114 115

how finance works

Financial accounting

Case study: operating costs

This table breaks down the company’s operating costs in more detail. It is important to

read any notes regarding depreciation and ordinary and extraordinary costs and gains.

Manpower costs 51.7 45.3

Materials and consumables 29.1 26.7

Other operational costs 67.6 63.8

Depreciation 120.3 114.0

Amortization of grants and contributions (0.8) (0.8)

Loss/(gain) on disposals of fixed assets 0.2 (0.5)

268.1 248.5

Operating leases for plant and machinery 1.5 1.2

Research and development 0.1 0.1

Directors’ remuneration 2.1 1.8

Fees paid to the auditor 0.2 0.2

Manpower costs including basic pay

and pensions, overtime payments,

staff training, and maternity leave

Term given to the gradual decline in an

asset’s value, caused by factors such as

wear and tear and market conditions.

Decrease in value over time of

intangible assets or loans

Leasing costs for buildings

and equipment

Research and development carried

out to improve the reliability and

effectiveness of services

Directors’ remuneration including

base salaries and benefits, pensions,

car and health benefits, share options,

and bonuses

Year 2013

£m

Year 2012

£m

Payroll

Salaries and wages paid to staff, temporary

contractors, and indirect labor

Utilities

Water, electricity, and gas; postage and

shipping; transportation

Insurance

Insurance on fixed assets and personal

liability insurance for employees

Phone/internet bills

Cost of telephone, broadband internet,

and mobile devices used by employees

Advertising

Sales and marketing of the company and

its products

Office supplies

Stationery such as pens, paper, and filing

systems, office printers, furniture, lighting

Legal fees and professional services

Accounting and legal fees, payable to

accountants, auditors, and legal advisers

Interest on loans

Interest paid on money borrowed, which

counts as a business expense

Tax

Varying among jurisdictions, this may

include payroll tax and corporation tax

Entertainment

Legitimate costs of business entertaining,

subject to certain criteria being met

TYPICAL EXPENSES

Figures in parentheses represent negative numbers.

Profit or loss on the sale of fixed assets

%

$

$

$

US_114-115_Profit_and_loss.indd 115 21/11/2014 14:24

How it works

The balance sheet essentially

shows what the company owns,

what it owes, and how much is

invested in it. It is based on the

accounting formula, sometimes

called the balance-sheet equation,

which is the basis of double-entry

bookkeeping. This shows the

relationship between assets,

liabilities, and owners’ capital—

what the company owns (assets)

is purchased either through debt

(liability) or investment (capital).

The equation always balances, as

everything a company owns has to

have been bought with its owner’s

funds or through borrowing.

Balance sheet

A balance sheet is a financial statement that shows what a business is

worth at a specific point in time. Its primary purpose is to show assets,

liabilities, and equity (capital), rather than financial results.

Deferred income Income a

company receives for goods

or services that have not yet

been delivered or provided. Until

income is received it is recorded

on a balance sheet as a liability.

NEED TO KNOW

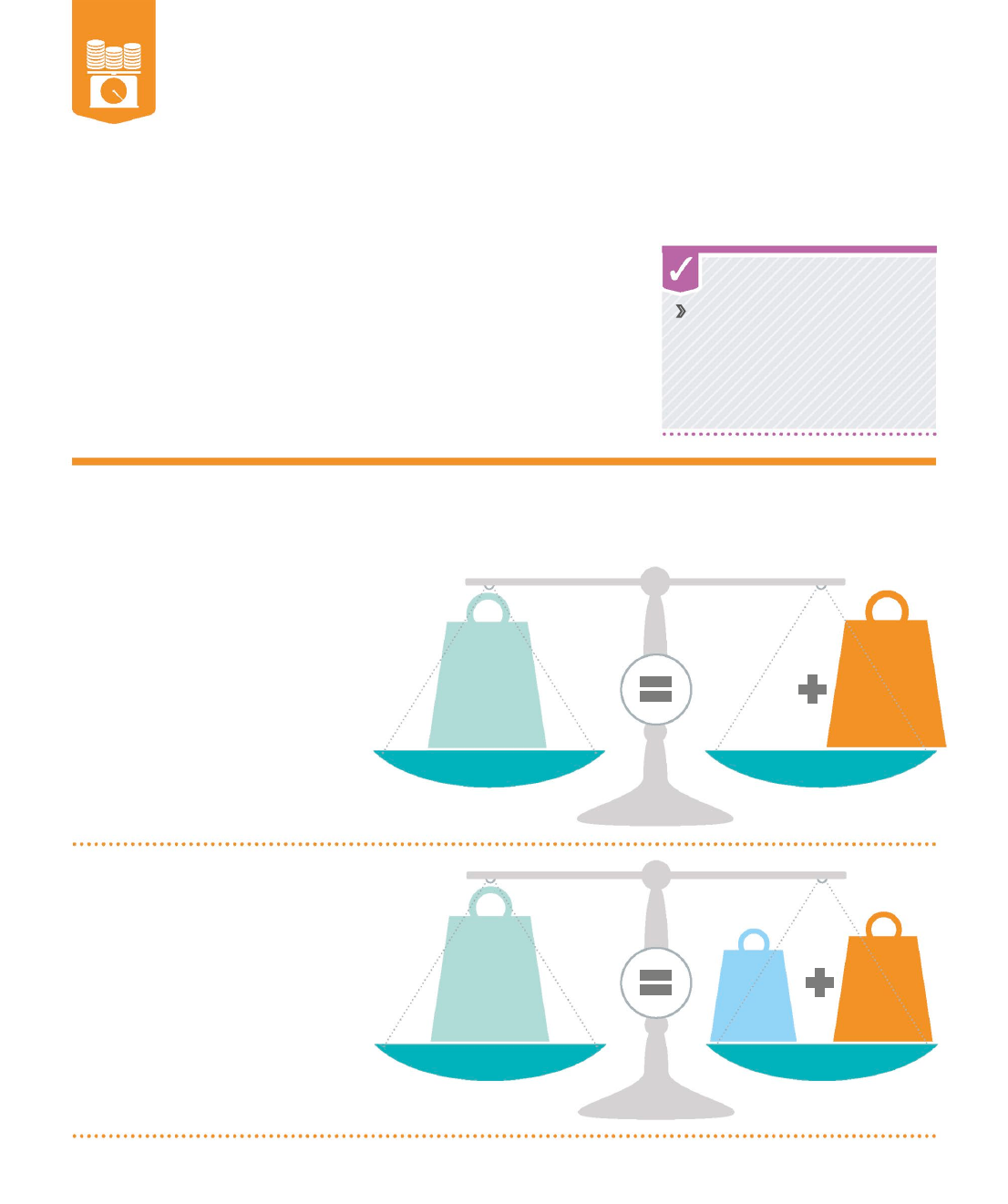

The balance-sheet equation

As the name suggests, the balance sheet must always balance. This is

because everything the business owns (its assets) must be offset against

the equivalent capital (or equity) and liabilities (debt).

ASSETS

$1,000

ASSETS

$1,000

CAPITAL

$600

LIABILITY

$400

LIABILITY

$0

CAPITAL

$1,000

Company incurs $400

in liabilities

After spending $400 on, for example,

an illuminated sign for the storefront,

the owner incurs $400 in liabilities and

so the formula changes. However, since

the sign is worth $400, and the owner

has $600 remaining, the equation

remains balanced—as it always does.

Company has no liabilities

For example, a young business may

have assets of $1,000. It currently has

no liabilities so its capital is equal to

its assets—that is, it is the amount of

equity the owners or shareholders

have invested in the business. Using

the accounting formula, the equation

would look like this:

US_116-119_Balance_sheets.indd 116 15/12/2014 12:57

116 117

HOW FINANCE WORKS

Financial accounting

Case study: balance sheet

This example from Wessex Water, a UK public utility company, shows how a balance

sheet works in practice (at the time, the exchange rate was £1 = $1.58).

Fixed assets

Tangible assets 2,167.1 2,069.2

Investments – –

Current assets

Stock and work in progress 7.0 6.3

Debtors 162.6 153.9

Cash in the bank and in hand 181.0 211.0

350.6 371.2

Creditors—amounts falling due within one year (198.8) (171.7)

Creditors—amounts falling due after more (1,891.5) (1,811.9)

than one year

Provisions for liabilities and charges (114.9) (115.3)

Retirement benefit obligations (93.1) (83.0)

Deferred income (17.2) (17.9)

Capital and reserves

Called-up equity share capital 81.3 81.3

Profit-and-loss account 120.9 159.3

Net assets 202.2 240.6

Shareholders’ funds 202.2 240.6

Net current assets 151.8 199.5

Total assets less current liabilities 2,318.9 2,268.7

Current assets are assets that last

one year or less, and can be easily

converted into cash. Cash, cash

equivalents, and inventory are

the most common current assets

Creditors are the individuals or

organizations to which the company

owes money. Here, the money must

be repaid in the current financial year

Net current assets equal current

assets after money due to creditors

within one year has been deducted

Total assets less current liabilities

is the sum of fixed and net current

assets minus liabilities due within the

current financial year

Fixed assets (or non-current assets)

are not easily converted into cash

and usually last longer than one

year. They are either tangible, such

as land, or intangible, such as a logo

Net assets are what is left once

liabilities have been deducted from

the company’s fixed and net current

assets to give the overall net assets

Shareholders’ funds, or owner’s

equity, is the remaining capital;

this money can be reinvested

into the business or paid out as

an annual dividend

Year 2013

£m

Year 2012

£m

ASSETS, LIABILITIES, AND CAPITAL

Liabilities due in more than one

year are amounts due to creditors,

which are deducted from total fixed

and net current assets

SYMBOLS FOR DEBITS AND CREDITS

Accountants use a number of different terms and symbols to indicate debits and credits.

Some use “Dr” for debits and “Cr” for credits, others use “+” for debits and “–” for credits.

On this balance sheet, parentheses are used to show credits (negative numbers).

$

US_116-119_Balance_sheets.indd 117 09/11/2016 11:01

116 117

HOW FINANCE WORKS

Financial accounting

Case study: balance sheet

This example from Wessex Water, a UK public utility company, shows how a balance

sheet works in practice (at the time, the exchange rate was £1 = $1.58).

Fixed assets

Tangible assets 2,167.1 2,069.2

Investments – –

Current assets

Stock and work in progress 7.0 6.3

Debtors 162.6 153.9

Cash in the bank and in hand 181.0 211.0

350.6 371.2

Creditors—amounts falling due within one year (198.8) (171.7)

Creditors—amounts falling due after more (1,891.5) (1,811.9)

than one year

Provisions for liabilities and charges (114.9) (115.3)

Retirement benefit obligations (93.1) (83.0)

Deferred income (17.2) (17.9)

Capital and reserves

Called-up equity share capital 81.3 81.3

Profit-and-loss account 120.9 159.3

Net assets 202.2 240.6

Shareholders’ funds 202.2 240.6

Net current assets 151.8 199.5

Total assets less current liabilities 2,318.9 2,268.7

Current assets are assets that last

one year or less, and can be easily

converted into cash. Cash, cash

equivalents, and inventory are

the most common current assets

Creditors are the individuals or

organizations to which the company

owes money. Here, the money must

be repaid in the current financial year

Net current assets equal current

assets after money due to creditors

within one year has been deducted

Total assets less current liabilities

is the sum of fixed and net current

assets minus liabilities due within the

current financial year

Fixed assets (or non-current assets)

are not easily converted into cash

and usually last longer than one

year. They are either tangible, such

as land, or intangible, such as a logo

Net assets are what is left once

liabilities have been deducted from

the company’s fixed and net current

assets to give the overall net assets

Shareholders’ funds, or owner’s

equity, is the remaining capital;

this money can be reinvested

into the business or paid out as

an annual dividend

Year 2013

£m

Year 2012

£m

ASSETS, LIABILITIES, AND CAPITAL

Liabilities due in more than one

year are amounts due to creditors,

which are deducted from total fixed

and net current assets

SYMBOLS FOR DEBITS AND CREDITS

Accountants use a number of different terms and symbols to indicate debits and credits.

Some use “Dr” for debits and “Cr” for credits, others use “+” for debits and “–” for credits.

On this balance sheet, parentheses are used to show credits (negative numbers).

$

US_116-119_Balance_sheets.indd 117 09/11/2016 11:01

BALANCE SHEET

Understanding the notes

The balance sheet is a useful indication of the health

of a business, and it is important that investors know

how to analyze it. It can be read in two ways—“at

a glance,” as on the previous page, where general

information is summarized, or in depth, with more

detailed information about each element. Provided

after the summary, the detailed section of the balance

sheet explains the specific financial workings of the

business in a number of notes. It shows exactly where

money has been gained or lost, in figures, and it

often includes a written commentary about potential

developments that may affect the company, such as

court cases, staffing, or availability of resources.

Cost

As of April 1, 2012 676.3 1,229.7 1,204.6 105.0

93.2 3,308.8

Additions 9.5 67.8 49.1 2.3

96.2 224.9

Transfers on

commissioning 13.7 11.2 42.2 2.8

(69.9) –

Disposals (0.2) - (13.1) (0.5)

– (13.8)

Grants and contributions – (5.0) – –

– (5.0)

As of March 31, 2013 699.3 1,303.7 1,282.8 109.6

119.5 3,514.9

£m £m £m £m

£m £m

LAND AND

BUILDINGS

INFRASTRUCTURE

ASSETS

PLANT,

MACHINERY,

AND

VEHICLES

OTHER

ASSETS

PAYMENTS

ON ACCOUNT AND

ASSETS IN COURSE

OF CONSTRUCTION

Net book value of an asset

is its initial cost minus all its

depreciation to date

Total value of the company’s

fixed assets is listed by

category and in total

Depreciation is the decrease

in value of assets over time

Value of depreciation

of assets is listed by

category and in total

Disposals are any tangible

fixed assets the business has

disposed of or sold this year

Tangible fixed assets

include land and machinery

Additions are new tangible

fixed assets the business

has acquired this year

Combined value of the

company’s tangible fixed

assets in each category,

and also in total, is listed

Depreciation

As of April 1, 2012 211.3 435.5 558.8 34.0

– 1,239.6

Charge for the period 13.7 43.2 56.8 6.6

– 120.3

Disposals (0.1) – (11.5) (0.5)

– (12.1)

As of March 31, 2013 224.9 478.7 604.1 40.1

– 1,347.8

As of April 1, 2012 465.0 794.2 645.8 71.0

93.2 2,069.2

Net book value

As of March 31, 2013 474.4 825.0 678.7 69.5

119.5 2,167.1

Balance-sheet notes

Investors may want to know more about the figures in the summary section, so additional notes and

tables give detailed breakdowns of the figures (at the time, the exchange rate was £1 = $1.58).

Case study: tangible fixed assets

This table presents details of Wessex Water’s tangible fixed assets (long-term assets

that cannot easily be converted into cash).

$

US_116-119_Balance_sheets.indd 118 02/12/2014 14:57

118 119

how finance works

Financial accounting

Cost

As of April 1, 2012 676.3 1,229.7 1,204.6 105.0 93.2 3,308.8

Additions 9.5 67.8 49.1 2.3 96.2 224.9

Transfers on

commissioning 13.7 11.2 42.2 2.8 (69.9) –

Disposals (0.2) - (13.1) (0.5) – (13.8)

Grants and contributions – (5.0) – – – (5.0)

As of March 31, 2013 699.3 1,303.7 1,282.8 109.6 119.5 3,514.9

£m £m £m £m £m £m

Trade debtors 48.9 48.1

Owed by group companies 31.8 35.0

Prepayments and 70.3 62.1

accrued income

Other debtors 11.6 8.7

162.6 153.9

Bank overdraft 21.8 18.6

Inter-company loan - 1.3

Obligations under 7.0 6.3

finance leases

Trade creditors 4.3 3.1

Amounts owed to subsidiary 18.9 14.2

company

Amounts owed to other group 0.6 0.6

companies

Amounts owed to associate 0.7 0.2

company

Dividend 23.3 21.7

Other creditors 2.4 2.0

Corporation tax 16.7 9.2

Taxation and social security 1.9 1.7

Accruals and deferred income 101.2 92.8

198.8 171.7

TOTAL

PAYMENTS

ON ACCOUNT AND

ASSETS IN COURSE

OF CONSTRUCTION

Individuals or entities that

sell assets to third parties on

credit, receiving payment at

a later date

Individuals or entities

that are owed money for

supplying raw materials

or components

Money owed to

related companies

that are owned by

the same group

Prepayments for services

that will be received in the

future, which the business

has already been paid for,

and accrued income that

is expected in the future

Any notes relating

to creditors

The inter company loan was due to a fellow subsidiary

company SC Technology GmbH and has been repaid.

Depreciation

As of April 1, 2012 211.3 435.5 558.8 34.0 – 1,239.6

Charge for the period 13.7 43.2 56.8 6.6 – 120.3

Disposals (0.1) – (11.5) (0.5) – (12.1)

As of March 31, 2013 224.9 478.7 604.1 40.1 – 1,347.8

As of April 1, 2012 465.0 794.2 645.8 71.0 93.2 2,069.2

Net book value

As of March 31, 2013 474.4 825.0 678.7 69.5 119.5 2,167.1

Case study: debtors

Debtors are individuals or entities that owe the business money.

Wessex Water has four categories of debtor.

Case study: creditors

Creditors are individuals or entities that the business

owes money to. They are in credit of Wessex Water.

2013

£m

2012

£m

2013

£m

2012

£m

Tax and employee

benefit payments

Payment to shareholders

Money owed to the bank

$

$

=

US_116-119_Balance_sheets.indd 119 02/12/2014 14:57

118 119

how finance works

Financial accounting

Cost

As of April 1, 2012 676.3 1,229.7 1,204.6 105.0

93.2 3,308.8

Additions 9.5 67.8 49.1 2.3

96.2 224.9

Transfers on

commissioning 13.7 11.2 42.2 2.8

(69.9) –

Disposals (0.2) - (13.1) (0.5)

– (13.8)

Grants and contributions – (5.0) – –

– (5.0)

As of March 31, 2013 699.3 1,303.7 1,282.8 109.6

119.5 3,514.9

£m £m £m £m

£m £m

Trade debtors 48.9 48.1

Owed by group companies 31.8 35.0

Prepayments and 70.3 62.1

accrued income

Other debtors 11.6 8.7

162.6 153.9

Bank overdraft 21.8 18.6

Inter-company loan - 1.3

Obligations under 7.0 6.3

finance leases

Trade creditors 4.3 3.1

Amounts owed to subsidiary 18.9 14.2

company

Amounts owed to other group 0.6 0.6

companies

Amounts owed to associate 0.7 0.2

company

Dividend 23.3 21.7

Other creditors 2.4 2.0

Corporation tax 16.7 9.2

Taxation and social security 1.9 1.7

Accruals and deferred income 101.2 92.8

198.8 171.7

TOTAL

PAYMENTS

ON ACCOUNT AND

ASSETS IN COURSE

OF CONSTRUCTION

Individuals or entities that

sell assets to third parties on

credit, receiving payment at

a later date

Individuals or entities

that are owed money for

supplying raw materials

or components

Money owed to

related companies

that are owned by

the same group

Prepayments for services

that will be received in the

future, which the business

has already been paid for,

and accrued income that

is expected in the future

Any notes relating

to creditors

The inter company loan was due to a fellow subsidiary

company SC Technology GmbH and has been repaid.

Depreciation

As of April 1, 2012 211.3 435.5 558.8 34.0

– 1,239.6

Charge for the period 13.7 43.2 56.8 6.6

– 120.3

Disposals (0.1) – (11.5) (0.5)

– (12.1)

As of March 31, 2013 224.9 478.7 604.1 40.1

– 1,347.8

As of April 1, 2012 465.0 794.2 645.8 71.0

93.2 2,069.2

Net book value

As of March 31, 2013 474.4 825.0 678.7 69.5

119.5 2,167.1

Case study: debtors

Debtors are individuals or entities that owe the business money.

Wessex Water has four categories of debtor.

Case study: creditors

Creditors are individuals or entities that the business

owes money to. They are in credit of Wessex Water.

2013

£m

2012

£m

2013

£m

2012

£m

Tax and employee

benefit payments

Payment to shareholders

Money owed to the bank

$

$

=

US_116-119_Balance_sheets.indd 119 02/12/2014 14:57

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.