by the discounted expectation of the payoff conditional on S(t) = S:

Given the share price for the stock at time t ≤ T, which is the spot S > 0, then (12.11) gives us the no-arbitrage time-t price of a European option having non-path-dependent attainable payoff Λ(S(T)) at maturity T, where Λ : ℝ+ → ℝ is the payoff function.

We can now generally express the pricing function in (12.11) as an integral over the standard normal density n(z) or equivalently as an integral over the risk-neutral transition PDF. This has essentially already been done in Example 11.11 of Chapter 11 where related formulas were derived under measure ℙ with drift µ (instead of with drift r). Using (12.2), the time-T stock price is given in terms of the time-t price and the -BM increment:

Throughout, we conveniently define τ := T − t as the time to maturity and

which is a standard normal random variable, i.e., under measure . Note that is independent of S(t) since is independent of . Combining these facts into (12.11) gives

By changing integration variables in (12.14), i.e., letting , gives the equivalent pricing formula

where denotes the risk-neutral transition PDF of the stock price process in (12.2):

We recall that this is the time-homogeneous log-normal density in y given by (11.79) with drift parameter µ set to the risk-free rate r. Note that when the stock price process is time homogeneous, as in the present case, the pricing formula is a function of the time to maturity τ = T − t and we shall also denote it by ν(τ, S) := V(t, S), i.e., ν(τ, S) := V(T − τ, S).

We see that (12.14) and (12.15) provide two equivalent expectation (integral) approaches for pricing standard European options on a stock. The transition PDF is the fundamental solution to the PDE in (11.72) with the spot value as a backward variable, x ≡ S, linear diffusion coefficient function σ(x) ≡ σ(S) = σS, and linear drift coefficient function µ(x) ≡ µ(S) = rS. The discounted transition PDF, , and hence the pricing function ν = ν(τ, S) in (12.15), satisfies the PDE in the variables (S, τ) (see (11.77) in Chapter 11):

subject to the payoff condition ν(0+, S) = Λ(S), which is an initial condition in the time to maturity τ ↘ 0. This is the Black–Scholes partial differential equation (BSPDE) for the pricing function expressed as function of the spot and time to maturity variables (S, τ). Since , then (12.17) is equivalent to

subject to the payoff condition V(T −, S) = Λ(S), which is a terminal condition in time t ↗ T. This is the usual BSPDE satisfied by the pricing function V = V(t, S) in the variables (t, S). In fact, the BSPDE in (12.18) arises by direct application of the discounted Feynman– Kac Theorem 11.9 to the conditional expectation in (12.11). [Note that Theorem 11.9 is the same when we replace ℙ, E, and W everywhere by , , and , respectively. All this means is that the probability measure is now the risk-neutral measure . Here, we have the dummy variable x ≡ S and the process X(t) ≡ S(t) is GBM with coefficient functions defined by µ(t, S) := rS, σ(t, S) := σS in the SDE (12.1). In particular, for constant interest rate r the pricing function V(t, S) satisfies the PDE (11.64) in the variables t and S, which is the BSPDE in (12.18).]

Let us now turn our attention to the problem of replicating a derivative claim, i.e., the hedging problem in the simple (B, S) model. We first see how this problem is solved in the case of non-path-dependent payoffs where VT = Λ(S(T)) and Vt = V(t, S(t)). By applying the Itô formula with the differential in (12.1) we obtain:

where is the differential generator corresponding to the GBM process with SDE in (12.1). Now using the fact that the pricing function V(t, S) satisfies the BSPDE in (12.18), i.e., for all (t, S), then

for all t ∊ [0, T]. Assuming the square-integrability condition on the integrand of this Itô integral, {e−rtV(t, S(t))}0≤t≤T is a -martingale. For portfolio replication we require Πt = V(t, S(t)), or , for all t ∊ [0, T]. We see from (12.8) that this can be achieved by setting the initial value of the portfolio Π0 = V0 = V(0, S(0)) and by choosing the delta position such that the respective Itô integrals in (12.8) and (12.19) are equal, i.e., the delta hedge is achieved by choosing

Hence, (12.20) gives the time-t (delta) position in the stock required to dynamically replicate the derivative claim in a self-financing portfolio strategy. Clearly, Δt is ℱt-measurable (in fact it is σ(S(t))-measurable) and is given uniquely by the first derivative (w.r.t. the spot variable S) of the pricing function evaluated at S = S(t). Defining the function , then Δ(t, S) gives the time-t position in the stock given the spot value S. Once the pricing function V(t, S) is known (and hence its derivative computed) the self-financing replicating portfolio in (12.4) is given by Δt = Δ(t, S(t)) positions in the stock and βt = e−rt[V(t, S(t)) − S(t)Δ(t, S(t))] units in the bank account, i.e., the value of the bank account portion of the portfolio at time t is V(t, S(t)) − S(t)Δ(t, S(t)).

Consider the general case where VT is any ℱT-measurable payoff (i.e., generally path dependent). Now, we generally have Vt ≠ V(t, S(t)) (i.e., we do not generally have Vt = as a function of t and S(t)) and hence the above BSPDE and Feynman–Kac results are not generally applicable. However, what is important is that the discounted derivative value process {D(t)Vt}0 ≤ t ≤ T is a (, )-martingale. We now show that we can guarantee that VT is attainable if we make two general assumptions on the payoff:

- VT is square integrable, i.e., E[VT2] < ∞.

- VT is ℱTW-measurable.

[Note that these two conditions are already implicit in the above non-path-dependent case.] The discounted price process {D(t)Vt}0 ≤ t ≤ T is then a square-integrable (, )-martingale. We can now make use of Theorem 11.14, in particular Proposition 11.15 of Chapter 11, where we identify M(t) ≡ D(t)Vt and identify the measure , with constant γ(t) = γ ≡ (r − µ)/σ being ℱtW-adapted. This implies2 and hence {D(t)Vt}0 ≤ t ≤ T is a square-integrable -martingale. Hence, there exists an adapted process, we now denote by , such that (note D(0)V0 = V0):

For portfolio replication we require Πt = Vt, for all t ∊ [0, T]. By (12.21) we see that this is achieved by setting Π0 = V0 and by choosing the delta position such that the integrands in (12.8) and (12.21) are equal, i.e., the delta hedge is achieved by setting [note ]

for all t ∊ [0, T]. This solution for Δt exists, for every , since we are assuming that the volatility parameter σ > 0. Note also that the stock price is a GBM with S(0) > 0 and therefore cannot hit zero in any finite time. Of course, implicit in this existence are also the above assumptions on the derivative payoff. Namely, VT must be ℱtW-measurable and this means that we can only guarantee replication of payoffs whose only source of randomness is the BM driving the stock itself.

We have therefore shown that the model can replicate (hedge) any complex arbitrary path-dependent derivatives with a payoff satisfying the above two assumptions. In this sense we can say that the (B, S) model is a complete market model. The formula in (12.22) asserts the existence of a hedging strategy and therefore justifies the use of the risk-neutral pricing formula in (12.9). We remark that generally (12.22) does not give a practical (or explicit) construction of the hedging strategy. However, there are important examples of common payoffs for which we do have an explicit formula for the delta hedge. For example, in the particular case of a non-path-dependent standard European option we already showed that θ(t) is given explicitly in terms of the derivative of the pricing function:

with the delta position given by (12.20).

12.1.1 Pricing Standard European Calls and Puts

We now use the risk-neutral pricing formulation to derive the well-known Black–Scholes– Merton formulae for the prices of a standard call and put option in the simplest (B, S) model of Section 12.1, where the stock price is a GBM with constant volatility σ > 0 and the bank account has constant interest rate r. Here we are assuming a zero dividend on the stock, but the inclusion of a stock dividend is quite simple, as shown later.

Consider a call option with payoff VT ≡ CT = (S(T) − K)+. This is an example of a non-path-dependent option with payoff function Λ(x) := (x − K)+. Let S(t) = S > 0 be the spot price of the stock at time t ≤ T. Since the payoff depends only on the terminal stock price S(T), the (current) time-t price of this call with strike K > 0 can be found by directly evaluating the integral in (12.14) using the identity (A.1) in the Appendix. We leave this as an exercise for the reader. We recall that in Chapter 4 a brute force integration of (12.14) was also used in deriving the time-0 price of the put option with payoff Λ(x) = (K − x)+. Here we carry out the derivation in an explicit manner that is instructive since it clearly displays the use of the conditional expectation approach and the connection between the different random variables and independence. In particular, using (12.11), the time-t price of the call, C(t, S), is the discounted risk-neutral expectation of the payoff at time T > t, conditional on S(t) = S:

with S(T) given by (12.12). Two conditional expectations need to be computed (where the last term has been expressed as a conditional probability). In both cases we use the fact that in (12.13) is independent of S(t) and, by the Independence Proposition 6.7, this allows us to remove the conditioning upon setting S(t) = S. First, let us rewrite the event {S(T) > K} in terms of and S(t) by simply dividing S(T) in (12.12) by S(t), dividing K by S(t), and taking natural logarithms:

where we define

for all x > 0, τ := T − t > 0. We use the above representation for the event and substitute the expression for S(T), given in (12.12), into the first expectation in (12.23), which is now readily computed by setting S(t) = S, using the independence of and S(t), and then applying the identity3 in (A.1) of the Appendix to evaluate the (unconditional) expectation:

The conditional probability in (12.23) now follows quite simply:

Note that this is also obtained directly from the transition CDF, , of the GBM process under measure , where

Substituting (12.25) and (12.26) into (12.23) completes our derivation of the pricing formula for the standard call:

Having priced the call, we can now easily derive the pricing formula for the put price, P(t, S), by recalling the simple symmetry between the call and put payoffs, i.e., a portfolio in one long call and one short put is equivalent to a portfolio in one long forward contract:

Taking discounted risk-neutral expectations on both sides of (12.28) gives

where we recognize the left-hand side as the difference in the time-t price of the call and put, at strike K. The right-hand side is the time-t price of a forward contract with payoff S(T) − K. This is the put-call parity relation that we have already encountered in our primer chapter (Chapter 4) on derivative securities. It is important to note that this relation is valid for quite general models (i.e., beyond the GBM model). The only assumption is that the discounted stock price is a -martingale. Substituting the call price in (12.27) into (12.29) gives the pricing formula for the standard put:

We leave it as an exercise for the reader to show by direct differentiation that the above call and put pricing functions in (12.27) and (12.30) solve the BSPDE. The initial conditions τ ↘ 0 (equivalently t ↗ T) on the above pricing functions are readily shown to be satisfied by working out the limiting forms (see also Example 11.11):

Hence, both limits equal the unit step function centered at S = K. Using both these limits in (12.27) verifies the payoff condition for the call:

By the same steps applied to (12.30), we verify the payoff condition:

The asymptotic values for the call and put pricing functions for small and large spot values are readily obtained. We leave it as an exercise to show, by directly computing the limits, that

and

The financial interpretation of the above limits is clear. In the limit that the time-t stock price (spot S) is very close to zero, it will remain close to zero within a finite time to maturity τ = T − t. This means that the call will certainly expire out of the money (hence is worthless) and the put will expire completely in the money with payoff K and time-t value e−rτ K. In the limit of arbitrarily large spot value, the stock price will remain arbitrarily large, i.e., the put will certainly expire out of the money (hence is worthless) and the call will expire in the money with an arbitrarily large payoff.

12.1.2 Hedging Standard European Calls and Puts

In Chapter 4 we computed the “delta” of a standard call and put by differentiating the pricing functions. Let us denote the delta of the call at calendar time t by and the delta of the put by . Note that Δc and Δp are also functions of (τ, S), since the pricing functions in (12.27) and (12.30) are expressible as functions of (τ, S). We recall a previous method to derive Δc by simply differentiating (12.27) w.r.t. S, where , while using ,

Here we used the following identity with x = S/K (which we leave as a somewhat tedious exercise in algebra for the reader to show):

The above derivation of Δc is correct but perhaps not the most instructive. We now give an alternate derivation of Δc by directly connecting it to the discounted risk-neutral conditional expectation in (12.25). From the risk-neutral pricing formula in (12.14),

We now differentiate w.r.t. S (as a parameter) inside the expectation or inside the integral and use the property . In the integral we have or in the expectation . We can write the steps compactly as follows by differentiating inside the expectation (note: ),

Here we identified the conditional expectation in (12.25).

It is important to note that the delta of a call is strictly positive, i.e., Δc(t, S) > 0 for all t < T, S > 0, since the CDF is strictly positive for all x ∊ ℝ. Hence, according to (12.20), to replicate a call the writer is continuously re-balancing the self-financing portfolio while always maintaining a delta positive (long) position in the stock given by for τ = T − t > 0. In particular, the time-t investment in the stock, given spot S(t) = S, is

Since Πt = C(t, S(t)) = C(t, S), the time-t value of the bank account (cash) portion of the self-financing portfolio is, upon using (12.27),

This quantity is negative for all t < T, S > 0. Hence, the writer of the call is always maintaining a negative position (loan) in the bank account.

The delta position at maturity t = T is given by the limit t ↗ T of the function in (12.34). From (12.31) we see that, in the limit of zero time to maturity, Δc approaches the unit step function with discontinuity at S = K. Moreover, for any fixed τ > 0, we observe that Δc is a strictly increasing function of S with limiting values of zero and unity:

Figure 12.1 contains typical plots of Δc for different values of τ. We clearly see that Δc approaches the unit step function as τ ↘ 0. As τ ↘ 0, (12.34) gives Δc → 0 for S < K, Δc → 1 for S > K, and for S = K. We see that Δc gets progressively steeper for smaller and smaller values of τ and eventually becomes the unit step function. At a time t just before expiry (i.e., τ ≍ 0), if the stock price lies above K, then Δc ≍ 1 and the hedging replicates the positive payoff of the call after paying off the loan in the amount of K (see (12.31) and the above expression for βtB(t)). On the other hand, if the stock price is below K (out of the money), then Δc ≍ 0 and βtB(t) ≍ 0, so the hedge replicates the zero payoff of the call.

Typical plots of the call delta as function of spot for four different values of time to maturity τ.

There are also scenarios where the stock price S(t) just before expiry (t ≍ T) stays very close to the strike K until time T. There is a fairly high probability (which is easily computed) that the stock price will fluctuate between values below K and above K. These are scenarios where the stock is said to be “pinning the strike.” For values of τ close to zero this would mean that the (hedge) position in the stock would have to be re-balanced, in a short time, between a very small long position (Δc ≍ 0) and a large long position where the replicating portfolio is almost all stock (Δc ≍ 1). This re-balancing requires either selling off a large portion of the underlying stock or buying up a large portion of stock so as to maintain the correct hedge. In particular, if the stock price suddenly moves just before expiry from one side of the strike to the other, then the writer or trader must rapidly trade enough of the underlying stock before expiration in order to hedge the loss against such a movement. In the (B, S) theoretical (idealized) model such transactions are assumed to occur instantaneously (as efficiently as is required!) and without any liquidity issues in trading, i.e., all scenarios are, in theory, hedged. In the real world these kinds of scenarios cannot be hedged effectively in time since instantaneous re-balancing is obviously not possible. Moreover, there are transaction fees associated with each trade. The risk associated with options trading whereby the market price of the stock is pinning the strike is referred to as pin risk. Later we consider the pricing of a so-called soft-strike call. This contract differs from the standard call, as its payoff is everywhere differentiable and it has a continuous range of strikes. This type of option avoids the problem of pin risk when delta hedging.

The delta of a put option, Δp, follows trivially by put-call parity,

The delta of a put is therefore strictly negative and is simply related to the call delta by Δp = Δc − 1. A put option is replicated by continuously re-balancing with a delta negative (short) position in the stock given by . Given spot S(t) = S, the time-t value of the stock portion of the replicating portfolio for the put is given by

The self-financing replicating portfolio value for the put is Πt = P(t, S(t)) = P(t, S), so the corresponding time-t investment in the bank account is

In direct contrast to the call, the put is replicated by always maintaining a positive investment in the bank account.

At maturity t = T, Δp(T, S) = Δc(T, S) − 1= H(S − K) − 1. For τ > 0, Δp is a strictly increasing function of S with limiting values:

The above discussion on hedging and pin risk associated with the call also applies in an obviously similar manner to the put with given strike K. We note that for the put delta the corresponding plots of Δp as a function of S are as in Figure 12.1, where the origin of the vertical axis is simply shifted up by unity.

In closing this section we recall that the delta is one among other so-called “Greeks” of an option that are of interest to practitioners such as options traders. Recall that in Section 4.3.4.4 of Chapter 4 we provided some discussion of these quantities. This chapter is focused on risk-neutral pricing and hedging of options. We leave it as an exercise for the reader to derive the corresponding formulas for the gamma, theta, vega, and rho of a standard call and put expressed as a function of S, τ, K, r, σ.

12.1.3 Europeans with Piecewise Linear Payoffs

Equations (12.25) and (12.26) are useful for pricing any European option having a piece-wise linear payoff with possibly a finite (or countable) number of discontinuities. Actually, the standard call and put options are important special cases of such payoffs with no discontinuity and a discontinuity in their first derivatives. Let’s now consider a simple example of a piecewise constant payoff with a single jump discontinuity.

(Asset-or-Nothing Binary Call) Consider an option that pays the holder the value of the underlying share price of the stock if the stock price at expiry is above a given strike K and is otherwise worthless, i.e., the holder gets the asset (stock) or nothing with payoff function

Derive the risk-neutral pricing formula and the hedging position in the stock for the European option with this payoff.

Solution. Observe that the payoff is also the first term in the standard call option. The risk-neutral pricing formula immediately follows from (12.25):

where τ = T − t. The delta hedge is obtained by straightforward differentiation,

Note that the time-t replicating portfolio is always long in the stock with a bank loan in the amount of .

Recall that a cash-or-nothing binary call has payoff Λ(S) = ?{S≥K}. Hence, a standard call struck at K is a portfolio consisting of K short positions in a cash-or-nothing call and one long position in an asset-or-nothing call, both struck at K.

We now consider a derivation of the risk-neutral pricing formula for a European option with arbitrary piecewise linear payoff, assuming the standard GBM model for the stock. As a general form for the payoff we consider the sum of linear functions restricted to any number n ≥ 1 of nonoverlapping intervals:

with any real constants Ai, Bi and where 0 ≤ a1 < b1 ≤ a2 < b2 ≤ ... ≤ an < bn ≤ ∞. This function can account for a number of jump discontinuities (including no discontinuities), piecewise constant payoffs, and piecewise linear payoffs with any combination of positive and negative slopes.

As a concrete example, let n = 1. A call with Λ(S) = (S − K)+ is then given by (12.37) with parameter choice A1 = 1, B1 = −K, a1 = K, b1 = ∞. A cash-or-nothing binary call with Λ(S) = ?{S≥K} obtains with A1 = 0, B1 = 1, a1 = K, b1 = ∞. The payoff of an assetor-nothing call, Λ(S) = S ?{S≥K}, corresponds to A1 = 1, B1 = 0, a1 = K, b1 = ∞. For n = 2, an example is the butterfly spread with strikes K1 < K2 < K3, K2 = (K1 + K3)/2, which is representable as a linear combination of piecewise linear functions with payoff . This corresponds to setting the parameters in (12.37) to A1 = 1, B1 = −K1, a1 = K1, b1 = K2 and A2 = −1, B2 = K3, a2 = K2, b2 = K3.

In order to make use of the conditional expectation identities in (12.25) and (12.26) we write and express the payoff in (12.37) as

Applying the identities in (12.25) and (12.26) and the linearity property of expectations, we arrive at an analytical expression for the risk-neutral pricing formula of a European option with payoff in (12.37):

where τ = T − t and d±(x, τ) functions defined in (12.24). We leave as an exercise the derivation of a general formula for the delta hedging position Δ(t, S) for this option. The pricing formula in (12.38) is applicable to several payoff forms that occur in practice and we leave some as assigned exercises at the end of this chapter.

12.1.4 Power Options

Power options differ from vanilla European options in that the payoff function is not linear but raised to some power in the underlying spot. We now show how to analytically value such options under the GBM model. Typically, the payoff of a power option is a quadratic function of the stock price. The widest possible application of power options is for addressing the nonlinear risk of option sellers. There was proposed a class of soft-strike options which do not have a single fixed strike price but a continuous range of strikes spread over an interval. As was mentioned earlier, such options allow for addressing limitations of a standard delta hedging when the underlying asset is pinning the strike at the expiration of the option.

More generally, the payoff of a power option may involve the terminal stock price raised to some power, e.g., Sα(T) ≡ (S(T))α with either positive or negative exponent α ≠ 0, as well as other terms involving Sα(T) times an indicator function restricting the value of S(T) on some interval. Let’s assume that the payoff is some linear combination of elemental payoffs having any of the three forms

where A1 < A2 and A are nonnegative constants. Hence, by the risk-neutral derivative pricing formulation the present value of a power option at time t < T will involve expectations of the above payoffs under the risk-neutral measure . We can handle all of the above three payoffs by simply deriving a formula for the conditional expectation of the payoff Sα(T) ?{S(T)>A}, for any A ≥ 0, since

Note also that for A1 = 0 we have

where ?{S(T)>0} = 1 since the stock price is always positive. The expectation of Sα(T), conditional on a given spot value S(t) = S > 0, for any t < T, is easily calculated using (12.12) raised to the exponent α. Again we use the fact that in (12.13) is independent of S(t) (under measure ), which allows us to remove the conditioning upon setting S(t) = S:

where τ := T − t. The only difference between the conditional expectation in (12.40) and that of Sα(T) ?{S(T)>A} is the indicator function term. By the exact same step as in our derivation of the standard call and put options, the indicator random variable term simplifies,

with d± defined in (12.24), i.e., . Then, conditioning on S(t) = S and using independence,

The last expectation was computed using the identity in (A.1) of the Appendix and noting that . Note that this formula also recovers (12.40) in the limit A ↘ 0. This follows by monotone convergence of the expectations where ?{S(T)>A} ↗ ?{S(T)>0} = 1, as A ↘ 0. Based on (12.39) and the linearity property of the expectation, using (12.41) for A = A1 and for A = A2 leads to the formula

We now use the formulae in (12.40)–(12.42) to price a soft-strike call option in the following example.

(Soft-Strike Call Option) Consider the soft-strike European call option with payoff function

where the constant a ∊ [0, K] and K is a central strike value.

- (a) Describe the main features of the graph of Λa(S) for all S > 0.

- (b) Assume the stock price process {S(t)}t≥0 is a GBM with constant interest rate r and volatility σ. Let S(t) = S be the spot price of the stock at current time t < T. Derive the no-arbitrage pricing formula for a European-style option with the above payoff function.

Solution.

(a) (see Figure 12.2) Note that Λa(S) ≥ (S − K)+, where Λa(S) ↘ (S − K)+ as a ↘ 0, i.e., as a function of the parameter a, the soft-strike payoff decreases monotonically to the standard call payoff as a ↘ 0. In contrast to the standard call payoff (S − K)+ whose derivative w.r.t. S has a unit jump discontinuity at S = K, the payoff Λa(S) has a continuous derivative for all S. The left and right derivatives at S = K − a are the same, Λ′a (K − a) = 0, and the left and right derivatives at S = K + a are the same, Λ′a (K + a) = 1. Combining this with the derivative for S ∊ (K − a, K + a), the payoff has a continuous derivative w.r.t. S given by

Moreover, the payoff has a piecewise constant second derivative Λ′a(S). In fact, the payoff can be expressed as an integral over the standard call payoff function (S − k)+ by employing a continuum of strikes k ∊ (K − a, K + a) (see Exercise 12.14).

(b) Express Λa(S(T)) as a linear combination of payoffs involving the different powers of S(T) multiplying indicator random variables:

The option value at current time t is then the discounted conditional expectation of this payoff. Let V(t, S) ≡ C(t, S; K, a) denote the time-t value of the soft-strike call where we include the dependence on the parameters a, K defining the payoff. By linearity of expectations:

We now use the formulas given in (12.41) and (12.42) for respective powers of α =1, 2, as well as our previously derived formulas for the risk-neutral conditional probability that S(T) lies above a strike level or within an interval. Combining all terms gives

where τ = T − t is the time to maturity and d±(x, τ) are defined in (12.24).

Based on the pricing formula in (12.45) we can compute the delta hedging position in the stock. Moreover, we can readily price the corresponding soft-strike put option with given center strike K and width a. We leave this as an exercise for the reader (see Exercise 12.15). There are also other power options that are readily priced with the use of the formulae in (12.40)–(12.42) and these are assigned as exercises at the end of this chapter.

12.1.5 Dividend Paying Stock

12.1.5.1 The Case of Continuous Dividend Paying Stock

Let us now consider the above (B, S) model where the stock is a standard GBM which also pays a dividend with a constant continuous yield q > 0 per unit of time. During an infinitesimal time dt the holder of the stock receives a dividend payment of qS(t)dt that is in proportion to the stock price at time t. We can see this from the return due only to the dividend, for small time interval δt ≍ 0. By no-arbitrage this dividend payment to the stock holder must be exactly balanced by a decrease in the share price of the stock. Hence, in the physical P-measure there is the additional negative drift term, −qS(t)dt, due to the dividend. The stock price process is a GBM with SDE

By the same unique risk-neutral measure as above, where is a standard -BM, the above SDE takes the form

For a nonzero dividend, the risk-neutral drift of the stock price is (r − q) in the place of r. Given an arbitrary initial stock value S(0) > 0, this SDE has a unique solution

The time-T stock price is given in terms of the time-t price and a -BM increment:

Note that the process acts as a nondividend stock, i.e., it has the same risk-neutral drift, r, as any non-dividend-paying asset. Discounting the price process with the bank account gives as a -martingale.

The replicating portfolio is the same as given in (12.4). The portfolio is invested in the amount of ΔtS(t) in the stock, so the dividend payment is qΔtS(t)dt over time dt. This term is now added to the differential change in the self-financing portfolio in (12.6), giving

In the last line we used (12.46). This is of the same form as in (12.7) and hence (12.8) still holds where the discounted self-financing portfolio value process is a -martingale. The risk-neutral pricing formula in (12.9) as well as (12.10) and (12.11) still hold. The conditions and arguments given in Section 12.1 that guarantee that a claim can be replicated (hedged) are the same as in the case of zero dividend on the stock.

The only difference is that the stock has drift parameter (r − q) instead of r, i.e., S(t) is given by (12.47) instead of (12.2) and (12.48) replaces (12.12). So the question is, in terms of pricing, what does this change? The general answer is actually very simple given the solution in the case that q = 0. Let’s take a look at how (12.14)–(12.20) change. Using (12.48) in the place of (12.12), the expectations in (12.14) and (12.15) now become

where is now the risk-neutral transition PDF of the stock price GBM process with drift r − q, i.e., with r replaced by r − q in (12.16). The generator for the stock price process with SDE in (12.46) is defined by . Hence, the respective Black–Scholes partial differential equations in (12.17) and (12.18) are now

subject to ν(0, S) = Λ(S) and

subject to V(T, S) = Λ(S). Note that the dividend only changes the drift term where has been replaced by . Everything else is the same, including the discount factor. Equations (12.19) and (12.20) are then also the same, i.e., the delta hedge position is the same. Of course, the derivative value V(t, S) for q ≠ 0 differs from the value when q = 0.

We now show that the derivative pricing formula for q ≠ 0 (nonzero stock dividend) obtains trivially from the corresponding pricing formula for q = 0 (zero dividend), given arbitrary payoff VT = Λ(S(T)). To precisely describe this, let V(t, S; r, q) be the time-t price of the derivative for given interest rate r and stock dividend q. This function has a dependence on parameters r and q, as well as other parameters that we simply suppress. The corresponding price when q = 0 is then V(t, S; r, 0). The function V(t, S; r, q) is given by (12.50) and V(t, S; r, 0) is given by (12.14). Multiplying out the discount factor in both cases gives erτ V(t, S; r, q) = [erτ V(t, S; r, 0)]|r→r− q, which is equivalent to

From this relation we see that the pricing function (on the left) for q ≠ 0 is given by the corresponding pricing function (on the right) for q = 0 after replacing the interest rate r by r − q and multiplying the function by e−qτ , τ = T − t. The simple example below shows how (12.53) is very easily applied to a standard call and put.

Apply the symmetry in (12.53) to (12.27) and obtain pricing formulae for the standard European call for a stock with continuous constant dividend yield q.

Solution. Let C(t, S; r, q) ≡ C(τ, S, K, σ, r, q) denote the pricing formula for the call with stock dividend q. For q = 0, C(t, S; r, 0) ≡ C(τ, S, K, σ, r, 0) is given by (12.27):

Applying (12.53), C(t, S; r, q) = e−qτ C(t, S; r − q, 0) = e−qτ C(τ, S, K, σ, r − q, 0):

where τ = T − t and d±(x, τ) are defined in (12.24).

This example also points out another very useful simple symmetry where the standard option pricing function, for given dividend q, is given by the original (zero dividend) pricing function with spot value S replaced by the “effective spot” value e−qτ S (keeping everything else the same). This is an alternatively useful symmetry that we can apply to immediately obtain the pricing formula for q ≠ 0 by substituting e−qτ S for S within the pricing formula for q = 0. We can express this additional symmetry as

We see quite trivially how this symmetry works in the above example of the call where setting e−qτ S for S in (12.27) gives (12.54). Applying either (12.53) or (12.55) to (12.30) gives the corresponding pricing formula for the put option on a dividend paying stock,

The put-call parity relation in (12.29) now takes the more general form,

where we simply write C(t, S) = C(t, S; r, q) and P(t, S) = P(t, S; r, q).

Corresponding symmetry relations for the delta hedging position also follow. Let us denote . Then,

By the chain rule, differentiating (12.55) gives us an alternative symmetry:

For example, consider a call where (12.34) gives Δc(t, S; r, 0) and by either (12.58) or (12.59):

We point out that this formula can also be obtained using our previous derivations, i.e., without use of the symmetry relation in (12.58).

If we assume no knowledge of the above symmetry and no prior pricing formula for q = 0, then we can of course derive the pricing formula in (12.54) from first principle, by employing the same steps that lead to (12.27) where we had q = 0. Namely, we substitute the expression for S(T) in (12.48) into the discounted expectation in (12.23) and evaluate by using the identities in (12.25) and (12.26) where now the drift r − q replaces r, i.e., (12.25) and (12.26) become

and

Combining these into (12.23) gives the call pricing formula in (12.54). Using similar steps, or by put-call parity, we obtain the above put pricing formula. The pricing formulae for European derivatives on a dividend paying stock for all other types of payoffs, including those we considered in Sections 12.1.3 and 12.1.4, also follow by the above symmetry relation. Alternatively the formulae can be derived from first principles based on the identities in (12.61) and (12.62). In the case of power options on a dividend payoff stock, we have the identities in (12.40), (12.41), and (12.42) where r is replaced by r − q (or equivalently do not replace r but replace S by e−qτ S).

[Technical Remark: We now give a more technical argument showing that the above symmetry relation in (12.53) holds as a particular case of a similar symmetry for more complex path-dependent payoffs. Consider an arbitrary European derivative where the payoff VT has a path dependence on the stock, i.e., is a functional of the stock price process from time t to T. Examples of these derivatives are barrier options, Asian options, lookback options, etc. In general, the derivative price Vt is an ℱt-measurable random variable where (12.9) holds for any attainable claim VT. More specifically, denote by {S(r − q)(u) : t ≤ u ≤ T} the path of the stock price process defined by the risk-neutral drift parameter r − q (and volatility σ) and let Vt = Vt(r, q) be the corresponding derivative price at time t, for any constant interest rate r and constant dividend yield q. Now, let VT depend on any segment of the stock price path, including the entire path history from time t to T. We write this as a functional, VT(r, q) = F{S(r − q)(u) : t ≤ u ≤ T}. Note that VT(r − q, 0) = F {S(r − q − 0)(u) : t ≤ u ≤ T} = VT(r, q). Hence, by (12.9),

So (12.53) is recovered for standard non-path-dependent payoffs with spot S(t) = S giving Vt(r, q) = V(t, S; r, q). However, we note that the relation in (12.55) does not generally hold for path-dependent derivative pricing.]

12.1.5.2 The Case of Discrete-Time Dividends

The continuous-time dividend payment model of a stock in the previous section led to analytical pricing formulae for European derivatives that have the same form as the formulae with zero dividend. We shall mostly adopt this model in further applications. In practice, however, stocks in the market pay dividends at discrete regular intervals of time. Let’s suppose that at present time t0 < T we know the fixed future dividend dates, Ti, i = 1, ... , N, t0 < T1 < ... < TN ≤ T. At each time Ti the dividend payment div(Ti) is a proportion of the stock value at time Ti, i.e., div(Ti) = diS(Ti), where 0 ≤ di ≤ 1 is the dividend percentage. When no dividend is paid at time Ti we have di = 0 and when the full share value of the stock is paid at time Ti then di = 1 and the stock becomes worthless for all time after Ti. Typically, we can assume 0 < di < 1 for i = 1, ..., N. We remark that by writing di = qi (Ti − Ti−1) then qi is a dividend yield (rate) that is fixed within the time interval (Ti−1, Ti].

The model for the stock is then as follows. Between the ith dividend date and just before the (i + 1)th dividend date, i.e., within any time interval between dividend payments, the stock price evolves simply as a GBM according to the SDE in (12.1). Hence the stock price at time t0 ≤ t < T1 is given in terms of the spot S(t0) ≡ S0 as

At time t = T1−:

where we use the notation for i = 1, . . . , N. For times t ∊ [Ti−1, Ti), i = 2, ..., N, we have

and in particular for t = Ti−, just before the ith dividend date,

Finally, for the last interval [TN, T],

Now, at each dividend payment date Ti, i = 1, ..., N, the stock price instantaneously decreases by a fraction di due to the dividend payment. This is expressed as

Hence, substituting the expression for S(Ti−) in (12.64) into this last equation gives the evolution of the stock price from one discrete dividend date to the next as

For time t0 to just after the first dividend payment time T1 we have

Multiplying out the stock price ratios for all adjoining time intervals including the first and last interval (note: this is a telescoping product) gives

where . In the last line we simplified the sum in the exponents where .

From (12.68) we see that the stock price S(T) is a GBM random variable with drift r and volatility σ. The overall discount factor due to all the dividends is multiplying the actual initial stock price S0 giving the initial value now acting as effective initial stock price at time-t0. We recall that in the case of a continuous dividend the quantity e−qτ S0 acts in the place of when pricing a non-path-dependent European derivatives. Hence, all the time-t0 pricing formulae for non-path-dependent (standard) European derivatives on the stock are obtained by using the initial value in the place of S0. This is clear by substituting the time-T stock price expression in (12.68) into the risk-neutral pricing (expectation) formula with (non-path-dependent) payoff VT = Λ(S(T)). In particular, let V(t0, S; d) represent the European pricing formula for the above stock model with discrete dividends, within the time interval (t0, T), grouped in a vector d = (d1, ..., dN). Accordingly, let V(t0, S) ≡ V(t0, S; 0) be the pricing function for zero dividends. Then, the analogue of (12.55) is the relation

The pricing functions for a standard call option, put option, power option, etc., follow immediately based on the formulae for zero dividends. For example, simply setting the spot value to in (12.27) gives the pricing formula for the time-t0 call option with discrete dividends d1, ..., dN within the time to maturity τ = T − t0:

where

12.2 Forward Starting and Compound Options

We are now equipped to readily develop pricing and hedging formulae for other classes of options besides the standard European options considered so far where we assumed a payoff VT = Λ(S(T)). Rather than having a payoff that depends solely on the terminal stock price S(T) at maturity T, there are European-style options that can have stipulations at a finite number of intermediate dates within the lifetime of the option. These types of options are examples of what can be termed multistage options. As in most options, there are simpler and more complex versions of these contracts.

Examples of simpler contracts are forward starting options with one intermediate date T1 < T. The holder enters the contract at a time t < T1 such that at time T1 the contract has the value of an option (say a European call) on an underlying stock which expires at T. Generally we can represent the option value at time T1 as a function of . The time-T payoff, VT = Λ(S(T1), S(T)), of the option can depend upon S(T1) and S(T). By risk-neutral pricing we have (discounting from T back to T1)

Let V(t, S) ≡ V(t, S; T1, T) denote the time-t value of the forward starting option with given spot S(t) = S. By the Markov property of the stock price process, conditioning on ℱt reduces to conditioning on S(t). Applying again the risk-neutral pricing formula (discounting from time T1 to t) and the tower property4 finally gives us the time-t price as a single conditional expectation discounted from T to t:

For instance, in a forward starting call the holder enters the contract at a time t < T1, prior to an intermediate date T1, whose value at time T1 is a call on an underlying stock initiated at the “forward” time T1. The call initiated at time T1 expires at date T > T1 and has some strike specification, which is generally a function of the stock price S(T1) (i.e., the strike is not a constant specified value). Specifically, the forward starting call can be specified as having strike , then Λ(S(T1), S(T)) = (S(T) − S(T1))+. Hence, as viewed at present time t, the strike is a random variable corresponding to the price of the stock at time T1. Inserting the payoff into (12.72) gives the time-t price of this forward starting call

Let’s assume the stock price is a GBM given by (12.2) with zero dividend. The addition of a continuous constant dividend yield q on the stock can be done trivially by applying the symmetry relation in (12.53) to the resulting pricing formula. The above expectation is readily evaluated by writing the payoff as

where random variable is independent of S(T1). Hence, using the tower property in reverse gives a nested expectation with an inner expectation conditional on S(T1) as in (12.72):

Here we pulled S(T1) out of the inner expectation as it is -measurable; then the inner condition is dropped since Y is independent of S(T1), and finally the unconditional expectation is a constant that is factored out of the expectation conditional on S(t) = S. Note that we have also factored the discount term into two parts. The first term on the right in (12.73) is recognized as the Black–Scholes price of a call with no dividend, time to maturity T − T1, effective strike and spot of unity:

where

The second term in (12.73) gives the spot S since . Multiplying the expression in (12.74) by S produces the pricing formula:

We observe that this pricing function is linear in the spot S since the term in square brackets depends only on parameters r, σ, T1,T . The delta hedge is then trivially given by the term in brackets, . This is a constant hedge position having no dependence on time t and spot S. What is then interesting is that this forward starting call can be hedged statically in time! Other related forward starting option problems are left as exercises for the reader (see Exercises 12.19 and 12.20).

We now consider the problem of pricing a more complex class of options known as compound options. As the name implies, such contracts are options on options. Here we shall assume the simplest types of compound options that involve an (outer) option to buy or sell another (inner or embedded) option at some future time. For standard European-style options the payoff is simply a function of the underlying stock price at some expiry time T > t where t is current calendar time. In a compound option the essential difference is that its value at some future time, say T1 > t, is a specified function of an option price on an underlying stock whereby the latter option is initiated at time T1 and matures at a future time T2 > T1 with a specified payoff function. In a compound option, the role of an underlying asset is not played by the stock but rather the embedded option on the stock plays the role of “underlying asset” for the (outer) option.

Generally, a European compound option is defined by an outer payoff function φ(1) and inner payoff function φ(2). We are interested in pricing the compound option at time t < T1. Given t < T1 < T2, let Vt = V(S(t), t, T1, T2), t ≤ T1, be the value process of the compound option. Note that we have also denoted this as a function of given exercise times T1, T2. At time T1, with stock price S(T1), the value of the compound option is given by , where V(2)(S(T1), T1, T2) is the value of the underlying (inner) option at time T1 with time to expiry T2 − T1 and payoff value V(2)(S(T2), T2, T2) = φ(2)(S(T2)). Note that V(2)(S(T1), T1, T2) is an ordinary function of the random variable S(T1) and can be viewed as a random asset value at time T1. Given spot S(t) = S, then by the risk-neutral pricing formulation the arbitrage-free price of the compound option is given by the conditional expectation (under the risk-neutral measure ) of the discounted value, , of the payoff of the outer option at time T1:

where

The order of the steps for obtaining the price V(t, S; T1, T2) by the above expectation approach is as follows.

- Determine the time-T1 price V(2)(S1, T1, T2) of the embedded option on the stock having expiry T2 > T1 and spot variable S1.

- Set S1 = S(T1) to obtain the payoff of the outer option at time T1; as a random variable this payoff is where .

- Compute the discounted risk-neutral expectation in (12.76), i.e., the time-t price is .

The most common examples of European compound options are a call-on-a-call, put-ona-call, put-on-a-put and call-on-a-put. These four options are characterized by two expiration dates T1 and T2 and two strike values K1 and K2 and with respective payoff functions φ(1)(x) = (x−K1)+ and φ(2)(x) = (x−K2)+; φ(1)(x) = (K1 −x)+ and φ(2)(x) = (x−K2)+; φ(1)(x) = (K1 −x)+ and φ(2)(x) = (K2 −x)+; φ(1)(x) = (x−K1)+ and φ(2)(x) = (K2 −x)+. For example, the call-on-a-call contract gives the holder the right (but not the obligation) to buy an underlying call option for a fixed strike price K1 at calendar time T1 and where the underlying call is specified by strike K2 and time to expiry T2 − T1.

As a concrete example, let us specifically value the call-on-a-call option by implementing (12.76) within the usual GBM process for the stock price process having dividend q in an economy with constant interest rate r. Denote the value of the underlying call at time T1 by . Hence, in (12.76) is given explicitly by the standard call price formula, i.e., for time-T1 spot value S(T1) = S1 > 0 and time to maturity T2 − T1:

where . Throughout this section, we define

From (12.76), the call-on-a-call option value, denoted by Vcc(S, t), is given by

Note that the random variable within this expectation is nonzero only when . Recall that the call pricing function is a strictly increasing function of the spot variable S1 where , as S1 → 0+, and , as S1 → ∞. The graph of versus S1 must therefore cross the level K1 > 0 at exactly one (critical) point, i.e., at S1 = S1*. This point is the root of the equation

Note that by (12.78) we see that this is a nonlinear algebraic equation so that S1*, being a function of K1, K2 and T2 − T1, is in practice obtained numerically. Given the point S1*, and since is strictly increasing in S1, we have the equivalence , hence

So (12.80) now reads

where we define τ1 := T1 − t and τ2 := T2 − t in what follows.

The two conditional expectations in (12.81) are readily evaluated by using the strong solution representation of the stock price process. In particular, the second expectation is evaluated using

and the fact that and are independent. Hence, and S(t) are independent, giving

where we denot . The last equality follows since under measure .

The first conditional expectation in (12.81) is re-expressed as follows:

Note that in the third line from the top we have moved the indicator random variable to the inside of the inner expectation since it is known at time T1 (i.e., it is σ(S(T1))-measurable). In the third line we have altogether eliminated the inner conditional expectation (i.e., the conditioning on S(T1)) simply by using iterated conditioning (i.e., the tower property). The two conditional expectations in the last equation line of (12.84) are evaluated as follows. The last expectation is a joint probability. Upon using the condition S(t) = S, the fact that S(T1)/S(t) and S(T2)/S(t) are both independent of S(t), and using (12.82) and

we have

where . Since the increments and are Norm(0, τ1) and Norm(0, τ2), respectively, the random variables and are both standard normals under the risk-neutral measure . Moreover, using the independence of nonoverlapping Brownian increments, their covariance (in the -measure) is given by

Hence the vector (Z1, Z2) has standard normal bivariate distribution with correlation coefficient . By symmetry, (−Z1, −Z2) has the same bivariate distribution. Hence, (12.86) gives

Following similar steps as led to (12.86) above, and inserting the exponential form in (12.85) for S(T2) where S(t) = S, the second to last conditional expectation in (12.84) is now conveniently rewritten in terms of Z1 and Z2 and evaluated:

We note that in evaluating the last expectation we used the identity in (A.13) of the Appendix.

Finally, by combining the expressions in (12.89), (12.88), (12.84), and (12.83) into (12.81) gives the explicit formula for the compound call-on-a-call:

where a±, b±, ρ are defined above. Note that the option value is a function of the spot S, the two strike values K1, K2, and the two time to expiration values τ1, τ2.

The other types of compound options can be valued in similar fashion. For example, we leave the valuation of the put-on-a-put as an exercise. There also exists a form of put-call parity among some pairs of compound options. In particular, the call-on-a-call option value and the corresponding put-on-a-call option value Vpc(S, t) are related by

Namely, the difference in the time-t value of the call-on-a-call and put-on-a-call (with spot S(t) = S and given inner and outer strike and maturity pairs K1, T1 and K2, T2) is simply the time-t value of a standard call (with spot S(t) = S, strike and maturity K2, T2) minus the discounted inner strike value e−rτ1 K1. This is shown as follows. According to (12.76), the put-on-a-call option has value

where is the value of the (inner) call option initiated at T1 and maturing at T2 > T1. Using the simple identity within the above expectation gives

The first expectation is Vcc(S, t). By the tower property, we now show that the second expectation reduces to the value Ct(S, K2, T2) of a standard call with spot S, strike K2, and maturity T2 >t. Note that the call value is a random variable expressed here as function of the time-T1 spot random variable S(T1), and hence its value is given by the discounted expected value of the payoff (S(T2) − K2)+ at time T2, conditional on S(T1):

Substituting this representation for into the second expectation in (12.92) and invoking the tower property, while combining the discount factors, gives

Hence (12.91) is recovered from (12.92).

Another way to obtain (12.93) is simply to note that the discounted call price process e−rtCt ≡ e−rtC(S(t), K2, T2), for t < T2 and fixed K2, T2, is a martingale under the risk-neutral measure . Hence, combining the -martingale and Markov properties:

Then, setting S(t) = S gives (12.93). We remark that the above put-call parity type relation is valid for quite general models of the stock price process, i.e., it holds for GBM and other models where we assume the discounted stock price process is a martingale under the risk-neutral measure and the stock is not allowed to default. Of course, under more general models the pricing formulas for the compound options will not involve univariate and bi-variate standard normal CDFs as we derived above for the GBM model. With the exception of some families of alternative models, one has to resort to numerical methods for pricing compound options under more complex stochastic models for the stock.

12.3 Some European-Style Path-Dependent Derivatives

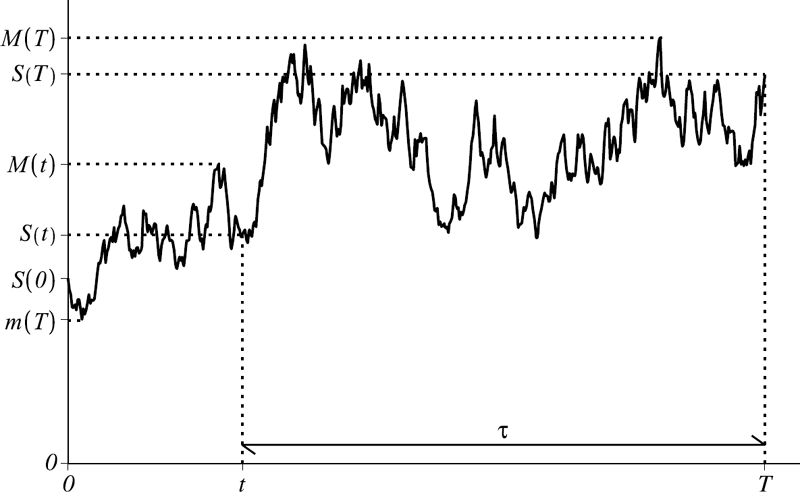

We now consider the application of risk-neutral pricing to path-dependent European options whose payoff is dependent on the underlying stock price history over the lifetime of the contract. We shall specialize to the pricing of two types of path-dependent options, namely, barrier options and lookback options. As seen in the examples below, these classes of options have a payoff that is a function of a combination of the stock price S(T) at maturity T > 0 and the realized (sampled) maximum MS(T) or the realized minimum mS(T) of the stock price process {S(t)}t≥0 where

for all 0 ≤ t ≤ T. There are many variations of the payoff for these options. Some payoffs, such as in the case of a so-called double barrier option, are functions of the triplet MS(T), mS(T), S(T). Here we shall focus our attention on developing analytical pricing formulae for single-barrier options and lookback options whose payoff is either a function of the pair MS(T), S(T) or a function of the pair mS(T), S(T), separately. Given the joint distribution of either pair of random variables, there are two main types of payoffs for which we can in principle derive pricing formulae. In the first case, the payoff is assumed to be a (Borel) function, φ : R+2 → ℝ, of the terminal stock price and its realized maximum and in the second case it is a function of the terminal stock price and its realized minimum:

Let’s first take a look at the payoffs that define some single-barrier option contracts. For such contracts the payoff simplifies into a product of a function of the terminal stock price Λ(S(T)) and an indicator function involving either the realized maximum MS(T) or minimum mS(T) of the stock price during the option’s lifetime. There are two basic types of single-barrier options: (i) knock-out options that have a nonzero payoff only if a level B > 0 is not attained and (ii) knock-in options that have a nonzero payoff only if level B is attained during the option’s lifetime. The different versions of these correspond to whether level B is a lower barrier or an upper barrier. Letting Λ(S(T)) be the effective payoff of a standard (non-path-dependent) European option, e.g., Λ(x) = (x − K)+ for a call and Λ(x) = (K − x)+ for a put struck at K > 0, we have the following four different payoffs for a single barrier at level B:

- (a)Up-and-out: where

- (b)Down-and-out: where

- (c)Up-and-in: where

- (d)Down-and-in: where

For example, an up-and-out call with strike K is defined as having the payoff of a call, (S(T) − K)+, if the realized maximum value of the underlying stock price stays below the barrier level B and has otherwise zero payoff if the stock price attains or goes above level B at any time until T. See Figure 12.3. We write this as , where φ(M, S) = (S − K)+ ?{M < B}. The down-and-out call has payoff . In the case of a knock-out put, the up-and-out put has payoff and the down-and-out put has payoff . See Figure 12.4.

Two types of stock price paths starting at S(0) < B are depicted for an up-and-out call with strike K. Only paths in the set {MS(T) < B; S(T) > K}, i.e., paths that do not surpass level B and also end up above the strike at terminal time T give a positive payoff for an up-and-out call struck at K.

Two types of stock price paths starting at S(0) > B are depicted for a down-and-out put with strike K. Only paths in the set {mS(T) > B, S(T) < K}, i.e., paths that do not fall below level B and also end up below the strike at terminal time T give a positive payoff for a down-and-out put struck at K.

On the other hand, an up-and-in call with strike K is defined as having a call payoff if the stock price has attained or has gone above B at any time until T and has otherwise zero payoff, i.e., the payoff is . Similarly, a down-and-in call has a payoff that is nonzero only if the stock price has fallen below or at level B, . For the up-and-in put and down-and-in put, with strike K, we have and , respectively.

There is a very simple and useful symmetry relation between the knock-in and knock-out payoffs. Since we have the obvious relations

then

This is known as “knock-in-knock-out” symmetry. By computing the pricing formula for the knock-out (or knock-in) option then the pricing formula for the corresponding knock-in (or knock-out) follows simply by subtracting the former from the price of the standard European option having payoff Λ(S(T)). That is, letting VtUO, VtUI, VtDO, VtDI represent the respective time-t barrier option prices, t ≤ T, then by risk-neutral pricing we have

where Vt is the time-t price of the standard European option with payoff Λ(S(T)).

We now turn to the definition of lookback options in the continuous time setting. We recall from the discrete-time setting (see Section 7.6.2 of Chapter 7) that there are two main kinds of lookback options, with either floating strike (LFS) or floating price (LFP). We list the four common lookback option payoffs:

- (a)Floating strike call (LFS call):

- (b)Floating strike put (LFS put):

- (c)Floating price call (LFP call):

- (d)Floating price put (LFP put):

Note that the LFS options are never out of the money since mS(T) ≤ S(T) ≤ MS(T). For an LFS option the strike price is floating as it is not preassigned but rather determined by the realized maximum or minimum value of the stock during the lifetime of the option. The payoff of an LFS option is the maximum difference between the stock’s price at maturity and the floating strike. The LFS call gives its holder the right to buy at the lowest stock price realized during the option’s lifetime, whereas the LFS put gives the right to sell at the highest realized stock price. For the LFP options, the payoffs are the maximum differences between the optimal (maximum or minimum) stock price and the fixed strike K. LFP options are designed so that the call (or put) has a payoff given by the stock price at its highest (or lowest) realized value during the option’s lifetime.

12.3.1 Risk-Neutral Pricing under GBM

Before specializing and thereby simplifying the problem to the pricing of barrier options and lookback options, covered in Sections 12.3.2 and 12.3.3, we now present the risk-neutral pricing formulation for the two general types of payoffs in (12.95) above. We assume {S(t)}t≥0 to be a GBM given by (12.2) if q = 0 or (12.47) if q ≠ 0. The stock price in (12.47) is given by a strictly increasing exponential mapping

where the drifted -BM process X is defined by (see (10.68) of Section 10.4.3)

Note that for the zero dividend case. Hence, the realized maximum and minimum of the stock price in (12.94) are related trivially to the maximum and minimum of the drifted BM:

where (see (10.70))

In what follows we will be conditioning on ℱt for any fixed current time t, 0 ≤ t ≤ T. By the time homogeneity property of the stock price process, it is convenient to define τ := T − t. Let us first consider expressing the joint random variables MS(T), S(T) as functions of the ℱt-measurable random variables MS(t), S(t). Using (12.100) the stock price at time T is

where we define . Note that the process , for fixed t, is a standard -BM ; hence is the drifted BM, . The realized maximum of the stock price up to time T is the larger of the realized maximum up to time t and the realized maximum from time t to T :

where . To arrive at the last term, we employed the steps:

By similar steps, the sampled minimum of the stock price takes the form

where .

Based on (12.105) and (12.107), {(MX(t), X(t))}t≥0 and {(mX(t), X(t))}t≥0 are both (vector) Markov processes. Observe that both pairs of random variables Mχ(τ), X(τ) and mχ(τ), χ(τ) are ℱt-independent (and hence also independent of the random variables S(t), mS(t), and MS(t)). Moreover, both pairs of random variables have the same joint distribution as (MX (τ), X(τ)), and (mX (τ), X(τ)), respectively. In particular, the joint PDF of Mχ(τ), χ(τ) (in the risk-neutral measure ) is given by (sending t → τ and µ → ν in (11.109) of Chapter 11)

for −∞ < x < w, w > 0 and zero otherwise. The risk-neutral joint PDF of mχ(τ), χ(τ) is given by (sending t → τ and µ → ν in (11.110) of Chapter 11)

for x > w, w < 0 and zero otherwise.

By the joint Markov property and using (12.104) and (12.105), a European option with payoff (i) in (12.95) has time-t no-arbitrage price (expressed as an ℱt-measurable random variable) given by

For any positive real values MS(t) = M, S(t) = S > 0, M ≥ S, i.e., the spot values of the sampled maximum up to calendar time t and the stock price at calendar time t, the general pricing formula is obtained by computing this expectation while using the fact that are ℱt-independent:

where τ = T − t is the time to maturity. This is a double integral of the joint density in (12.108) multiplied by the effective payoff, h(w, x) := φ(max{M, S eσw}, S eσx), which is a function of w, x.

Applying the same steps by using (12.104) and (12.107), the time-t no-arbitrage pricing formula for the European option with payoff (ii) in (12.95) for given real positive spot values, 0 < mS(t) = m ≤ S = S(t), is given by

τ = T − t. This is now a double integral involving the joint density in (12.109) and the effective payoff given by g(w, x) := φ(min{m, S eσw}, S eσx).

[We remark that one can always generally write a stock price as in (12.100), using an exponential (monotonic) function of a Markov process X which is specified as a more complex process. Then, the pricing formulae in (12.111) and (12.112) can be used for more general stock price models as long as there exist joint densities and and also that the discounted stock price process is a -martingale. Of course, for a more general stock price model that is not a GBM process, the process X is not specified simply as a drifted BM but as a more complex process. The joint densities for such processes will also be more complex than those for drifted BM given in (12.108) and (12.109).]

Note that both pricing formulae in (12.111) and (12.112) are functions of τ = T − t. For example, we can write the price in (12.111) as a function ν(τ, S, M) where ν(τ, S, M) = V(t, S, M) = V(T − τ, S, M) and similarly for the pricing function in (12.112). Note that the above pricing formulae are generally valid for any intermediate time and that the spot values S(t) = S, MS(t) = M, mS(t) = m are known at intermediate time t. However, the payoff is generally a function of the realized maximum MS(T) (or minimum mS(T)) involving the continuous sampling of the stock price starting at a prior time t0 = 0. These are therefore referred to as “seasoned” contracts. This general situation is depicted in Figure 12.5.

A sample stock price path is shown with its initial value, its value and realized maximum and minimum at both the intermediate (current) time t and at terminal time T.

Let’s now specialize to the case where the realized maximum and minimum are computed starting from current time t. Then S(t) = MS(t) = MS(t), i.e., with spot values S = M = m, where in the integrands of (12.111) and (12.112) we have, respectively,

Hence both payoff functions in (12.111) and (12.112) have the form φ(S eσw,S eσx) and the option pricing formulae are functions of only the spot S and τ = T − t. In particular, the pricing formula in (12.111) is reduced to V(t, S, M) = V(t, S) = ν(τ, S):

Setting the current calendar time t = 0, S = S(0) = S0, τ = T gives the price expressed as function of spot S0, and the time to maturity, which is now represented by the variable T, V(0, S0) = ν(T, S0):

Of course, we need only compute one of these as (12.114) obtains trivially from (12.113) and vice versa. For options involving the realized minimum, (12.112) gives V(t, S, m) = V(t, S) = ν(τ, S):

or expressed as a function of T and S(0) = S0, where we simply make the variable replacements S → S0 and τ → T in the derived pricing function ν(τ, S).

12.3.2 Pricing Single Barrier Options