To better understand cointegration, we focus on VAR models for their simplicity in estimation. Consider a k-dimensional VAR(p) time series ![]() with possible time trend so that the model is

with possible time trend so that the model is

8.35 ![]()

where the innovation ![]() is assumed to be Gaussian and

is assumed to be Gaussian and ![]() =

= ![]() , where

, where ![]() and

and ![]() are k-dimensional constant vectors. Write

are k-dimensional constant vectors. Write ![]() =

= ![]() . Recall that if all zeros of the determinant

. Recall that if all zeros of the determinant ![]() are outside the unit circle, then

are outside the unit circle, then ![]() is unit-root stationary. In the literature, a unit-root stationary series is said to be an I(0) process; that is, it is not integrated. If

is unit-root stationary. In the literature, a unit-root stationary series is said to be an I(0) process; that is, it is not integrated. If ![]() = 0, then

= 0, then ![]() is unit-root nonstationary. For simplicity, we assume that

is unit-root nonstationary. For simplicity, we assume that ![]() is at most an integrated process of order 1; that is, an I(1) process. This means that (1 − B)xit is unit-root stationary if xit itself is not.

is at most an integrated process of order 1; that is, an I(1) process. This means that (1 − B)xit is unit-root stationary if xit itself is not.

An error correction model (ECM) for the VAR(p) process ![]() is

is

where ![]() are defined in Eq. (8.34) and

are defined in Eq. (8.34) and ![]() =

= ![]() . We refer to the term

. We refer to the term ![]() of Eq. (8.36) as the error correction term, which plays a key role in cointegration study. Notice that

of Eq. (8.36) as the error correction term, which plays a key role in cointegration study. Notice that ![]() can be recovered from the ECM representation via

can be recovered from the ECM representation via

![]()

where ![]() , the zero matrix. Based on the assumption that

, the zero matrix. Based on the assumption that ![]() is at most I(1),

is at most I(1), ![]() of Eq. (8.36) is an I(0) process.

of Eq. (8.36) is an I(0) process.

If ![]() contains unit roots, then

contains unit roots, then ![]() = 0 so that

= 0 so that ![]() is singular. Therefore, three cases are of interest in considering the ECM in Eq. (8.36):

is singular. Therefore, three cases are of interest in considering the ECM in Eq. (8.36):

1. Rank(![]() ) = 0. This implies

) = 0. This implies ![]() and

and ![]() is not cointegrated. The ECM of Eq. (8.36) reduces to

is not cointegrated. The ECM of Eq. (8.36) reduces to

![]()

so that ![]() follows a VAR(p − 1) model with deterministic trend

follows a VAR(p − 1) model with deterministic trend ![]() .

.

2. Rank(![]() ) = k. This implies that

) = k. This implies that ![]() and

and ![]() contains no unit roots; that is,

contains no unit roots; that is, ![]() is I(0). The ECM model is not informative and one studies

is I(0). The ECM model is not informative and one studies ![]() directly.

directly.

3. ![]() . In this case, one can write

. In this case, one can write ![]() as

as

where ![]() and

and ![]() are k × m matrices with Rank(

are k × m matrices with Rank(![]() ) = Rank(

) = Rank(![]() ) = m. The ECM of Eq. (8.36) becomes

) = m. The ECM of Eq. (8.36) becomes

8.38 ![]()

This means that ![]() is cointegrated with m linearly independent cointegrating vectors,

is cointegrated with m linearly independent cointegrating vectors, ![]() , and has k − m unit roots that give k − m common stochastic trends of

, and has k − m unit roots that give k − m common stochastic trends of ![]() .

.

If ![]() is cointegrated with Rank(

is cointegrated with Rank(![]() ) = m, then a simple way to obtain a presentation of the k − m common trends is to obtain an orthogonal complement matrix

) = m, then a simple way to obtain a presentation of the k − m common trends is to obtain an orthogonal complement matrix ![]() of

of ![]() ; that is,

; that is, ![]() is a k × (k − m) matrix such that

is a k × (k − m) matrix such that ![]() , a (k − m) × m zero matrix, and use

, a (k − m) × m zero matrix, and use ![]() . To see this, one can premultiply the ECM by

. To see this, one can premultiply the ECM by ![]() and use

and use ![]() to see that there would be no error correction term in the resulting equation. Consequently, the (k − m)-dimensional series

to see that there would be no error correction term in the resulting equation. Consequently, the (k − m)-dimensional series ![]() should have k − m unit roots. For illustration, consider the bivariate example of Section 8.5.1. For this special series,

should have k − m unit roots. For illustration, consider the bivariate example of Section 8.5.1. For this special series, ![]() and

and ![]() . Therefore,

. Therefore, ![]() , which is precisely the unit-root nonstationary series y1t in Eq. (8.32).

, which is precisely the unit-root nonstationary series y1t in Eq. (8.32).

Note that the factorization in Eq. (8.37) is not unique because for any m × m orthogonal matrix ![]() satisfying

satisfying ![]() , we have a

, we have a

![]()

where both ![]() and

and ![]() are also of rank m. Additional constraints are needed to uniquely identify

are also of rank m. Additional constraints are needed to uniquely identify ![]() and

and ![]() . It is common to require that

. It is common to require that ![]() , where

, where ![]() is the m × m identity matrix and

is the m × m identity matrix and ![]() is a (k − m) × m matrix. In practice, this may require reordering of the elements of

is a (k − m) × m matrix. In practice, this may require reordering of the elements of ![]() such that the first m components all have a unit root. The elements of

such that the first m components all have a unit root. The elements of ![]() and

and ![]() must also satisfy other constraints for the process

must also satisfy other constraints for the process ![]() to be unit-root stationary. For example, consider the case of a bivariate VAR(1) model with one cointegrating vector. Here k = 2, m = 1, and the ECM is

to be unit-root stationary. For example, consider the case of a bivariate VAR(1) model with one cointegrating vector. Here k = 2, m = 1, and the ECM is

![]()

Premultiplying the prior equation by ![]() , using

, using ![]() , and moving wt−1 to the right-hand side of the equation, we obtain

, and moving wt−1 to the right-hand side of the equation, we obtain

![]()

where ![]() . This implies that wt is a stationary AR(1) process. Consequently, αi and β1 must satisfy the stationarity constraint |1 + α1 + α2β1| < 1.

. This implies that wt is a stationary AR(1) process. Consequently, αi and β1 must satisfy the stationarity constraint |1 + α1 + α2β1| < 1.

The prior discussion shows that the rank of ![]() in the ECM of Eq. (8.36) is the number of cointegrating vectors. Thus, to test for cointegration, one can examine the rank of

in the ECM of Eq. (8.36) is the number of cointegrating vectors. Thus, to test for cointegration, one can examine the rank of ![]() . This is the approach taken by Johansen (1988, 1995) and Reinsel and Ahn (1992).

. This is the approach taken by Johansen (1988, 1995) and Reinsel and Ahn (1992).

8.6.1 Specification of the Deterministic Function

Similar to the univariate case, the limiting distributions of cointegration tests depend on the deterministic function ![]() . In this section, we discuss some specifications of

. In this section, we discuss some specifications of ![]() that have been proposed in the literature. To understand some of the statements made below, keep in mind that

that have been proposed in the literature. To understand some of the statements made below, keep in mind that ![]() provides a presentation for the common stochastic trends of

provides a presentation for the common stochastic trends of ![]() if it is cointegrated.

if it is cointegrated.

1. ![]() : In this case, all the component series of

: In this case, all the component series of ![]() are I(1) without drift and the stationary series

are I(1) without drift and the stationary series ![]() has mean zero.

has mean zero.

2. ![]() , where

, where ![]() is an m-dimensional nonzero constant vector. The ECM becomes

is an m-dimensional nonzero constant vector. The ECM becomes

![]()

so that the components of ![]() are I(1) without drift, but

are I(1) without drift, but ![]() have a nonzero mean

have a nonzero mean ![]() . This is referred to as the case of restricted constant.

. This is referred to as the case of restricted constant.

3. ![]() , which is nonzero. Here the component series of

, which is nonzero. Here the component series of ![]() are I(1) with drift

are I(1) with drift ![]() and

and ![]() may have a nonzero mean.

may have a nonzero mean.

4. ![]() , where

, where ![]() is a nonzero vector. The ECM becomes

is a nonzero vector. The ECM becomes

![]()

so that the components of ![]() are I(1) with drift

are I(1) with drift ![]() and

and ![]() has a linear time trend related to

has a linear time trend related to ![]() . This is the case of restricted trend.

. This is the case of restricted trend.

5. ![]() =

= ![]() , where

, where ![]() are nonzero. Here both the constant and trend are unrestricted. The components of

are nonzero. Here both the constant and trend are unrestricted. The components of ![]() are I(1) and have a quadratic time trend and

are I(1) and have a quadratic time trend and ![]() have a linear trend.

have a linear trend.

Obviously, the last case is not common in empirical work. The first case is not common for economic time series but may represent the log price series of some assets. The third case is also useful in modeling asset prices.

8.6.2 Maximum-Likelihood Estimation

In this section, we briefly outline the maximum-likelihood estimation (MLE) of a cointegrated VAR(p) model. Suppose that the data are ![]() . Without loss of generality, we write

. Without loss of generality, we write ![]() , where

, where ![]() , and it is understood that

, and it is understood that ![]() depends on the specification of the previous section. For a given m, which is the rank of

depends on the specification of the previous section. For a given m, which is the rank of ![]() , the ECM model becomes

, the ECM model becomes

8.39 ![]()

where t = p + 1, … , T. A key step in the estimation is to concentrate the likelihood function with respect to the deterministic term and the stationary effects. This is done by considering the following two multivariate linear regressions:

Let ![]() and

and ![]() be the residuals of Eqs. (8.40) and (8.41), respectively. Define the sample covariance matrices

be the residuals of Eqs. (8.40) and (8.41), respectively. Define the sample covariance matrices

![]()

Next, compute the eigenvalues and eigenvectors of ![]() with respect to

with respect to ![]() . This amounts to solving the eigenvalue problem

. This amounts to solving the eigenvalue problem

![]()

Denote the eigenvalue and eigenvector pairs by ![]() , where

, where ![]() . Here the eigenvectors are normalized so that

. Here the eigenvectors are normalized so that ![]() , where

, where ![]() is the matrix of eigenvectors.

is the matrix of eigenvectors.

The unnormalized MLE of the cointegrating vector ![]() is

is ![]() and from which we can obtain an MLE for

and from which we can obtain an MLE for ![]() that satisfies the identifying constraint and normalization condition. Denote the resulting estimate by

that satisfies the identifying constraint and normalization condition. Denote the resulting estimate by ![]() with the subscript c signifying constraints. The MLE of other parameters can then be obtained by the multivariate linear regression

with the subscript c signifying constraints. The MLE of other parameters can then be obtained by the multivariate linear regression

![]()

The maximized value of the likelihood function based on m cointegrating vectors is

![]()

This value is used in the maximum-likelihood ratio test for testing Rank(![]() ) = m. Finally, estimates of the orthogonal complements of

) = m. Finally, estimates of the orthogonal complements of ![]() and

and ![]() can be obtained using

can be obtained using

![]()

8.6.3 Cointegration Test

For a specified deterministic term ![]() , we now discuss the maximum-likelihood test for testing the rank of the

, we now discuss the maximum-likelihood test for testing the rank of the ![]() matrix in Eq. (8.36). Let H(m) be the null hypothesis that the rank of

matrix in Eq. (8.36). Let H(m) be the null hypothesis that the rank of ![]() is m. For example, under H(0), Rank(

is m. For example, under H(0), Rank(![]() ) = 0 so that

) = 0 so that ![]() and there is no cointegration. The hypotheses of interest are

and there is no cointegration. The hypotheses of interest are

![]()

For testing purpose, the ECM in Eq. (8.36) becomes

![]()

where t = p + 1, … , T. Our goal is to test the rank of ![]() . Mathematically, the rank of

. Mathematically, the rank of ![]() is the number of nonzero eigenvalues of

is the number of nonzero eigenvalues of ![]() , which can be obtained if a consistent estimate of

, which can be obtained if a consistent estimate of ![]() is available. Based on the prior equation, which is in the form of a multivariate linear regression, we see that

is available. Based on the prior equation, which is in the form of a multivariate linear regression, we see that ![]() is related to the covariance matrix between

is related to the covariance matrix between ![]() and

and ![]() after adjusting for the effects of

after adjusting for the effects of ![]() and

and ![]() for i = 1, … , p − 1. The necessary adjustments can be achieved by the techniques of multivariate linear regression shown in the previous section. Indeed, the adjusted series of

for i = 1, … , p − 1. The necessary adjustments can be achieved by the techniques of multivariate linear regression shown in the previous section. Indeed, the adjusted series of ![]() and

and ![]() are

are ![]() and

and ![]() , respectively. The equation of interest for the cointegration test then becomes

, respectively. The equation of interest for the cointegration test then becomes

![]()

Under the normality assumption, the likelihood ratio test for testing the rank of ![]() in the prior equation can be done by using the canonical correlation analysis between

in the prior equation can be done by using the canonical correlation analysis between ![]() and

and ![]() . See Johnson and Wichern (1998) for information on canonical correlation analysis. The associated canonical correlations are the partial canonical correlations between

. See Johnson and Wichern (1998) for information on canonical correlation analysis. The associated canonical correlations are the partial canonical correlations between ![]() and

and ![]() because the effects of

because the effects of ![]() and

and ![]() have been adjusted. The quantities

have been adjusted. The quantities ![]() are the squared canonical correlations between

are the squared canonical correlations between ![]() and

and ![]() .

.

Consider the hypotheses

![]()

Johansen (1988) proposes the likelihood ratio (LR) statistic

8.42 ![]()

to perform the test. If Rank(![]() ) = m, then

) = m, then ![]() should be small for i > m and hence LRtr(m) should be small. This test is referred to as the trace cointegration test. Due the presence of unit roots, the asymptotic distribution of LRtr(m) is not chi squared but a function of standard Brownian motions. Thus, critical values of LRtr(m) must be obtained via simulation.

should be small for i > m and hence LRtr(m) should be small. This test is referred to as the trace cointegration test. Due the presence of unit roots, the asymptotic distribution of LRtr(m) is not chi squared but a function of standard Brownian motions. Thus, critical values of LRtr(m) must be obtained via simulation.

Johansen (1988) also considers a sequential procedure to determine the number of cointegrating vectors. Specifically, the hypotheses of interest are

![]()

The LR ratio test statistic, called the maximum eigenvalue statistic, is

![]()

Again, critical values of the test statistics are nonstandard and must be evaluated via simulation.

8.6.4 Forecasting of Cointegrated VAR Models

The fitted ECM can be used to produce forecasts. First, conditioned on the estimated parameters, the ECM equation can be used to produce forecasts of the differenced series ![]() . Such forecasts can in turn be used to obtain forecasts of

. Such forecasts can in turn be used to obtain forecasts of ![]() . A difference between ECM forecasts and the traditional VAR forecasts is that the ECM approach imposes the cointegration relationships in producing the forecasts.

. A difference between ECM forecasts and the traditional VAR forecasts is that the ECM approach imposes the cointegration relationships in producing the forecasts.

8.6.5 An Example

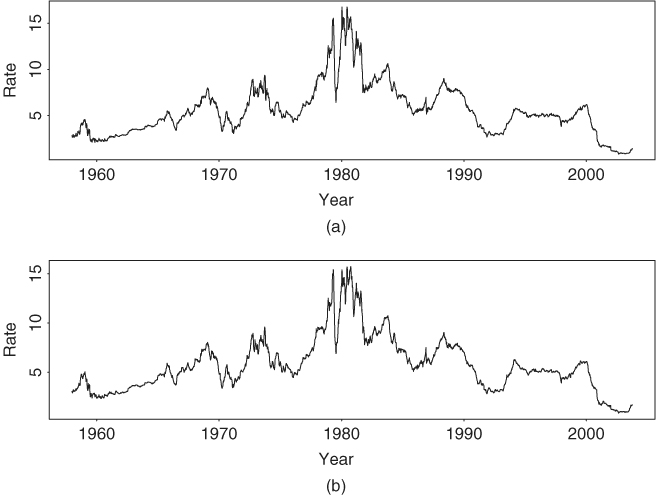

To demonstrate the analysis of cointegrated VAR models, we consider two weekly U.S. short-term interest rates. The series are the 3-month Treasury bill (TB) rate and 6-month Treasury bill rate from December 12, 1958, to August 6, 2004, for 2383 observations. The TB rates are from the secondary market and obtained from the Federal Reserve Bank of St. Loius. Figure 8.12 shows the time plots of the interest rates. As expected, the two series move closely together.

Figure 8.12 Time plots of weekly U.S. interest rate from December 12, 1958, to August 6, 2004. (a) The 3-month Treasury bill rate and (b) 6-month Treasury bill rate. Rates are from secondary market.

Our analysis uses the S-Plus software with commands VAR for VAR analysis, coint for cointegration test, and VECM for vector error correction estimation. Denote the two series by tb3m and tb6m and define the vector series ![]() . The augmented Dickey–Fuller unit-root tests fail to reject the hypothesis of a unit root in the individual series; see Chapter 2. Indeed, the test statistics are − 2.34 and − 2.33 with p value about 0.16 for the 3-month and 6-month interest rate when an AR(3) model is used. Thus, we proceed to VAR modeling.

. The augmented Dickey–Fuller unit-root tests fail to reject the hypothesis of a unit root in the individual series; see Chapter 2. Indeed, the test statistics are − 2.34 and − 2.33 with p value about 0.16 for the 3-month and 6-month interest rate when an AR(3) model is used. Thus, we proceed to VAR modeling.

For the bivariate series ![]() , the BIC criterion selects a VAR(3) model:

, the BIC criterion selects a VAR(3) model:

> x=cbind(tb3m,tb6m)

> y=data.frame(x)

> ord.choice$ar.order

[1] 3

To perform a cointegration test, we choose a restricted constant for ![]() because there is no reason a priori to believe the existence of a drift in the U.S. interest rate. Both Johansen's tests confirm that the two series are cointegrated with one cointegrating vector when a VAR(3) model is entertained.

because there is no reason a priori to believe the existence of a drift in the U.S. interest rate. Both Johansen's tests confirm that the two series are cointegrated with one cointegrating vector when a VAR(3) model is entertained.

> cointst.rc=coint(x,trend=‘rc’, lags=2) % lags = p-1.

> cointst.rc

Call:

coint(Y = x, lags = 2, trend = “rc”)

Trend Specification:

H1*(r): Restricted constant

Trace tests sign. at the 5% level are flagged by ‘ +’.

Trace tests sign. at the 1% level are flagged by ‘++’.

Max Eig. tests sign. at the 5% level are flagged by ‘ *’.

Max Eig. tests sign. at the 1% level are flagged by ‘**’.

Tests for Cointegration Rank:

Eigenvalue Trace Stat 95% CV 99% CV

H(0)++** 0.0322 83.2712 19.96 24.60

H(1) 0.0023 5.4936 9.24 12.97

Max Stat 95% CV 99% CV

H(0)++** 77.7776 15.67 20.20

H(1) 5.4936 9.24 12.97

Next, we perform the maximum-likelihood estimation of the specified cointegrated VAR(3) model using an ECM presentation. The results are as follows:

> vecm.fit=VECM(cointst.rc)

> summary(vecm.fit)

Call:

VECM(test = cointst.rc)

Cointegrating Vectors:

coint.1

1.0000

tb6m −1.0124

(std.err) 0.0086

(t.stat) −118.2799

Intercept* 0.2254

(std.err) 0.0545

(t.stat) 4.1382

VECM Coefficients:

tb3m tb6m

coint.1 −0.0949 −0.0211

(std.err) 0.0199 0.0179

(t.stat) −4.7590 −1.1775

tb3m.lag1 0.0466 −0.0419

(std.err) 0.0480 0.0432

(t.stat) 0.9696 −0.9699

tb6m.lag1 0.2650 0.3164

(std.err) 0.0538 0.0484

(t.stat) 4.9263 6.5385

tb3m.lag2 −0.2067 −0.0346

(std.err) 0.0481 0.0433

(t.stat) −4.2984 −0.8005

tb6m.lag2 0.2547 0.0994

(std.err) 0.0543 0.0488

(t.stat) 4.6936 2.0356

Regression Diagnostics:

tb3m tb6m

R-squared 0.1081 0.0913

Adj. R-squared 0.1066 0.0898

Resid. Scale 0.2009 0.1807

> plot(vecm.fit)

Make a plot selection (or 0 to exit):

1: plot: All

2: plot: Response and Fitted Values

3: plot: Residuals

...

13: plot: PACF of Squared Cointegrating Residuals

Selection:

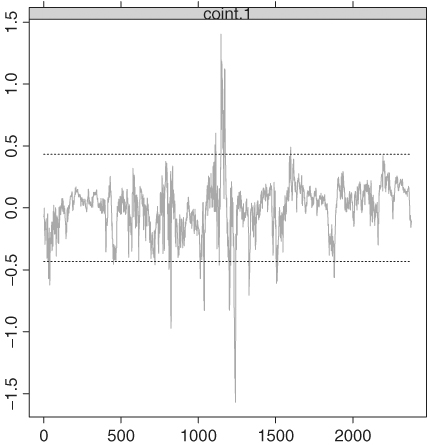

As expected, the output shows that the stationary series is wt ≈ tb3mt − tb6mt and the mean of wt is about − 0.225. The fitted ECM is

and the estimated standard errors of ait are 0.20 and 0.18, respectively. Adequacy of the fitted ECM can be examined via various plots. For illustration, Figure 8.13 shows the cointegrating residuals. Some large residuals are shown in the plot, which occurred in the early 1980s when the interest rates were high and volatile.

Figure 8.13 Time plot of cointegrating residuals for an ECM fit to weekly U.S. interest rate series. Data span is from December 12, 1958, to August 6, 2004.

Finally, we use the fitted ECM to produce 1-step- to 10-step-ahead forecasts for both ![]() and

and ![]() . The forecast origin is August 6, 2004.

. The forecast origin is August 6, 2004.

> vecm.fst=predict(vecm.fit, n.predict=10)

> summary(vecm.fst)

Predicted Values with Standard Errors:

tb3m tb6m

1-step-ahead −0.0378 −0.0642

(std.err) 0.2009 0.1807

2-step-ahead −0.0870 −0.0864

(std.err) 0.3222 0.2927

...

10-step-ahead −0.2276 −0.1314

(std.err) 0.8460 0.8157

> plot(vecm.fst,xold=diff(x),n.old=12)

> vecm.fit.level=VECM(cointst.rc,levels=T)

> vecm.fst.level=predict(vecm.fit.level, n.predict=10)

> summary(vecm.fst.level)

Predicted Values with Standard Errors:

tb3m tb6m

1-step-ahead 1.4501 1.7057

(std.err) 0.2009 0.1807

2-step-ahead 1.4420 1.7017

(std.err) 0.3222 0.2927

...

10-step-ahead 1.4722 1.7078

(std.err) 0.8460 0.8157

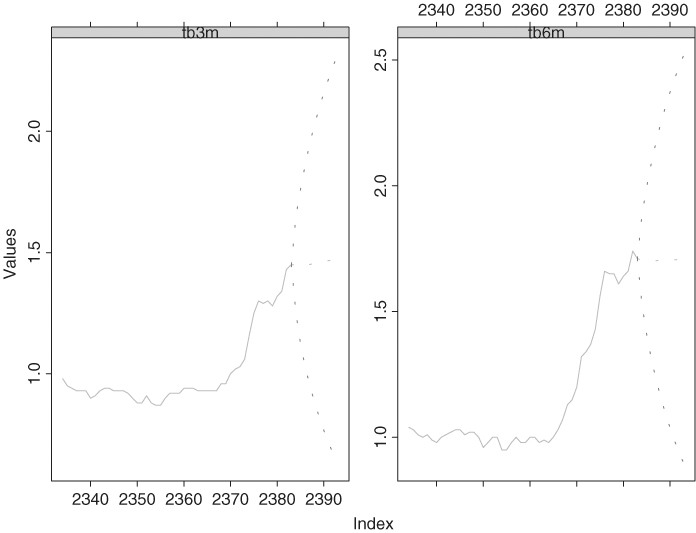

> plot(vecm.fst.level, xold=x, n.old=50)

The forecasts are shown in Figures 8.14 and 8.15 for the differenced data and the original series, respectively, along with some observed data points. The dashed lines in the plots are pointwise 95% confidence intervals. Because of unit-root nonstationarity, the intervals are wide and not informative.

Figure 8.14 Forecasting plots of fitted ECM model for weekly U.S. interest rate series. Forecasts are for differenced series and forecast origin is August 6, 2004.

Figure 8.15 Forecasting plots of fitted ECM model for weekly U.S. interest rate series. Forecasts are for interest rates and forecast origin is August 6, 2004.

Remark

The package urca of R can be used to perform Johansen's co-integration test. The command is ca.jo. It requires specification of some subcommands. See the section of pairs trading for demonstration.