Case study: cash-flow statement

By analyzing this water utility’s statement, which includes a comparison to the previous year, decision-

makers can base future plans on past cash flows (at the time, the exchange rate was £1 = $1.58).

Cash-flow statement

The cash-flow statement shows the movement of cash during the last

accounting period. It is important because it reveals a company’s

liquidity—whether or not it has more money coming in than going out.

How to read a cash-flow statement

The statement of cash flows, to give it its official title, answers the key question of whether a

business is making enough money to sustain itself and provide surplus capital to grow in the

future, pay any debts, and give out dividends. Figures in parentheses are negative numbers.

Net cash inflow from operating activities 334.6 303.2

Returns on investments and servicing of finance (80.0) (79.2)

Taxation (21.8) (31.5)

Capital expenditure and financial investment (215.4) (149.7)

Dividends paid (129.6) (129.4)

(Decrease)/increase in cash—above (33.2) 135.6

Movement in loans and leases (79.0) (222.2)

Movement in net debt (112.2) (86.6)

Opening net debt (1,626.1) (1,539.5)

Closing net debt (1,738.3) (1,626.1)

Cash outflow before financial investment (112.2) (86.6)

Financing 79.0 222.2

Reconciliation of cash movement to the movement in net debt

(Decrease)/increase in cash (33.2) 135.6

Using profit before tax as a starting

point, non-cash income and expenses

are deducted to reach net cash inflow

from operating activities

Returns on investment in this case

is total interest received minus total

interest paid, as well as interest paid

on finance lease rentals

Taxation is the sum of all taxes paid

and tax credits received

Capital expenditure and financial

investment is, here, the sum of the

sale of tangible assets plus connection

charges, grants, and deferred income

Dividends are sums of money paid

to shareholders, typically each year

This is the sum of all the figures above

Financing describes how much money

the company has made or lost from

loans, finance leases, and bonds

This is the change from last year’s

figures to this year’s, and the total

of the two figures above

A utility company can afford

to operate with more debt than

companies with a less stable base

Year to

March 31,

2013

£m

Year to

March 31,

2012

£m

$

US_120-121_Cashflow_statement_Steve.indd 120 21/11/2014 14:24

120 121

HOW FINANCE WORKS

Financial accounting

How it works

The cash-flow statement is often more useful for

investors assessing a business’s health than other key

statements, because it shows how the core activities

are performing. The profit-and-loss statement, for

example, obscures this by adding in non-cash factors

such as depreciation. Similarly, the balance sheet is

more concerned with assets than liquidity.

Three types of cash flow

Cash refers to actual money as well as cash equivalents including cash in the bank; bank lines

of credit; and short-term, highly liquid investments for which there is little risk of a change in

value. Cash does not include interest, depreciation, or bad debts (debts written off).

Cash flow from operating activities

The bulk of cash flow usually comes from operations, and is worked out with a

formula. The change in working capital (current assets minus current liabilities)

can be a negative figure.

In this example, a juice company sells $100 worth of orange

juice after spending $20 on oranges. It pays 25 percent of its

$80 earnings in tax. Its juicing machine incurs a depreciation

expense of $20 over the period (a positive adjustment on the

orginal outlay for the machine). There is no change in working

capital (short-term assets to cover short-term debt).

$100

$20

$20

$0

$80

=++-

-

A JUICE

COMPANY SELLS

WORTH OF

ORANGE JUICE

AND SPENDS

ON ORANGES

OVER THE

PERIOD

ITS JUICING

MACHINE INCURS

A DEPRECIATION

EXPENSE OF

IT PAYS

25%

OF ITS EARNINGS

IN TAX

DEPRECIATION

REVENUE –

COST OF SALES

TAXES

– + + =

ANY CHANGE

IN WORKING

CAPITAL

NO CHANGE

IN WORKING

CAPITAL

CASH FLOW

FROM OPERATING

ACTIVITIES

CASH FLOW

FROM

OPERATING

ACTIVITIES

Total cash flow

Adding all three cash flows

gives the total. Separating

out the three types shows decision-

makers the health of core activities

as opposed to financing and

investing, which bear little relation

to day-to-day operations.

Cash flow from

investing activities

Buying or selling assets

or investments is in this category.

This figure is usually a cash outflow

(negative figure) due to buying more

than selling, but can be positive if

there are significant sales.

Cash flow from

financing activities

This includes buying or

selling stock and paying out debt

or dividends. Money made from

selling something is called cash

inflow; money lost through paying

out is cash outflow.

Cash flow from operating activities in practice

=

US_120-121_Cashflow_statement_Steve.indd 121 09/11/2016 11:01

120 121

HOW FINANCE WORKS

Financial accounting

How it works

The cash-flow statement is often more useful for

investors assessing a business’s health than other key

statements, because it shows how the core activities

are performing. The profit-and-loss statement, for

example, obscures this by adding in non-cash factors

such as depreciation. Similarly, the balance sheet is

more concerned with assets than liquidity.

Three types of cash flow

Cash refers to actual money as well as cash equivalents including cash in the bank; bank lines

of credit; and short-term, highly liquid investments for which there is little risk of a change in

value. Cash does not include interest, depreciation, or bad debts (debts written off).

Cash flow from operating activities

The bulk of cash flow usually comes from operations, and is worked out with a

formula. The change in working capital (current assets minus current liabilities)

can be a negative figure.

In this example, a juice company sells $100 worth of orange

juice after spending $20 on oranges. It pays 25 percent of its

$80 earnings in tax. Its juicing machine incurs a depreciation

expense of $20 over the period (a positive adjustment on the

orginal outlay for the machine). There is no change in working

capital (short-term assets to cover short-term debt).

$100

$20

$20

$0

$80

=++-

-

A JUICE

COMPANY SELLS

WORTH OF

ORANGE JUICE

AND SPENDS

ON ORANGES

OVER THE

PERIOD

ITS JUICING

MACHINE INCURS

A DEPRECIATION

EXPENSE OF

IT PAYS

25%

OF ITS EARNINGS

IN TAX

DEPRECIATION

REVENUE –

COST OF SALES

TAXES

– + + =

ANY CHANGE

IN WORKING

CAPITAL

NO CHANGE

IN WORKING

CAPITAL

CASH FLOW

FROM OPERATING

ACTIVITIES

CASH FLOW

FROM

OPERATING

ACTIVITIES

Total cash flow

Adding all three cash flows

gives the total. Separating

out the three types shows decision-

makers the health of core activities

as opposed to financing and

investing, which bear little relation

to day-to-day operations.

Cash flow from

investing activities

Buying or selling assets

or investments is in this category.

This figure is usually a cash outflow

(negative figure) due to buying more

than selling, but can be positive if

there are significant sales.

Cash flow from

financing activities

This includes buying or

selling stock and paying out debt

or dividends. Money made from

selling something is called cash

inflow; money lost through paying

out is cash outflow.

Cash flow from operating activities in practice

=

US_120-121_Cashflow_statement_Steve.indd 121 09/11/2016 11:01

How it works

Globally, there are reams of different environment

acts spread across multiple jurisdictions that affect

the companies operating within their borders in

different ways. Areas protected by environment acts

include the atmosphere, fresh water, the marine

environment, nature conservation, nuclear safety, and

noise pollution. International acts are usually ratified

by each country individually before taking effect

there. An example of a common global means of

reducing greenhouse gas emissions is emissions

trading (“cap and trade”), by which companies must

buy a permit for each ton of CO

2

they emit over a

certain level. Those emitting under the agreed level

can sell their permits to other companies.

Environmental

accounting

Environmental regulations force companies to consider the impact of

their activities and to adopt corporate social responsibility (CSR) as

they grapple with legislation, climate change, and public opinion.

Environmental credentials

Most companies include a section on environmental

accounting in their financial statement. Some details are

required by law, but the statement also gives an opportunity

to showcase environmental credentials to stakeholders.

Product

responsibility

Life-cycle stages in which the

health-and-safety impact

of products and services are

assessed for improvement

Adherence to laws,

standards, and voluntary

codes relating to marketing

communications

Society

Programs and practices

that assess and manage

the impact of operations

on communities

Fines and sanctions for

noncompliance with

regulations

Cleaning up rivers

Wessex Water’s impressive record on pollution is

mentioned several times in its statement, including in

the chairman’s introduction. This prominence shows

that the company believes acting in an environmentally

conscious manner is important to its investors. The

company illustrates several areas where it has acted

with others to positively affect the environment:

Work with the charity Surfers Against Sewage,

which campaigns for clean seawater

Its river strategy: collaborating with pressure groups

and organizations to reduce pollutants and the impact

of habitat alteration, and so increase the numbers

of aquatic plants, invertebrates, and fish in local rivers

Improving water quality at swimming beaches in the

region, in compliance with mandatory standards

Case study

US_122-123_Environment_acts_and_crs.indd 122 21/11/2014 14:25

122 123

How finance works

Financial accounting

Environmental

Direct and indirect energy

consumption

Waste by type and disposal method

Water withdrawal by source;

discharge by destination and quality

Fines and sanctions for

noncompliance with regulations

Human rights

Investment agreements

that include human rights

clauses or that have undergone

human rights screening

Suppliers and contractors

that have undergone screening

on human rights; actions taken

to address any issues

Economic

Financial implications, risks,

and opportunities for the

organization’s activities

due to climate change

Financial assistance received

from the government

Greenhouse Gas emissions

Appointed

business

Direct fuel

use

Grid

electricity

Third

parties

Total

2012–13

Total

2011–12

Gas, diesel,

other fuels

6 0 4 10 8

Grid electricity 0 115 0 115 107

Transportation 9 0 1 11 11

Methane 17 0 2 20 20

Nitrous oxide 10 0 7 17 19

Exported

renewable

0 (3) 0 (3) (4)

TOTAL (net

emissions)

42 112 14 169 161

In some countries, companies are

required by law to provide details

of their greenhouse gas emissions.

This is usually presented as a table

in the environmental accounting

section of the annual report. It

includes direct and indirect

emissions—by the company itself and

by third parties—of gas, diesel, and

other fuels; sulfur oxides and nitrous

oxides; methane; and other ozone-

depleting substances. In this table,

from the Wessex Water utility

company, emissions are shown

as ktCO

2

equivalents.

Labor practices

Workforce by employment

type, contract, and region

Average hours of training

per year, per employee by

employee category

Ratio of basic salary

of men to women by

employment category

$

US_122-123_Environment_acts_and_crs.indd 123 21/11/2014 14:25

122 123

How finance works

Financial accounting

Environmental

Direct and indirect energy

consumption

Waste by type and disposal method

Water withdrawal by source;

discharge by destination and quality

Fines and sanctions for

noncompliance with regulations

Human rights

Investment agreements

that include human rights

clauses or that have undergone

human rights screening

Suppliers and contractors

that have undergone screening

on human rights; actions taken

to address any issues

Economic

Financial implications, risks,

and opportunities for the

organization’s activities

due to climate change

Financial assistance received

from the government

Greenhouse Gas emissions

Appointed

business

Direct fuel

use

Grid

electricity

Third

parties

Total

2012–13

Total

2011–12

Gas, diesel,

other fuels

6 0 4 10 8

Grid electricity 0 115 0 115 107

Transportation 9 0 1 11 11

Methane 17 0 2 20 20

Nitrous oxide 10 0 7 17 19

Exported

renewable

0 (3) 0 (3) (4)

TOTAL (net

emissions)

42 112 14 169 161

In some countries, companies are

required by law to provide details

of their greenhouse gas emissions.

This is usually presented as a table

in the environmental accounting

section of the annual report. It

includes direct and indirect

emissions—by the company itself and

by third parties—of gas, diesel, and

other fuels; sulfur oxides and nitrous

oxides; methane; and other ozone-

depleting substances. In this table,

from the Wessex Water utility

company, emissions are shown

as ktCO

2

equivalents.

Labor practices

Workforce by employment

type, contract, and region

Average hours of training

per year, per employee by

employee category

Ratio of basic salary

of men to women by

employment category

$

US_122-123_Environment_acts_and_crs.indd 123 21/11/2014 14:25

How it works

If a business buys a long-lived

asset, such as a building, factory

equipment, or computer, to help it

earn income, this expenditure can

be offset as a cost against income

earned. However, not all this

income will be generated in the

year of purchase and, over time,

the asset will age and become less

beneficial to the business, until

it becomes outdated or unusable.

Accountants do two things to

turn the declining value into a

tax advantage. Firstly, they work

out how much the asset’s value

decreases over a period of time—

typically a year. Secondly, they

match that loss in value to the

amount of income earned in that

period, so depreciation becomes

a deduction from taxable income.

There are several different

ways to calculate depreciation.

The method a company uses may

depend on the kind of business, the

type of asset, tax rules, or personal

preference. In the United States,

per IRS guidelines, companies

must use MACRS (Modified

Accelerated Cost Recovery System),

a combination of straight-line and

double declining balance methods

(see below and p.126).

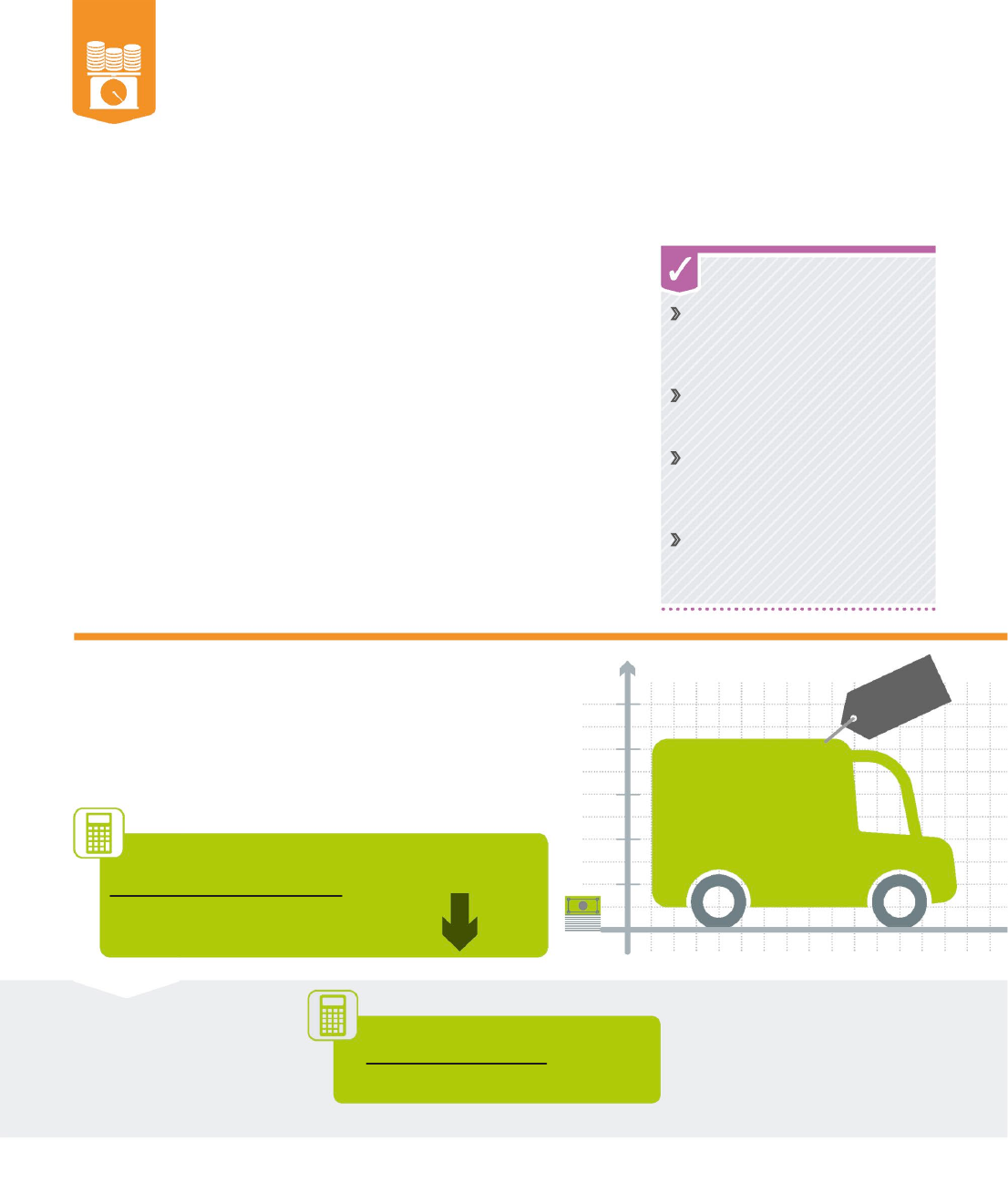

Depreciation

When a company buys an asset, its cost can be deducted from income

for accounting and tax purposes. Depreciation allows the company to

spread the cost, by calculating the asset’s decline in value over time.

USEFUL ECONOMIC

LIFE (YEARS)

ANNUAL

DEPRECIATION ($)

=

Example

A landscaping business buys a

new van for $25,000. The IRS

sets its scrap value at $5,000

after five years of use.

Year 1 After a year, the van’s

value has depreciated by $4,000

(its purchase value minus its scrap

value, divided by its useful economic

life). Its value is now $21,000.

$25,000 – $5,000

5

$4,000

=

Fixed/tangible assets Items that

enable a business to operate but are

not a part of trade; assets lasting a

year or more qualify for depreciation

Useful/economic life Length of

time an asset is fit for its purpose

and has monetary value

Salvage/scrap/residual value

Worth of an asset once it has

outlived its useful life—often set

by the tax authority

Book value An asset’s worth on

paper at any point between its

initial purchase and salvage

NEED TO KNOW

The straight-line method is the simplest way of working out

depreciation and can be applied to most assets. Depreciation is

calculated along a timeline, with value loss spread evenly over

the asset’s economic life. Scrap value is deducted from purchase

value and the remainder is split into equal portions over time.

Calculating depreciation

$21,000

VALUE ($)

$25,000

$20,000

$15,000

$10,000

$5,000

1

0

PURCHASE

VALUE

SCRAP

VALUE

–

$

$

US_124-127_Depreciation.indd 124 21/11/2014 16:23

124 125

how finance works

Financial accounting

Year 2 After the second year, the

value has depreciated by another

$4,000. The van will lose an equal

amount of value each year for the next

three years of its useful economic life.

Year 3 At the end of the third

year, the van has depreciated

by another $4,000, and its book

value is $13,000, although its

actual value may be more or less.

Year 4 The van

has depreciated by

$4,000, to $9,000,

at the end of four

years of life.

Year 5 By the

end of year five,

the van is valued

at only $5,000—

its scrap value.

RACEHORSES

2 years

COMPUTERS

3 years

OFFICE

FURNITURE

6 years

ROADS

15 years

BOATS

20 years

FRUIT-

BEARING TREES

10 years

Time

(years)

5 15

10 20

$17,000

$13,000

$9,000

$5,000

TIME (YEARS)

2 3 4

5

Typical life of fixed asseTs

Tax authorities often specify the typical useful (economic) life of a particular asset.

This helps to standardize depreciation, and to eliminate uncertainty about value

and the number of years over which an asset can be depreciated.

60%

the value the

average car

loses after

three years

US_124-127_Depreciation.indd 125 21/11/2014 16:23

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.