Costs

Fixed and

variable costs

One way of looking at costs is to split them

into two categories: fixed costs, which do not

change with the level of business activity, and

variable costs, which do change with the level

of business activity. This helps accountants

to determine how changes in business

activity (for example, cutting or increasing

production) will affect costs. In reality, some

fixed costs will increase once business activity

reaches a certain level—these are called

stepped fixed costs.

How it works

There are two main ways of classifying costs:

variable costs, which increase as output increases,

and fixed costs, which remain constant; direct and

indirect costs, which contribute directly or indirectly

to the overall running of the business, and can either

vary with the level of production or stay fixed. There

are three main costs that businesses need to account

for. The first is labor—wages paid to people employed

to carry out a particular task. Labor can be regarded

as a direct cost or overhead, or as variable or fixed. The

second is the raw materials used in production and

other materials used in service industries—these costs

are variable. The third is expenses, which are other

costs incurred in the course of the business’s activities.

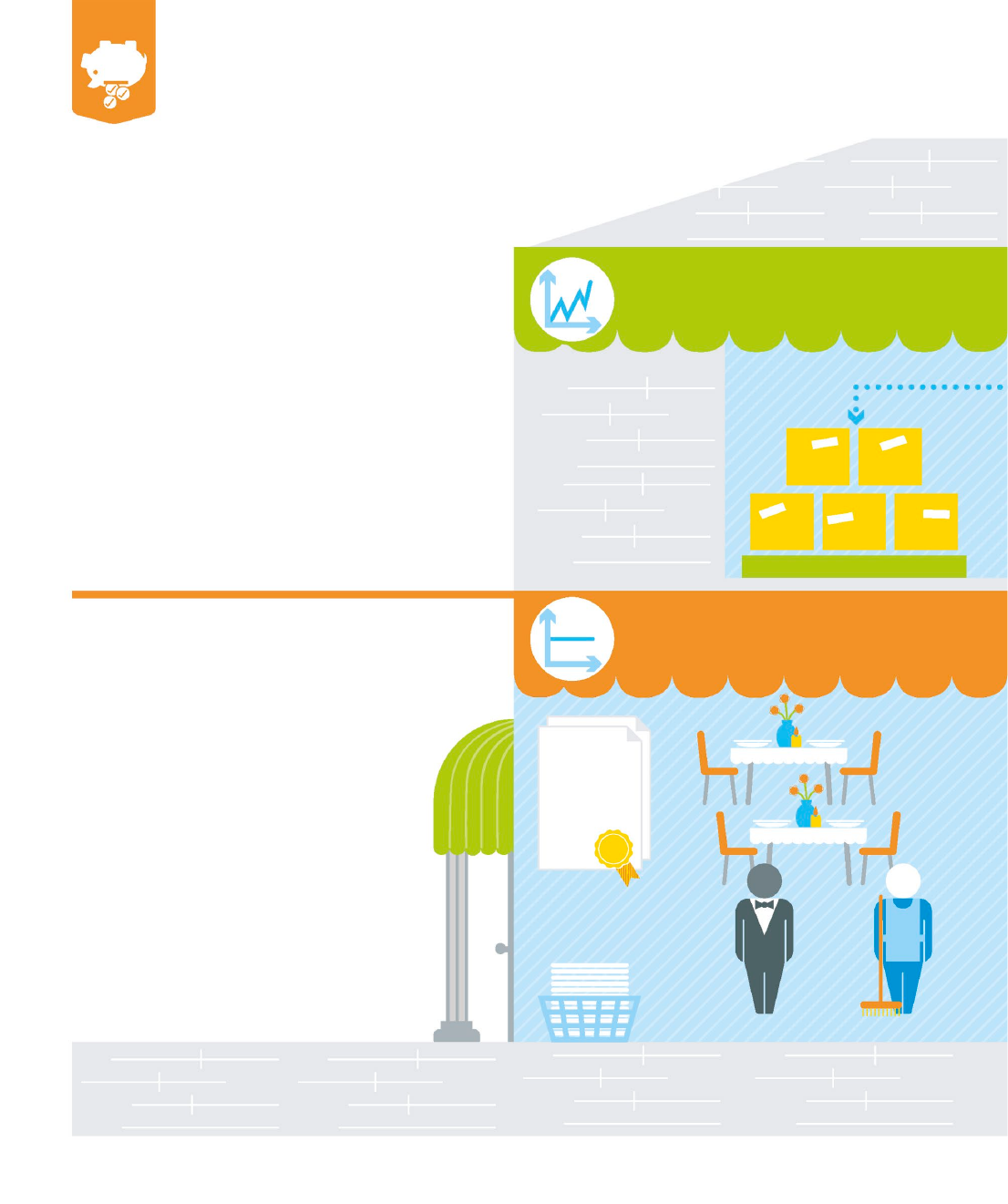

Costs are the direct or indirect expenses that a business incurs

in order to carry out activities that earn revenue, such as

manufacturing goods or providing a service.

Fixed costs

Variable costs

A restaurant rents premises to cater for 40 diners. The

fixed costs are the same whether the restaurant serves

30 or 40 diners a night.

The head chef orders

the ingredients that will

be required each day.

For peak evenings the

cost of the food order

is higher; for quieter

nights, the food order

is lower.

CLEANING BILL

STAFF SALARIES

LAUNDRY

SERVICES

RENT AND

INSURANCE

COSTS

LARGE

FOOD ORDER

US_140-141_Costs.indd 140 09/11/2016 11:01

140 141

HOW FINANCE WORKS

Management accounting

Break-even point (BEP) The

point at which total sales revenue

is equal to total costs

Questionable costs Costs that

can be treated as fixed or variable

Sunk costs Costs incurred in the

past that cannot be recovered

Prospective costs Costs that

may be incurred in the future

depending on which business

decisions are made

need to know

Stepped fixed costs

The restaurant becomes popular, so the owner rents the

premises next door to serve an additional 40 diners a night.

The costs that were fixed at a certain level have now doubled.

EXTRA

LAUNDRY

SERVICES

HIGHER STAFF COSTS HIGHER CLEANING BILL

HIGHER

RENT AND

INSURANCE

COSTS

PEAK

EVENINGS

QUIETER

EVENINGS

SMALL

FOOD ORDER

40%

of business

owners say that

payroll is their

greatest expense

US_140-141_Costs.indd 141 21/11/2014 16:23

140 141

HOW FINANCE WORKS

Management accounting

Break-even point (BEP) The

point at which total sales revenue

is equal to total costs

Questionable costs Costs that

can be treated as fixed or variable

Sunk costs Costs incurred in the

past that cannot be recovered

Prospective costs Costs that

may be incurred in the future

depending on which business

decisions are made

need to know

Stepped fixed costs

The restaurant becomes popular, so the owner rents the

premises next door to serve an additional 40 diners a night.

The costs that were fixed at a certain level have now doubled.

EXTRA

LAUNDRY

SERVICES

HIGHER STAFF COSTS HIGHER CLEANING BILL

HIGHER

RENT AND

INSURANCE

COSTS

PEAK

EVENINGS

QUIETER

EVENINGS

SMALL

FOOD ORDER

40%

of business

owners say that

payroll is their

greatest expense

US_140-141_Costs.indd 141 21/11/2014 16:23

How it works

Both direct and indirect costs

contribute to the production cost

of a product, whether it is a

manufactured good or a service

being provided. In order to

calculate the cost of a product, it

is treated as one unit of production.

The direct and indirect costs

involved in creating that single

unit are then assessed and added

together to create the full cost.

Product costing

and pricing

Full cost pricing

Direct costs can be measured in terms

of how materials and labor are used

to produce each unit. Indirect costs

(overheads) are harder to assess but also

need to be factored in so that the full cost of

each product can be calculated. Managers

and accountants must apportion indirect

costs to reflect their contribution to the cost

of creating a single product. Once this is

ascertained, the full cost of that product can

be determined. In general terms, the price is

worked out by adding the direct and indirect

costs of production with a

profit margin that gives an

appropriate selling price.

Knowing the full cost of creating each product that a business

sells is vital because it helps a company price its products

appropriately and assess the performance of the business.

Materials

Direct labor

Direct expenses

All used exclusively to

create a product or

service for sale

Direct costs

Production and service

overheads

Administrative

and management

overheads

Sales and distribution

overheads

Share of indirect costs

Absorption costing Allocation

of all production costs to product

Differential costing Difference

between the cost of two options

Incremental (marginal) costing

The change in total costs incurred

when one additional unit is made

Throughput costing Treating all

costs except for direct materials

as period expenses

Cost-plus pricing Product price

is based on direct and indirect

costs, plus markup percentage

NEED TO KNOW

38%

the average total of US

business costs that can be

accounted for by indirect costs

US_142-143_Product_costing.indd 142 09/11/2016 11:01

142 143

how finance works

Management accounting

Share of indirect costs

Profit margin

Selling price

Low: in order to gain market

share, or to match competitors

Cost-based: recover

direct and indirect

costs and profit

margin that the

market will accept

Service-based:

flexible since no

manufacturing or

distribution cost

Must be able to generate profit

for the company

Must be in line with how the

product has been

marketed

Must be

pitched

realistically so

that customers

will buy

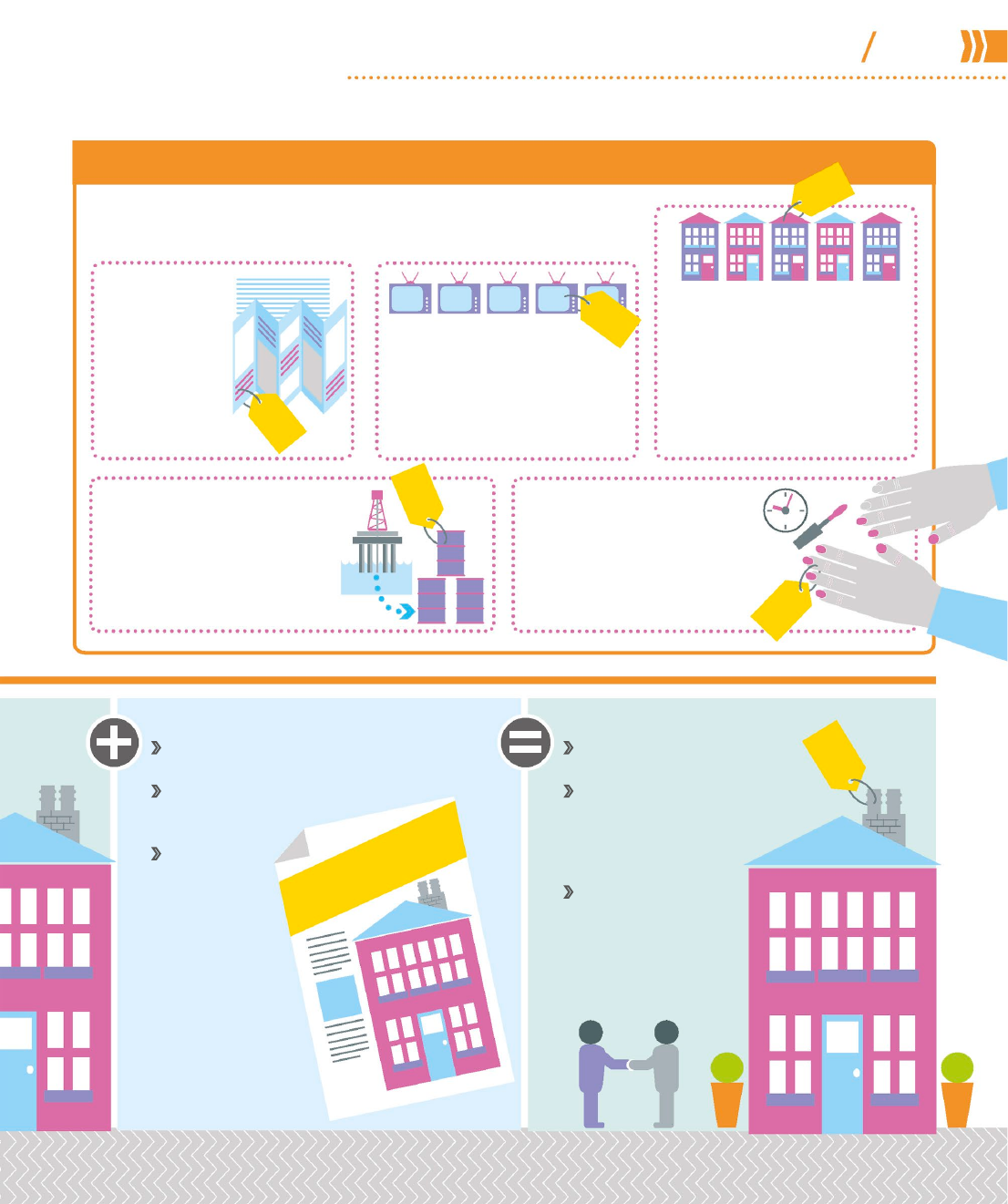

Process costing

Used for an ongoing job that often

involves several manufacturing

processes, making it difficult to isolate

individual unit costs—for example,

an oil refinery which processes

crude oil into diesel oil

service costing

Used when the product being sold

is a standard service offered to

customers—for example, a nail salon

offering an express manicure and

pedicure within a set period of time

and for a fixed price

Job costing

Used for a

customized order

made to a client’s

specifications—for

example, a printing

company that

prints brochures

for a client

batch costing

Used when a batch of identical

products is made—for example,

an electrical goods company

manufacturing television sets

contract costing

Used for a large one-time job, often

the result of a tender process (when

a company bids for work) and

carried out at the client’s site—for

example, a construction company

building homes in a new residential

development

$

$

$

$

$

LUXURY HOME

FOR SALE

OTHER COSTING METHODS

There are several different approaches to costing and pricing depending on the

industry, the type and size of the business, and the method of production.

$

US_142-143_Product_costing.indd 143 21/11/2014 16:38

142 143

how finance works

Management accounting

Share of indirect costs

Profit margin

Selling price

Low: in order to gain market

share, or to match competitors

Cost-based: recover

direct and indirect

costs and profit

margin that the

market will accept

Service-based:

flexible since no

manufacturing or

distribution cost

Must be able to generate profit

for the company

Must be in line with how the

product has been

marketed

Must be

pitched

realistically so

that customers

will buy

Process costing

Used for an ongoing job that often

involves several manufacturing

processes, making it difficult to isolate

individual unit costs—for example,

an oil refinery which processes

crude oil into diesel oil

service costing

Used when the product being sold

is a standard service offered to

customers—for example, a nail salon

offering an express manicure and

pedicure within a set period of time

and for a fixed price

Job costing

Used for a

customized order

made to a client’s

specifications—for

example, a printing

company that

prints brochures

for a client

batch costing

Used when a batch of identical

products is made—for example,

an electrical goods company

manufacturing television sets

contract costing

Used for a large one-time job, often

the result of a tender process (when

a company bids for work) and

carried out at the client’s site—for

example, a construction company

building homes in a new residential

development

$

$

$

$

$

LUXURY HOME

FOR SALE

OTHER COSTING METHODS

There are several different approaches to costing and pricing depending on the

industry, the type and size of the business, and the method of production.

$

US_142-143_Product_costing.indd 143 21/11/2014 16:38

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.