124 125

how finance works

Financial accounting

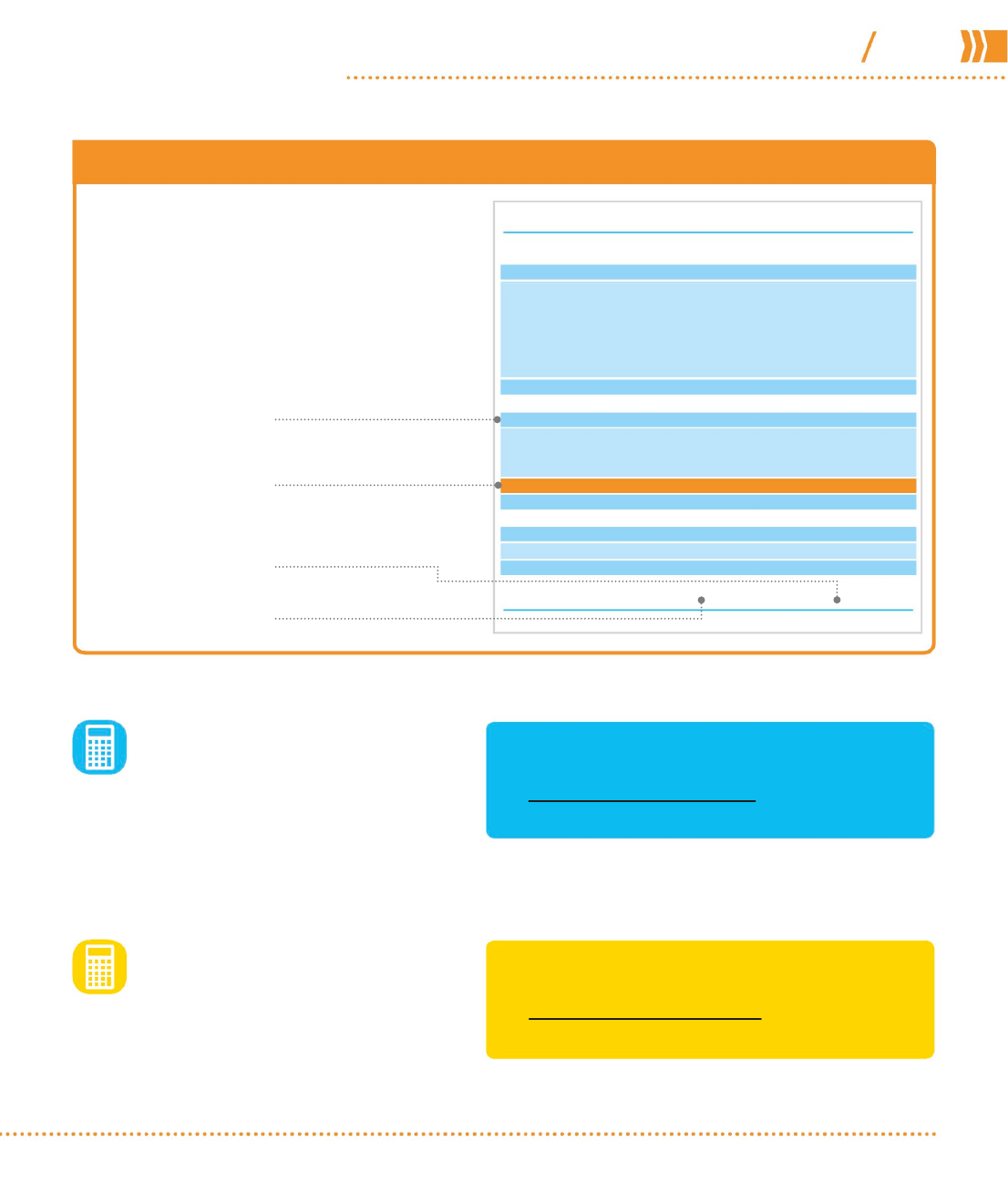

Year 2 After the second year, the

value has depreciated by another

$4,000. The van will lose an equal

amount of value each year for the next

three years of its useful economic life.

Year 3 At the end of the third

year, the van has depreciated

by another $4,000, and its book

value is $13,000, although its

actual value may be more or less.

Year 4 The van

has depreciated by

$4,000, to $9,000,

at the end of four

years of life.

Year 5 By the

end of year five,

the van is valued

at only $5,000—

its scrap value.

RACEHORSES

2 years

COMPUTERS

3 years

OFFICE

FURNITURE

6 years

ROADS

15 years

BOATS

20 years

FRUIT-

BEARING TREES

10 years

Time

(years)

5 15

10 20

$17,000

$13,000

$9,000

$5,000

TIME (YEARS)

2 3 4

5

Typical life of fixed asseTs

Tax authorities often specify the typical useful (economic) life of a particular asset.

This helps to standardize depreciation, and to eliminate uncertainty about value

and the number of years over which an asset can be depreciated.

60%

the value the

average car

loses after

three years

US_124-127_Depreciation.indd 125 21/11/2014 16:23

DEPRECIATION

Sum of the years’ digits

method (SYD)

Depreciation is calculated by dividing each

year of the asset’s life by the sum of the total years to

give a percentage of the depreciable value. If the asset’s

useful life is 5 years, then the sum of the years as digits

is 15 (5 + 4 + 3 + 2 + 1). In year 1, it loses 33 percent

(5 ÷ 15), in year 2, 27 percent (4 ÷ 15), and so on.

Applying depreciation

When calculating depreciation,

there are a number of different

factors to consider. For instance,

a business needs to be able to

predict the number of years an

asset will last. Helpfully, tax

authorities in most countries issue

guidelines to accountants and

businesses with estimates of

the useful economic life of many

common business assets.

Companies may also wonder

which of the many methods of

calculating depreciation to use

for a given asset. Each method

reflects a different pattern of

depreciation, with some being

more suitable for particular

categories of assets. For example,

the “accelerated” methods that

chart rapid depreciation at the

beginning of an asset’s life are

more suitable for technology,

while the “activity” methods that

link depreciation to actual hours

of use or number of units produced

are best suited to transport and

production lines.

Again, tax authorities in most

countries offer guidelines on which

method to use. Although it is

technically possible for a company

to use two different methods for

their own accounting and for tax

purposes, this is best avoided.

(PURCHASE VALUE – SCRAP VALUE)

X

REMAINING USEFUL LIFE

SUM OF THE YEARS’ DIGITS

There are many different methods of calculating depreciation. Some are favored

by particular tax codes, while others are specifically applicable to certain industries

and types of assets, and their patterns of value loss.

Double declining balance method

A method used to claim more depreciation in

the first years after purchase, which is useful for

assets that lose most of their value early on. It reduces a

company’s net income in the early years of an asset’s life,

but generates initial tax savings.

PURCHASE VALUE – SCRAP VALUE

USEFUL ECONOMIC

LIFE (YEARS)

When to use it This accelerated method can be used for assets

that lose most value early on, such as computers or a delivery truck.

When to use it This is another accelerated method that can also

be used for vehicles that lose most of their value early on.

(

X 2 =

ANNUAL

DEPRECIATION

(%)

( )

=

ANNUAL

DEPRECIATION

(%)

)

Other depreciation methods

Misusing depreciation

The wrong method A company

must choose a method that is

permissible for an asset type

Frontloading Opting for an

accelerated method can result in a

taxable gain if an asset is sold early,

for more than its book value

Claiming beyond useful life

Depreciation cannot be claimed

after an asset’s useful life

Ignoring depreciation If a

company fails to claim depreciation,

it has to report a gain from the sale,

despite the loss on deduction

WARNING

US_124-127_Depreciation.indd 126 09/11/2016 11:01

126 127

how finance works

Financial accounting

Hours of service method

The asset’s decline in value is measured

according to the number of actual hours it is

in use. To calculate depreciation using this method,

the company measures the hours of use per year as a

percentage of the estimated total lifetime hours. It is

particularly useful for transportation industries.

Units of production method

When a company uses an asset to produce

quantifiable units, such as pages printed

by a photocopier, it can claim depreciation with this

method, which calculates depreciation according to the

number of units an asset produces in a year.

(PURCHASE VALUE – SCRAP VALUE)

X

UNITS PRODUCED PER YEAR

LIFETIME PRODUCTION

(PURCHASE VALUE – SCRAP VALUE)

X

HOURS USED PER YEAR

LIFETIME HOURS

Previous year’s total

assets can be compared

Total assets are calculated

after depreciation has been

deducted

When to use it This method is typically used by factories to

calculate depreciation on machines that produce units of goods.

When to use it This method may be used to match an airplane’s

flying hours with the revenue generated from those hours.

( )

=

DEPRECIATION

(PER UNIT)

( )

=

DEPRECIATION

(PER HOUR)

Depreciation of fixed

assets is deducted

Fixed assets are shown

distinct from current assets

DEPRECIATION ON THE BALANCE SHEET

A company’s accounts have to list all assets held by the

company, including all fixed assets such as property and

equipment. The accumulated depreciation of these fixed

assets over the year is deducted from their value at the

start of the year to give the year-end total. Without a

depreciation figure, the accounts would give a false

reflection of the finances of the business. The assets

would appear as their original cost value and that might

well exceed their current value.

COMPANY NAME BALANCE SHEET

Assets

Current assets: 2013 2014

Cash 17,467.0 0 8,023.00

Investments 4,853.00 3,367.00

Inventories 1,056.00 2,138.00

Accounts receivable 2,165.00 3,600.00

Prepaid expenses 3,000.00 3,000.00

Other 860.00 976.00

Total current assets 29,401.00 21,104.00

Fixed assets: 2013 2014

Property and equipment 64,553.00 58,219.00

Building/site improvements 4,780.00 2,679.00

Equity and other investments 3,789.00 4,587.00

Less accumulated depreciation 5,625.00 4,171.00

Total fixed assets 67,497.00 61,314.00

Other assets: 2013 2014

Goodwill 1,577.00 1,650.00

Total other assets 1,577.00 1,650.00

Total assets 98,475.00 84,068.00

US_124-127_Depreciation.indd 127 21/11/2014 16:23

126 127

how finance works

Financial accounting

Hours of service method

The asset’s decline in value is measured

according to the number of actual hours it is

in use. To calculate depreciation using this method,

the company measures the hours of use per year as a

percentage of the estimated total lifetime hours. It is

particularly useful for transportation industries.

Units of production method

When a company uses an asset to produce

quantifiable units, such as pages printed

by a photocopier, it can claim depreciation with this

method, which calculates depreciation according to the

number of units an asset produces in a year.

(PURCHASE VALUE – SCRAP VALUE)

X

UNITS PRODUCED PER YEAR

LIFETIME PRODUCTION

(PURCHASE VALUE – SCRAP VALUE)

X

HOURS USED PER YEAR

LIFETIME HOURS

Previous year’s total

assets can be compared

Total assets are calculated

after depreciation has been

deducted

When to use it This method is typically used by factories to

calculate depreciation on machines that produce units of goods.

When to use it This method may be used to match an airplane’s

flying hours with the revenue generated from those hours.

( )

=

DEPRECIATION

(PER UNIT)

( )

=

DEPRECIATION

(PER HOUR)

Depreciation of fixed

assets is deducted

Fixed assets are shown

distinct from current assets

DEPRECIATION ON THE BALANCE SHEET

A company’s accounts have to list all assets held by the

company, including all fixed assets such as property and

equipment. The accumulated depreciation of these fixed

assets over the year is deducted from their value at the

start of the year to give the year-end total. Without a

depreciation figure, the accounts would give a false

reflection of the finances of the business. The assets

would appear as their original cost value and that might

well exceed their current value.

COMPANY NAME BALANCE SHEET

Assets

Current assets: 2013 2014

Cash 17,467.0 0 8,023.00

Investments 4,853.00 3,367.00

Inventories 1,056.00 2,138.00

Accounts receivable 2,165.00 3,600.00

Prepaid expenses 3,000.00 3,000.00

Other 860.00 976.00

Total current assets 29,401.00 21,104.00

Fixed assets: 2013 2014

Property and equipment 64,553.00 58,219.00

Building/site improvements 4,780.00 2,679.00

Equity and other investments 3,789.00 4,587.00

Less accumulated depreciation 5,625.00 4,171.00

Total fixed assets 67,497.00 61,314.00

Other assets: 2013 2014

Goodwill 1,577.00 1,650.00

Total other assets 1,577.00 1,650.00

Total assets 98,475.00 84,068.00

US_124-127_Depreciation.indd 127 21/11/2014 16:23

How it works

Amortization is how the cost of purchasing an

intangible asset, such as copyright of an artwork, is

spread over a period of time, usually its useful lifetime.

It is shown as a reduction in the value of the intangible

asset on the balance sheet and an expense on the

income statement. In lending, amortization can also

mean the paying off of debts over time. Depletion

shows the exhaustion of natural resources such as

coal mines, forests, or natural gas.

Amortization

and depletion

Amortization in practice

There are two types of amortization, one for spreading the cost of an

intangible asset, the other for loan repayment. Both are calculated in

similar ways, but loan repayments are worked out as a percentage.

Similar concepts to depreciation, amortization and depletion are used

by accountants to show how intangible assets and natural resources

respectively are used up.

$2,000

YEARLY

AMORTIZATION

%

2%

=

=

=

=

=

$20,000

10 YEARS

INITIAL COST

USEFUL LIFE

COST OF LOAN

YEARLY REPAYMENT

150,000

3,000

YEARS TO REPAY

100

50

100

Loan percentage

If a company has an outstanding loan worth

$150,000, and pays off $3,000 of this loan

each year, then $3,000 of the loan has been

amortized. It can also be said that 2 percent

of the loan has been amortized, as it will

take 50 years to repay the loan at this rate.

Time (years)

Intangible assets

In this example, a

company buys an

intangible asset—

a patent for a new,

revolutionary type

of tennis racket—for

$20,000. The patent

will be useful for 10

years, so its cost is

recorded as a $2,000

amortization (expense)

each year rather than as

a one-time cost. Unlike

tangible assets, a patent

does not have a salvage

value (see p.124).

Value ($)

1

2 3 4 5 6 7 8 9 10

$20,000

$16,000

$12,000

$8,000

$4,000

0

=

US_128-129_Amortization-depletion.indd 128 21/11/2014 16:23

128 129

HOW FINANCE WORKS

Financial accounting

GOODWILL

In business, goodwill describes an

intangible asset based on a company’s

reputation, including loyal customers

and suppliers, brand name, and public

profile. Goodwill arises when one

company buys another for more than

the fair market value of its net assets

(total assets minus total liabilities).

For example, if Company A buys

Company B for $10 million but the

total sum of its assets and liabilities is

$9 million, the goodwill is worth $1

million. According to International

Financial Reporting Standards since

2001, goodwill does not amortize,

so it does not appear as amortization

in financial statements. However, if

the value of goodwill falls (through

negative publicity, for example) it

can be recorded as an impairment.

How to calculate depletion

Like amortization, depletion is calculated using the straight-line

method (see pp.124–125) unless there is a particular reason to use

another method.

Intangible assets Non-

physical assets, such as patents,

trademarks, brand recognition,

and copyright; their valuation is

sometimes subjective

Patent A license granted by a

government or authority giving

the owner exclusive rights for

making or owning an invention

NEED TO KNOW

$900,000

DEPLETION

EXPENSE

UNITS

EXTRACTED

=

=

X

COST – SALVAGE VALUE

TOTAL UNITS

10,000,000 - 1,000,000

60,000

6,000

TIME (YEARS)

NUMBER

OF TREES

10987654321

In this example, a logging company buys

a forest with an estimated 60,000 trees for

$10million. The original salvage value is

$1.5million, but the company spends $500,000

on road building in the forest, bringing it down

to $1million. The company cuts down 6,000

trees during each accounting period.

X

60,000

50,000

40,000

30,000

20,000

10,000

0

$10

MILLION

$1

MILLION

$9.1

MILLION

$8.2

MILLION

$7.3

MILLION

$6.4

MILLION

$5.5

MILLION

$4.6

MILLION

$3.7

MILLION

$2.8

MILLION

$1.9

MILLION

US_128-129_Amortization-depletion.indd 129 09/11/2016 11:01

128 129

HOW FINANCE WORKS

Financial accounting

GOODWILL

In business, goodwill describes an

intangible asset based on a company’s

reputation, including loyal customers

and suppliers, brand name, and public

profile. Goodwill arises when one

company buys another for more than

the fair market value of its net assets

(total assets minus total liabilities).

For example, if Company A buys

Company B for $10 million but the

total sum of its assets and liabilities is

$9 million, the goodwill is worth $1

million. According to International

Financial Reporting Standards since

2001, goodwill does not amortize,

so it does not appear as amortization

in financial statements. However, if

the value of goodwill falls (through

negative publicity, for example) it

can be recorded as an impairment.

How to calculate depletion

Like amortization, depletion is calculated using the straight-line

method (see pp.124–125) unless there is a particular reason to use

another method.

Intangible assets Non-

physical assets, such as patents,

trademarks, brand recognition,

and copyright; their valuation is

sometimes subjective

Patent A license granted by a

government or authority giving

the owner exclusive rights for

making or owning an invention

NEED TO KNOW

$900,000

DEPLETION

EXPENSE

UNITS

EXTRACTED

=

=

X

COST – SALVAGE VALUE

TOTAL UNITS

10,000,000 - 1,000,000

60,000

6,000

TIME (YEARS)

NUMBER

OF TREES

10987654321

In this example, a logging company buys

a forest with an estimated 60,000 trees for

$10million. The original salvage value is

$1.5million, but the company spends $500,000

on road building in the forest, bringing it down

to $1million. The company cuts down 6,000

trees during each accounting period.

X

60,000

50,000

40,000

30,000

20,000

10,000

0

$10

MILLION

$1

MILLION

$9.1

MILLION

$8.2

MILLION

$7.3

MILLION

$6.4

MILLION

$5.5

MILLION

$4.6

MILLION

$3.7

MILLION

$2.8

MILLION

$1.9

MILLION

US_128-129_Amortization-depletion.indd 129 09/11/2016 11:01

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.